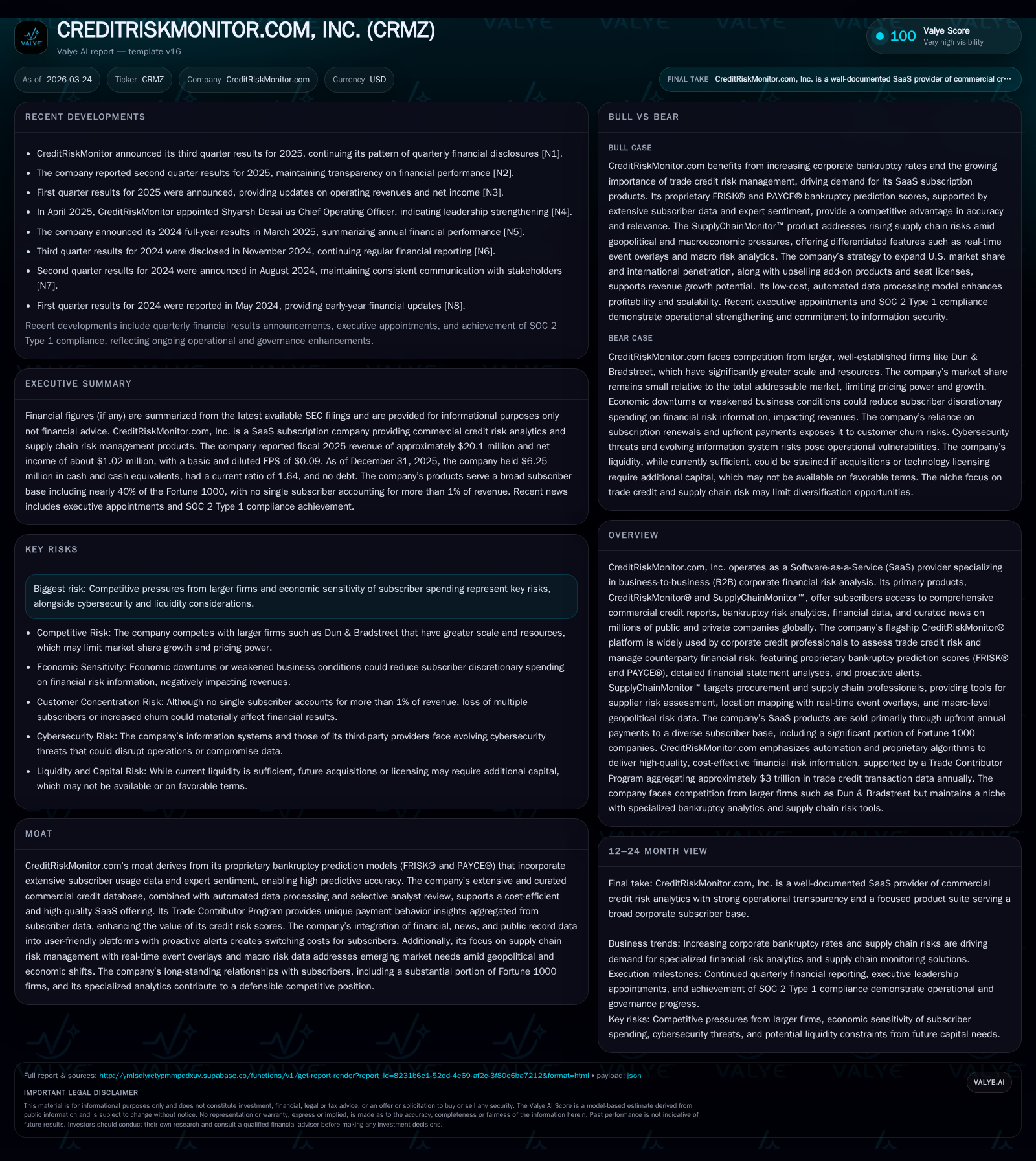

CreditRiskMonitor: Earnings Growth Slows Amid Margin Compression

CreditRiskMonitor reported modest revenue growth in 2025 while confronting significant pressure on operating income and cash flow margins.

CreditRiskMonitor.com, Inc. delivered incremental top-line gains of 1.6% in fiscal 2025, fueled by sustained subscription demand and product expansion, notably the SupplyChainMonitor™ platform. However, operating income contracted sharply by 53.4%, reflecting increased investments in sales infrastructure, CRM modernization, data content costs, and higher hosting expenses. Despite diminished operating cash flow, the company retains robust liquidity and a conservative capital allocation stance, generating a roughly 8.2% return on equity. Leveraging proprietary bankruptcy prediction models and a unique trade contributor data network, CreditRiskMonitor sustains a competitive moat in the financial risk SaaS industry but faces risks from larger competitors and cyclicality given economic sensitivity of trade credit spending.

Steady Revenue Growth Supported by Market Demand

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($mm) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 20 | 1017931 | 1 | 582031 | +1.6% | -39.2% |

| 2024 | 20 | 1674902 | 3 | 1249542 | +4.6% | -1.2% |

| 2023 | 19 | 1695053 | 1 | 1492096 | +5.3% | +24.6% |

| 2022 | 18 | 1360238 | 2 | 1571479 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1 | 8.2 |

| 2024 | 2 | 15.0 |

| 2023 | 1 | 18.1 |

| 2022 | 1 | 18.0 |

Source: SEC companyfacts cache [F1].

CreditRiskMonitor.com’s annual revenues increased modestly from approximately $19.81 million in FY2024 to about $20.12 million in FY2025, a year-over-year gain of roughly 1.6% [F1]. This steady expansion reflects continued subscription uptake for its flagship CreditRiskMonitor® financial risk platform and growth contributions from the more recently launched SupplyChainMonitor™ product focused on procurement and supply chain professionals [N1][S4][S5]. The revenue improvement has been driven both by adding new subscribers and renewing existing ones with some degree of price increases embedded in subscription fees [S7]. Notably, the company’s SaaS model ensures most revenues are collected upfront annually, providing stable visibility into near-term top-line performance [S18].

Market demand benefits from structural trends such as rising corporate bankruptcy filings—up approximately 32% over two years through 2025 compared to 2023—creating urgency among credit managers for timely risk analytics [S23]. The firm serves nearly 40% of Fortune 1000 companies alongside over a thousand large enterprises globally, illustrating broad industry acceptance [S18][S28]. These factors collectively underpin the slight but considered revenue advance amid challenging macroeconomic conditions.

Operating Income and Margins Show Signs of Pressure

While top-line growth persisted, CreditRiskMonitor’s operating income plunged from about $1.25 million in FY2024 to just $582 thousand in FY2025, equating to a steep decline of over 53% [F1]. This margin compression stems primarily from targeted investment activity as the company prioritizes longer-term growth over near-term profitability [S7][S18].

Specifically, selling, general and administrative expenses increased due to deploying a new Customer Relationship Management (CRM) platform intended to improve client engagement and sales effectiveness as well as augmenting its sales force [S7]. Concurrently, data content costs rose with third-party suppliers imposing higher charges reflecting broader inflationary pressures [S7]. Hosting expenses also grew owing to elevated production demands exacerbated by the expiration of leased office space previously contributing indirect cost relief [S9][S19].

This delicate balancing act typifies a high operating leverage environment common in subscription-based SaaS businesses where upfront development outlays weigh on margins until subscriber scale delivers efficiencies [S16]. The company anticipates some normalization as CRM-related redundancies materialize over time but remains committed presently to these expenses as necessary strategic investments.

Emerging Trends and Product Enhancements Shaping Future Potential

SupplyChainMonitor™ represents CreditRiskMonitor’s answer to heightened interest in supplier financial durability amid global disruptions affecting logistics and sourcing strategies [S4][S5][N1]. The product offers location mapping overlayed with real-time events such as weather disturbances or power outages alongside macro-level geopolitical risk data powered by the Economist Intelligence Unit across numerous risk vectors including labor stability, taxation regimes, legal environments, national security concerns, and more [S5].

These features cater directly to procurement professionals managing nuanced risk exposures amplified by shifts away from globalization towards “nearshore” or “friendshore” sourcing paradigms—a reaction necessitated in part by recent geopolitical tensions and trade uncertainties [S4][S5]. By integrating proprietary FRISK® bankruptcy scores with predictive analytics tailored for private companies via PAYCE®, the platform provides clients actionable foresight into supplier insolvency risk that can imperil manufacturing continuity or revenue streams if undetected [S28].

Additionally, the firm’s provision of curated news alerts filtered for material financial relevance ensures subscribers remain vigilant against subtle but critical developments impacting counterparties’ creditworthiness [S28]. This layered intelligence delivery exemplifies how CreditRiskMonitor positions itself at the nexus of fintech compliance demands and agile risk management.

Capital Allocation Focused on Controlled Investment and Modest Returns

CreditRiskMonitor.com maintains a conservative capital structure devoid of external debt or credit lines, emphasizing organic growth funded through internal cash generation and robust liquidity reserves predominantly held in U.S. Treasury securities [F1][S6][S18]. As of December 31, 2025, the company reported cash and equivalents around $6.25 million with healthy current assets exceeding current liabilities leading to a current ratio approximating 1.64—signaling substantial short-term solvency buffer [F1].

Operating cash flow fell significantly by about two-thirds year-over-year—from roughly $2.87 million in FY2024 down to below $1 million in FY2025—mirroring margin pressures discussed previously [F1]. Nevertheless free cash flow remains positive after subtracting capital expenditures which themselves retreated nearly 30%, indicating disciplined spending aligned with strategic priorities rather than imprudent expansion [F1]. The resulting free cash flow is close to $700 thousand annually.

Equity base expanded steadily through retained earnings with total shareholders’ equity reaching roughly $12.35 million at fiscal year-end despite profit contraction [F1]. The calculated return on equity stands at approximately 8.2%, an adequate figure reflecting moderate profitability characteristic for specialized SaaS providers reinvesting for future product breadth extension rather than maximizing immediate returns [F1][S18].

Competitive Moat Rooted in Proprietary Bankruptcy Analytics

CreditRiskMonitor's defensible competitive advantage is anchored primarily in its proprietary bankruptcy prediction models — FRISK® and PAYCE® — which are distinguished by incorporating rich subscriber behavior data reflecting collective payment experiences within its vast Trade Contributor Program totaling some $3 trillion in annualized transaction volume [N1][S22][S28].

The FRISK® score reportedly identifies nearly all public company bankruptcies at least three months ahead with circa 96% accuracy while PAYCE® extends similar predictive strength into private firm populations otherwise difficult to assess without public disclosures [S28]. These analytics synthesize multiple inputs including standard financial ratios alongside behavioral signals derived from expert users who effectively 'vote' with their financial decisions.

This synthesis creates formidable switching costs for customers deeply embedded into daily decision workflows reliant on proactive alerting mechanisms that rapidly surface emerging risks across thousands of counterparties [S28]. Such integration between real-time data ingestion pipelines, expert analysis support roles, automated report generation, and user-centric interface design positions CreditRiskMonitor favorably within the mid-market SaaS ecosystem specializing in trade credit risk assessment.

Risks from Competitive Landscape and Economic Cycle Sensitivity

Despite its tailored offerings and technical edge, CreditRiskMonitor faces significant headwinds stemming from entrenched competition primarily posed by Dun & Bradstreet Holdings which commands sizeable share within finance & risk enterprise segments exceeding $1 billion annually across North America alone—some two orders of magnitude larger than CRMZ’s reported revenues (~$20 million) [S14]. Other sizeable players include Experian plc and Equifax Inc., augmenting market fragmentation but intensifying pressure on pricing power and customer retention.

Additional risks derive from economic cyclicality since clients’ discretionary spending on enhanced credit monitoring often contracts during downturns when trade credit budgets tighten—in turn possibly elevating subscriber churn or slowing renewal rates impacting recurring revenues disproportionately relative to fixed costs [S21]. Cybersecurity threats also feature prominently given reliance on cloud-hosted financial data repositories demanding continuous vigilance against breaches that could undermine client trust or invite regulatory scrutiny.

Furthermore liquidity constraints appear manageable currently due to no debt load yet remain contingent upon stable subscriber inflows sustaining positive operating cash flows sufficient to meet internal cost structures during periods of fluctuating market conditions [F1][S18]. Monitoring these factors including market share evolution relative to larger competitors will be critical indicators going forward.

Disclaimer: This analysis does not constitute investment advice or recommendations but aims to provide an informed internal perspective based solely on reviewed public filings and company disclosures as of March 24, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments