Concord Acquisition Corp II's Pursuit of Business Combination: Financials and Strategic Outlook

Concord Acquisition Corp II remains focused on closing its business combination with Events.com while navigating liquidity and regulatory challenges typical for SPACs.

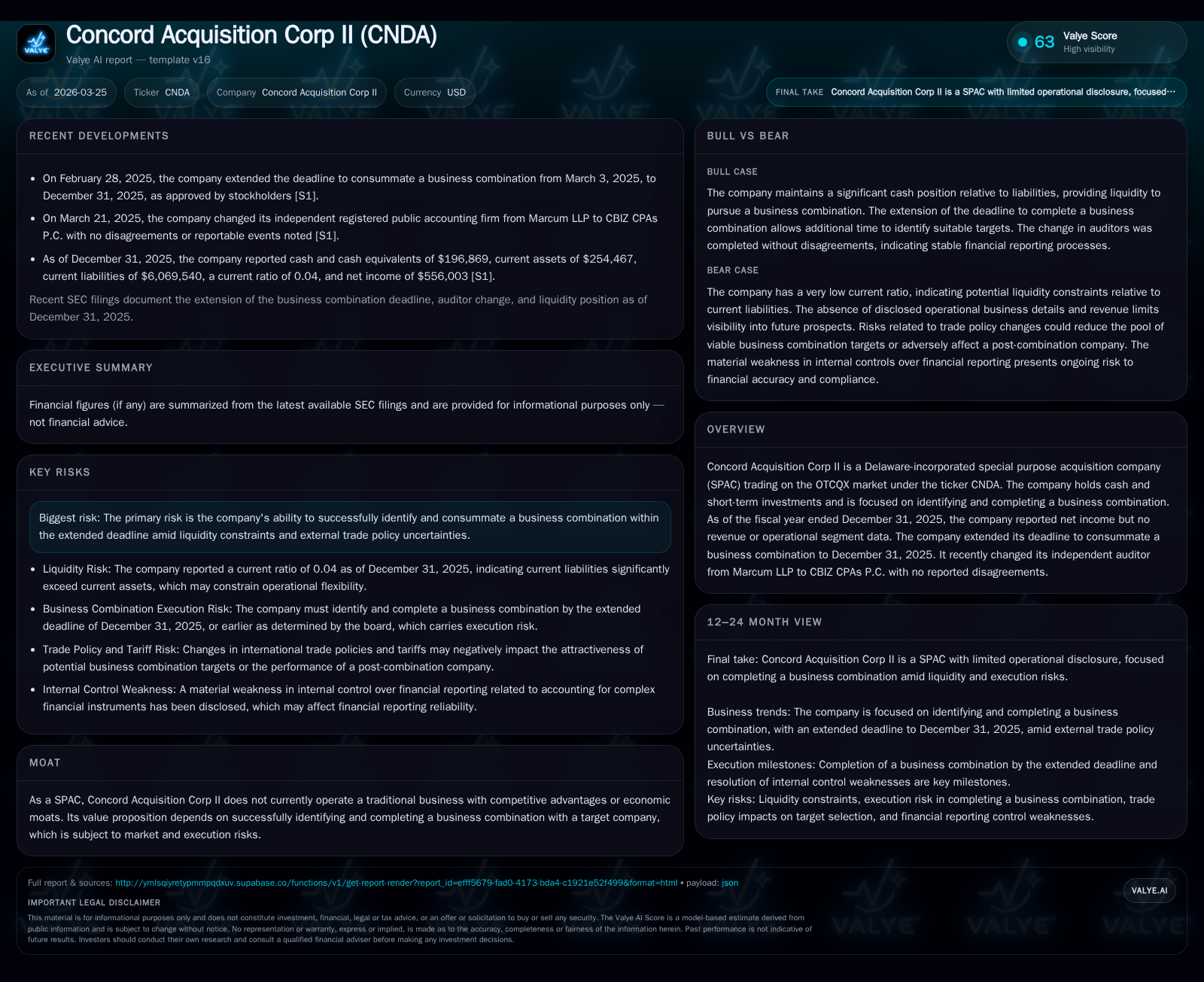

Concord Acquisition Corp II operates as a special purpose acquisition company (SPAC) without traditional operations, seeking to complete a business combination by the extended deadline of December 31, 2025. Its recent financials reflect typical SPAC dynamics: operating losses persist but accompanied by positive net income due primarily to non-operational factors. The company faces execution risks common to SPACs, including shareholder voting discretion and potential adverse impacts from evolving U.S. trade policies on acquisition targets. Capital structure shows tight liquidity and negative equity reflective of warrant dilution and redemptions; no dividends or buybacks have been initiated. Moving forward, milestones around the merger with Events.com, regulatory approvals, and market reactions will be key indicators to monitor.

Historical Financial Performance and Operating Realities

Concord Acquisition Corp II exemplifies a typical special purpose acquisition company (SPAC) which raises capital through an initial public offering (IPO) expressly to pursue a merger or acquisition without current operational revenues. As such, Concord’s financials reflect this paradigm: it reports no revenue streams but incurs operating expenses related primarily to corporate overhead and merger activities.

From fiscal year (FY) 2022 through FY2025, Concord sustained operating losses each year. However, FY2025 showed an improved operating loss of approximately -$1.27 million compared to -$2.15 million in FY2024 — a roughly 41% year-over-year improvement [F1]. This easing loss trend may reflect cost discipline or reduced transactional expenses as the company finalizes negotiations with a target.

Interestingly, despite ongoing operating losses, Concord posted positive net income of $556,003 in FY2025 compared to a net loss of -$766,076 the prior fiscal year [F1]. This suggests that non-operating gains—likely related to changes in warrant liabilities or other financial instruments common in SPAC structures—have offset operational expenditures during the period. Investors should interpret net income figures cautiously given the absence of typical business revenues.

Operating cash flow has remained negative but improved from -$1.55 million in FY2024 to -$928,608 in FY2025 [F1], indicating an ongoing cash burn albeit at a reduced rate consistent with pre-business combination activity. Equity remains deeply negative at approximately -$8.75 million as of FY2025-end, slightly improved from -$8.97 million the prior year but indicative of capital impact from warrant exercises and shareholder redemptions which erode book value [F1].

These dynamics underscore Concord’s status as a 'blank check company' with financial metrics governed more by capital market transactions than operating performance.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 1 | -1 | -1 | +172.6% |

| 2024 | -1 | -2 | -2 | -111.0% |

| 2023 | 7 | -4 | -2 | -52.1% |

| 2022 | 15 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -6.4 |

| 2024 | 8.5 |

| 2023 | -84.8 |

| 2022 | -142.4 |

Source: SEC companyfacts cache [F1].

Table: Concord Acquisition Corp II: Historical Financial Summary (FY2022-FY2025) [F1]

Extended Business Combination Timeline and Target Acquisition Progress

Concord Acquisition launched its IPO on September 3, 2021 issuing over 28 million units raised gross proceeds near $280 million inclusive of partial option exercises and private placements tailored toward sponsor interests [S1]. Each unit comprises one share of Class A common stock plus one-third of one warrant exercisable at $11.50 — structuring standard in SPAC IPOs.

On August 26, 2024 Concord executed a definitive merger agreement with Events.com intending to merge via Concord’s wholly owned subsidiary into Events.com with it surviving as a wholly owned subsidiary post-transaction [S1]. This 'business combination' awaits customary conditions — obtaining stockholder approvals from both entities as required by applicable laws or exchange rules along with other closing conditions.

Notably Concord retains discretion on whether stockholders vote on the deal unless issuance exceeds thresholds triggering mandatory approval [S1]. This flexibility introduces execution risk whereby the Company could consummate the merger even absent majority public shareholder endorsement.

The initial deadline for completing this merger was March 3, 2025 but Concord successfully secured shareholder authorization at a February 28 special meeting to extend this Termination Date to December 31, 2025 — providing additional runway to finalize negotiations and satisfy contingencies [S13]. Approximately $23.8 million was redeemed by shareholders exercising liquidation rights at roughly $10.84 per share during this vote process leaving modest funds in trust [S13].

This extension underscores both investor caution and management’s commitment to closing the deal with Events.com before potentially liquidating remaining assets.

Trade and Regulatory Risks Shaping Deal Prospects

Recent shifts in United States trade policies present thorny risks that could affect target valuations or complicate deal execution for Concord’s proposed transaction.

Since early-2020s considerable escalations in tariffs—both imposed by the U.S. government on imports and retaliatory tariffs by trade partners—have disrupted traditional international supply chains [S5]. Such changes create "trade policy uncertainty" that can affect companies reliant on cross-border inputs or sales channels.

Specifically for potential post-combination businesses like Events.com or other targets assessed by Concord’s management team these tariff regimes may inflate costs or reduce market engagement opportunities thereby depressing expected returns post-merger [S5][S8]. The company's own disclosures note difficulty predicting the persistence of current tariff structures which complicates forecasting target financial performance after combination closes [S5].

Additionally these policy-driven dynamics sometimes necessitate contractual contingencies or cause deal term renegotiations owing to unforeseen material adverse effects — posing risk premiums on deal completion timing or valuation acumen.

Risks also stem from evolving regulatory scrutiny especially given some SPACs’ increased visibility; compliance burdens may hamper swift transaction closure.

Capital Structure, Liquidity Profile and Shareholder Returns

Concord’s capital structure reflects typical SPAC complexity involving sponsor-owned warrants alongside public shares issued during IPO plus option placements designed to align incentives while raising incremental funds.

At fiscal year-end December 31, 2025 total cash and cash equivalents stood at approximately $197 thousand against current liabilities exceeding $6 million—yielding an anomalously low current ratio near 0.04 that signals extremely tight liquidity within short maturities [F1]. This is attributable primarily to the accounting treatment whereby redeemable shares are classified as short-term liabilities rather than equity.

Equity reported remains negative at about $-8.75 million reflecting accumulated losses augmented by dilution impacts from warrant revaluations and exercised options which increase liability classification while suppressing net book value [F1][S7][S9][S12].

There is no evidence of dividend issuance or share repurchases as such payouts contradict SPAC fundamentals which prioritize preserving capital for eventual business combination deployment rather than distribution [S6][S9][S12].

On auditor matters Concord transitioned in early-2025 from Marcum LLP to CBIZ CPAs P.C with no disagreements reported between parties nor adverse audit opinions except continuing substantial doubt over going concern centered on uncertain deal closure [S10][S11][S14]. This change reflects normal industry consolidation trends rather than red flags.

Warrant exercises by sponsors generate incremental capital inflows but also add layers of complexity regarding ownership dilution post-merger—a critical factor investors monitor closely when evaluating pro-forma equity stakes.

Outlook and Key Milestones Ahead

Looking ahead the primary focus centers on achieving requisite conditions enabling successful consummation of the business combination by December 31 2025:

- Securing all necessary stockholder approvals without major dissent or redemption pressures,

- Fulfilling or waiving customary closing conditions including regulatory clearances,

- Disclosure of finalized pro-forma capitalization structure post-merger,

- Monitoring any adjustments or extensions requested should market or legal circumstances impede timely closure,

- Observing macroeconomic factors such as further U.S.-foreign trade tensions impacting underlying target valuations.

Absent explicit numeric guidance from management filings remain qualitative; market participants must parse SEC disclosures closely alongside announcements from both Concord Acquisition Corp II and Events.com.

Risk-reward calculations must weigh benefits of exposure to newly public merged entity against possibility of deal failure resulting in liquidation distributed at near trust values less costs.

Conclusion: Specialized Considerations for Evaluating Concord Acquisition Corp II

As a blank check company without operational revenues or historical performance metrics beyond financial statements dominated by capital market activities Concord represents an investment vehicle whose value depends critically on executing its stated business combination strategy successfully [S1].

Investors should consider:

- The potential absence of public security holder voting rights if tender offers replace meetings,

- Dilution effects from sponsor warrants converting into shares post-deal,

- Management's disclosed experience which carries no guarantee of future success,

- Risks posed by redemption exercises stripping trust account liquidity,

- Trade policy uncertainties influencing target viability.

These factors demand nuanced interpretation distinct from traditional equities within buy-side analysis frameworks.

This report synthesizes publicly filed information up through March 25 2026 related to Concord Acquisition Corp II without speculation beyond disclosed facts. It does not constitute investment advice nor endorse securities but aims to illuminate underpinning financial realities and strategic context surrounding this SPAC's path toward completing its declared business combination strategy.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments