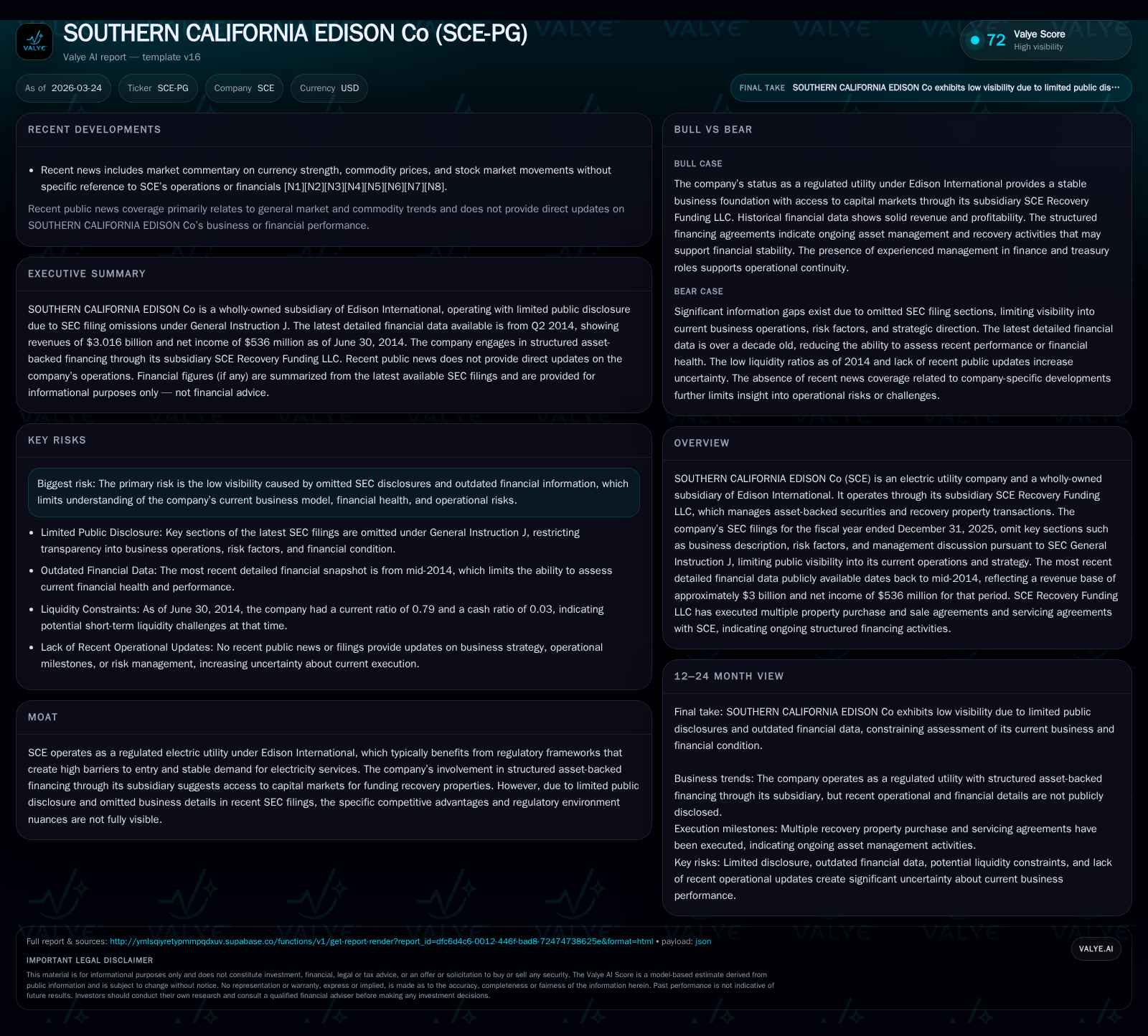

Southern California Edison’s Structural Financing and Regulatory Transparency Constraints Limit Visibility on Growth and Returns

SOUTHERN CALIFORNIA EDISON Co operates as a regulated utility with a complex asset-backed securities structure but opaque current financial disclosure.

Southern California Edison Company (SCE), a wholly owned Edison International subsidiary, functions primarily as a regulated electric utility in California. Its most recent detailed financial disclosures date back over a decade, with key business descriptions and risk factors omitted in recent SEC filings, reducing transparency. SCE’s growth is tied to regulatory approvals and capital-intensive infrastructure investment, while its financing strategy increasingly involves asset-backed securities through a specialized subsidiary. Historical financials show steady operating income and moderate net income growth through 2011, but free cash flow remains challenged due to large capital expenditures.

Company Overview and Structure

Southern California Edison Company (SCE) is a prominent electric utility serving the Southern California region. As a wholly owned subsidiary of Edison International, SCE operates within a highly regulated environment that fundamentally shapes its revenue stability and competitive positioning. Uniquely, SCE owns SCE Recovery Funding LLC, another wholly owned entity that manages an extensive portfolio of asset-backed securities (ABS) tied to recovery properties. This layered structure indicates strategic use of capital markets to finance substantial infrastructure needs.

Despite its significance in the California energy market, SCE’s most recent annual SEC filings for the fiscal year ended December 31, 2025 [S1] notably omit comprehensive business descriptions, risk factors, management discussion & analysis (MD&A), and legal proceedings pursuant to SEC General Instruction J. This substantially limits public transparency regarding its operational status, future initiatives, and risk exposure.

Historical Financial Performance

Publicly available detailed numeric data for SCE dates primarily from filings ending mid-2014 at the latest [F1]. At that time:

- Revenue was approximately $3.016 billion (mid-2014 quarterly figure).

- Operating income peaked at roughly $2.123 billion in FY2011.

- Net income hovered around $1.085 billion in FY2011.

- Operating cash flow ranged above $3 billion but free cash flow was negative due to capital expenditures exceeding CFO consistently.

- Capex rose from roughly $3 billion in FY2009 to over $4.1 billion by FY2011.

- Equity base expanded from $8.7 billion in FY2009 to nearly $10 billion by FY2011.

These figures show a mature utility scaling its infrastructure investments aggressively while realizing moderate earnings growth (approximately 13.9% operating income YoY increase from FY2010 to FY2011; net income grew circa 4.3% YoY). Persistent negative free cash flow (-$861 million estimated for FY2011) reflects intense reinvestment demands common among utilities adapting to regulatory requirements and aging assets.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Capex ($bn) | Net YoY |

|---|---|---|---|---|---|

| 2014 | |||||

| 2011 | 1085 | 3.3 | 2.1 | 4.1 | +4.3% |

| 2010 | 1040 | 3.4 | 1.9 | 3.8 | -15.2% |

| 2009 | 1226 | 4.1 | 1.9 | 3.0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2014 | ||

| 2011 | -861 | 10.9 |

| 2010 | -394 | 11.3 |

| 2009 | 1070 | 14.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue for full years is not detailed in the available data; last reliable revenue snapshot is Q2 2014.

Capital Structure and Liquidity

SCE demonstrated active debt management through early 2026 filings including agreement on new term loans totaling up to $1.5 billion maturing March 2027 [S5], simultaneous termination of prior term loan facilities without penalty, and bond issuances totaling $1.2 billion across maturities up to at least 2033 [S3][S18]. Such activity points to refinancing efforts amid an environment demanding liquidity for ongoing capital projects.

The company's revolving credit facilities are sizeable ($3.35 billion revolving credit mentioned), supported by parent company Edison International's own commitments [S5]. Covenants include maintaining consolidated indebtedness-to-capital ratios below specified thresholds (~0.65) which indicate scrutiny over leverage levels given the capital-intensive model.

Importantly, SCE Recovery Funding LLC manages significant ABS transactions involving recovery properties sold or serviced on behalf of SCE [S4][S12][S13]. These financing methods provide access to non-traditional funding channels beyond typical utility bonds or bank loans, reflecting sophisticated financial engineering consistent with sector trends toward off-balance-sheet structuring.

Regulatory Framework Impact

As a regulated monopoly under California Public Utilities Commission oversight, SCE’s revenues principally derive from tariffed rates approved via rate cases periodically submitted for approval. This adds stability but imposes constraints tied to regulatory timelines and allowed returns on invested capital.

The omission of any discussion on regulatory risks or rate case outcomes in the latest SEC filings restricts assessment of near-term catalysts or risks tied to policy changes, environmental mandates (e.g., wildfire liabilities), or energy transition initiatives crucial in California’s dynamic energy landscape [S11][S15].

Future Growth Prospects

Without explicit guidance disclosed in filings or press releases specific to SCE standalone operations [N#]/[S#], future growth prospects must be interpreted cautiously:

- Infrastructure modernization driven by grid reliability improvements and renewable integration represents both imperative expenditure areas and potential returns when sanctioned by regulators.

- Demand growth remains modest given mature customer base; incremental revenues likely depend on electrification trends (EV adoption) or efficiency programs promoted by policy shifts.

- Financing via asset-backed securities suggests continued reliance on structured transactions supporting recovery-related assets possibly linked to wildfire-related costs or other regulated recoverable expenses.

- Exposure to emerging regulatory hurdles or sudden cost escalations could cap growth if not efficiently managed or recovered through rates.

Returns and Capital Allocation

Historical metrics suggest an approximate return on equity around 10.9% based on net income versus equity for FY2011 [F1], aligning with typical utility expectations bounded by regulatory rate-setting frameworks.

Negative free cash flow underscores reinvestment phase dominance over discretionary returns such as dividends or share repurchases; recent disclosures lack information on dividends or buyback programs specific to SCE itself due to filing omissions [S1]. Equity holders’ return experience thus heavily depends on timely rate case approvals enabling recovery of invested capital plus authorized profits.

Key Executives and Governance

Management continuity appears intact with senior executive Aaron D. Moss serving as CFO since April 2022, supported by Treasurer Brendan Bond overseeing finance since late 2024 [S8]. Independent managerial oversight for the Recovery Funding LLC subsidiary ensures compliance with servicing responsibilities critical to ABS credibility [S8].

That said, lack of broader corporate governance discussions in public documents makes evaluation of strategic agility or risk governance challenging.

Sector Context — Analysis Only

Utilities with regulated monopolies benefit from demand stability but face intense scrutiny on cost structures amid accelerating infrastructure needs (e.g., wildfire mitigation). Asset-backed securitizations are becoming an important tool for these companies to isolate specific recoverable assets from core operations while tapping capital markets efficiently — a dynamic reflected at SCE through its Recovery Funding LLC unit.

California's aggressive renewable portfolio standards increase both capital requirements and operational complexity, forcing utilities like SCE into balancing system reliability investments with cost control — pressures that often manifest only gradually in ratemaking cycles.

What To Watch — Analysis Only

Investors should monitor future Edison International disclosures relating explicitly to SCE’s operational performance metrics once routine Form 10-K submissions resume full content disclosure post-omission periods.

Key indicators include:

- Outcomes of CPUC rate case filings impacting authorized ROE adjustments or capital expenditure recovery timelines,

- Trends in ABS issuance volumes signaling increasing leverage or changes in recovery asset monetization strategies,

- Changes in working capital sufficiency revealed through interim liquidity reports,

- Legal/regulatory developments related to wildfire liability provisions or environmental compliance costs,

- Parent company strategic shifts indicating altered investment priorities for subsidiaries like SCE.

Conclusion

Southern California Edison remains a cornerstone utility entrenched within California's regulated electricity framework operating under complex financial arrangements involving ABS structures tailored via its subsidiary arm for recovery property investments. Its solid historical earnings track record contrasts sharply with limited contemporary public disclosure that obscures current operational realities and strategic outlooks.

Growing reliance on sophisticated financing tools accompanied by active debt refinancings captures the company’s effort at navigating high capital demands amid constrained transparency layers caused by omission of key SEC reporting sections under General Instruction J provisions.

Until more granular disclosures emerge offering forward-looking clarity about risk profiles or growth plans beyond parent-level commentary, proxying value creation potential rests heavily on legacy financial patterns extrapolated cautiously alongside sector-wide regulatory dynamics shaping every U.S.-based electric utility’s trajectory today.

This analysis is based strictly on publicly available information as of March 24, 2026, including SEC filings with noted exclusions per regulatory allowances; newer data sources were unavailable at this writing which limits completeness regarding current performance or future expectations for SOUTHERN CALIFORNIA EDISON Co.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments