Semtech's Growth Plateaued by Integration and Market Pressures Despite Revenue Stability

Semtech’s diversified semiconductor and IoT portfolio supports steady revenues but faces margin challenges and integration risks post Sierra Wireless acquisition.

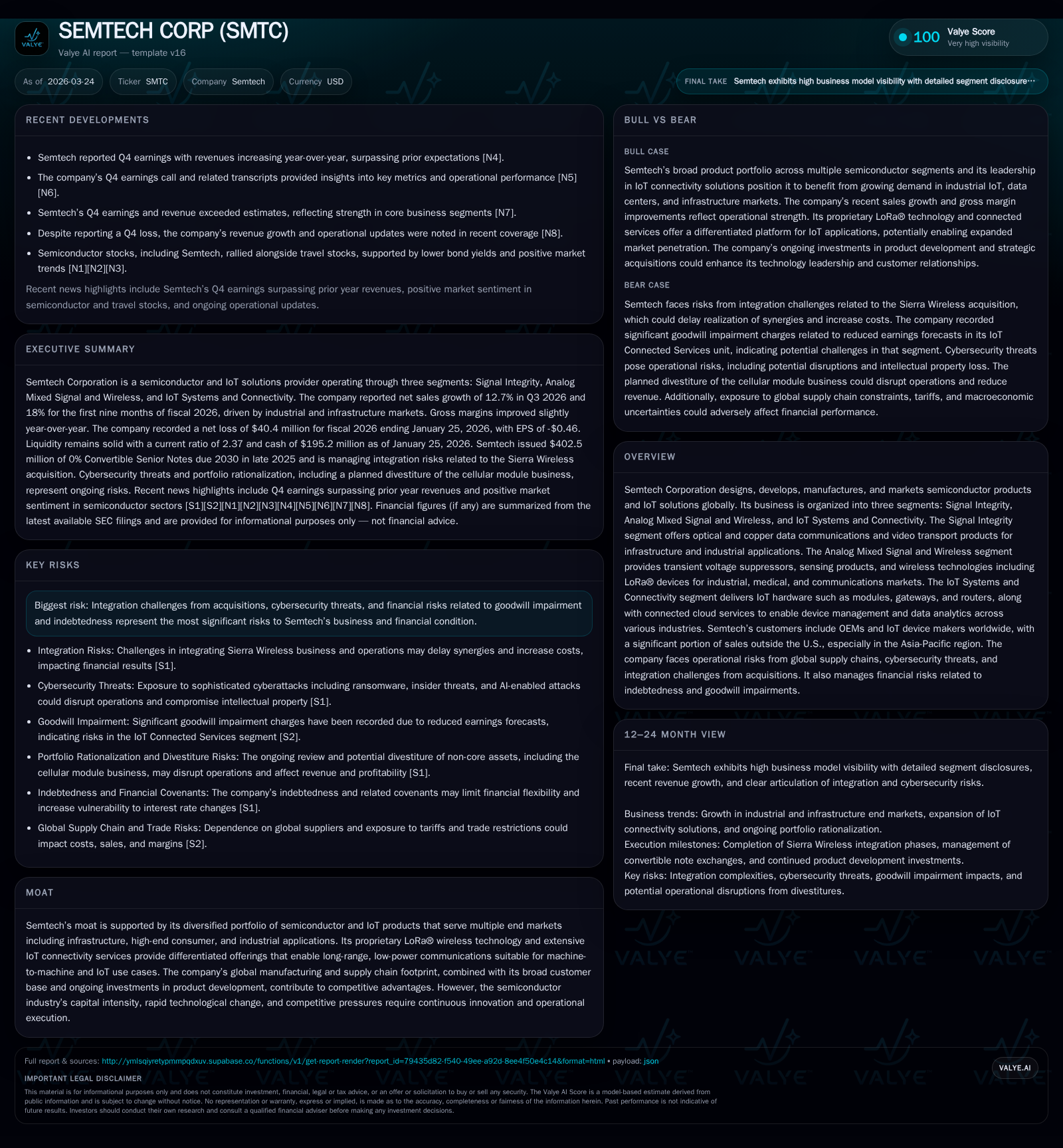

Semtech Corporation operates across three key segments with a strong product portfolio in semiconductors and IoT connectivity, including its proprietary LoRa wireless technology. While revenue has remained stable with modest growth, the company continues to face operational challenges related to integrating Sierra Wireless, which has dampened operating income and led to a net loss despite solid cash flows. Capital allocation has been conservative with no recent buybacks, and balance sheet leverage is managed with available credit lines. Going forward, success hinges on realizing synergies from acquisitions, controlling costs, and capturing demand in infrastructure and industrial IoT markets.

Company Overview

Semtech Corporation specializes in high-performance semiconductors and Internet of Things (IoT) solutions worldwide. Its portfolio spans three primary operating segments: Signal Integrity, Analog Mixed Signal and Wireless, and IoT Systems and Connectivity [S2]. The company leverages proprietary LoRa® wireless technologies within its Analog Mixed Signal segment for long-range, low-power machine-to-machine communications—a critical differentiator in IoT markets. Additionally, Semtech integrates IoT hardware such as modules and gateways with cloud connectivity services under its IoT Systems segment.

Historical Financial Performance

Semtech reported fiscal year 2026 revenue of approximately $140.6 million, essentially flat compared to prior years with only a 0.4% year-over-year increase [F1]. While top-line stability persists, profitability has been pressured; operating income dropped around 35% from $49.9 million last year to about $32.6 million due largely to integration costs tied to the Sierra Wireless acquisition and goodwill impairments [F1][S1][S26]. Net income remained negative at -$40.4 million but improved relative to previous losses of over $160 million a year prior [F1].

Operating cash flow showed marked improvement, more than tripling year-over-year from approximately $58 million to $181 million in FY2026, enabling capital expenditures close to $9.8 million focused on product development investments [F1][S21][S26]. This robust cash generation contrasts with net losses at the earnings line, indicating effective working capital management but ongoing cost pressures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -40 | 181 | 33 | 10 | +75.1% |

| 2025 | -162 | 58 | 50 | 8 | +85.2% |

| 2024 | -1092 | -94 | -944 | 29 | -1879.1% |

| 2023 | 61 | 127 | 93 | 28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 171 | -7.3 | |

| 2025 | 0 | 50 | -29.8 |

| 2024 | 0 | -123 | 355.2 |

| 2023 | 50 | 98 | 8.1 |

Source: SEC companyfacts cache [F1].

*Note: Revenue exhibits near flat growth while operating income suffered due to acquisition-related charges; CFO rebounded significantly.

Growth Drivers and Industry Positioning

Semtech’s portfolio benefits from diversification across infrastructure (including data centers and carrier networks), high-end consumer electronics, and industrial markets such as smart utilities and connected spaces [S17][N2]. Within these verticals:

- Signal Integrity solutions target critical communications infrastructure requiring high-speed optical transceivers supporting up to 1.6 Tbps speeds.

- Analog Mixed Signal & Wireless enhances device robustness via transient voltage suppression products while expanding wireless reach through its LoRa platform—favored for IoT use cases due to long range and low power consumption.

- The IoT Systems & Connectivity segment integrates hardware platforms like routers and gateways with cloud device management services enabling scalable IoT deployments.

LoRa-enabled offerings have driven increased sales volumes in Analog Mixed Signal & Wireless during recent quarters amid rising industrial IoT adoption globally [S22][N2]. The Asia-Pacific region accounts for the bulk of sales (~68-80%), reflecting concentration in manufacturing hubs with growing infrastructure modernization initiatives [S17].

Challenges Capping Growth Potential

Despite innovation strengths, Semtech faces headwinds notably from its ongoing efforts to absorb Sierra Wireless' business. Integration complexities have manifested as operational disruptions, elevated costs, delayed synergy realization, workforce assimilation issues, and risks surrounding internal controls impacting financial reporting reliability [S1][N3]. These factors weigh heavily on operating margins.

Furthermore, the semiconductor sector’s rapid technological evolution requires consistent R&D spend which depresses near-term profitability even as it seeds future opportunities [S26]. Macroeconomic uncertainties coupled with expanded industry competition add pressure on pricing power and inventory management [S13][N1]. Trade restrictions affecting supply chain geographies represent additional risks given Semtech's global footprint [S17].

Financial Outlook & Milestones

The company has yet to provide explicit forward guidance beyond operational commentary emphasizing inventory alignment actions amid variable demand conditions [S13][N14]. Key performance indicators to monitor include design wins of new semiconductor products that may translate into production orders, revenue growth particularly within the higher-margin Signal Integrity segment, progress against Sierra Wireless integration milestones, and gross margin trends reflecting shifts in product mix or cost efficiencies.

Capital Allocation & Returns

Semtech maintains a strong liquidity profile highlighted by $195 million in cash reserves supplemented by a sizable $455 million revolving credit facility with undrawn availability near $451 million as of late fiscal 2025 [F1][S5][S7]. This financial flexibility supports ongoing capital expenditures approximating $10 million annually aimed at new product introduction alongside strategic investment initiatives.

Notably, no stock repurchases occurred during recent periods despite an active buyback authorization totaling over $200 million remaining unused; this suggests prudent capital preservation priorities amidst integration uncertainties and debt management focus [S19][F1]. The company carries convertible senior notes due through 2030 bearing relatively low coupon rates (around 0-1.625%), positioning interest expense favorably though requiring attention on future conversion impacts [S10][S20].

Return metrics reflect current business pressures with an approximate ROE of -7.3% based on latest fiscal losses against equity base around $550 million; addressing profitability dilution remains essential for restoring shareholder returns [F1].

Industry Context (Analysis)

Semtech’s strategic emphasis on IoT connectivity aligns well with industry trends favoring edge computing proliferation and industrial automation advances leveraging LPWAN (Low Power Wide Area Network) technologies like LoRaWAN standardized via third-party ecosystems enhancing interoperability. Yet supply chain constraints common across semiconductors continue challenging timely fulfillment of rising IoT hardware demand globally. Additionally, competing wireless standards (NB-IoT, LTE-M) pressure differentiation efforts requiring agile innovation roadmaps.

Conclusion

Semtech Corporation embodies a diversified semiconductor firm extending traditional signal integrity solutions into emerging IoT system domains supported by unique LoRa-enabled wireless capabilities that underpin its competitive moat internationally. Despite sustained revenues near $140 million annually driven by infrastructure buildouts and industrial adoption across Asia-Pacific markets, the company’s financial results remain constrained by elevated acquisition integration costs stemming from Sierra Wireless. This challenge tempers operating income gains while net profitability stays negative even amid robust operating cash flows that fund steady-capital investment cycles. Liquidity remains ample with access to revolving credit mitigating near-term financing risk; however, restoring margin expansion through successful integration execution alongside continued product innovation will be critical for turning recent losses into sustainable returns. Investors should watch carefully for milestone achievements related to synergy realization timelines alongside design win announcements that presage upward revenue trajectories.

This analysis is based solely on information available as of March 24, 2026, including company filings and publicly released statements without any investment recommendation or forecast beyond disclosed facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments