Titan America’s Regional Cement Leadership and Integrated Logistics Shape Growth Through 2026

Titan America leverages vertical integration and its strategic Southeast and Mid-Atlantic footprint to sustain growth amid sector cyclicality.

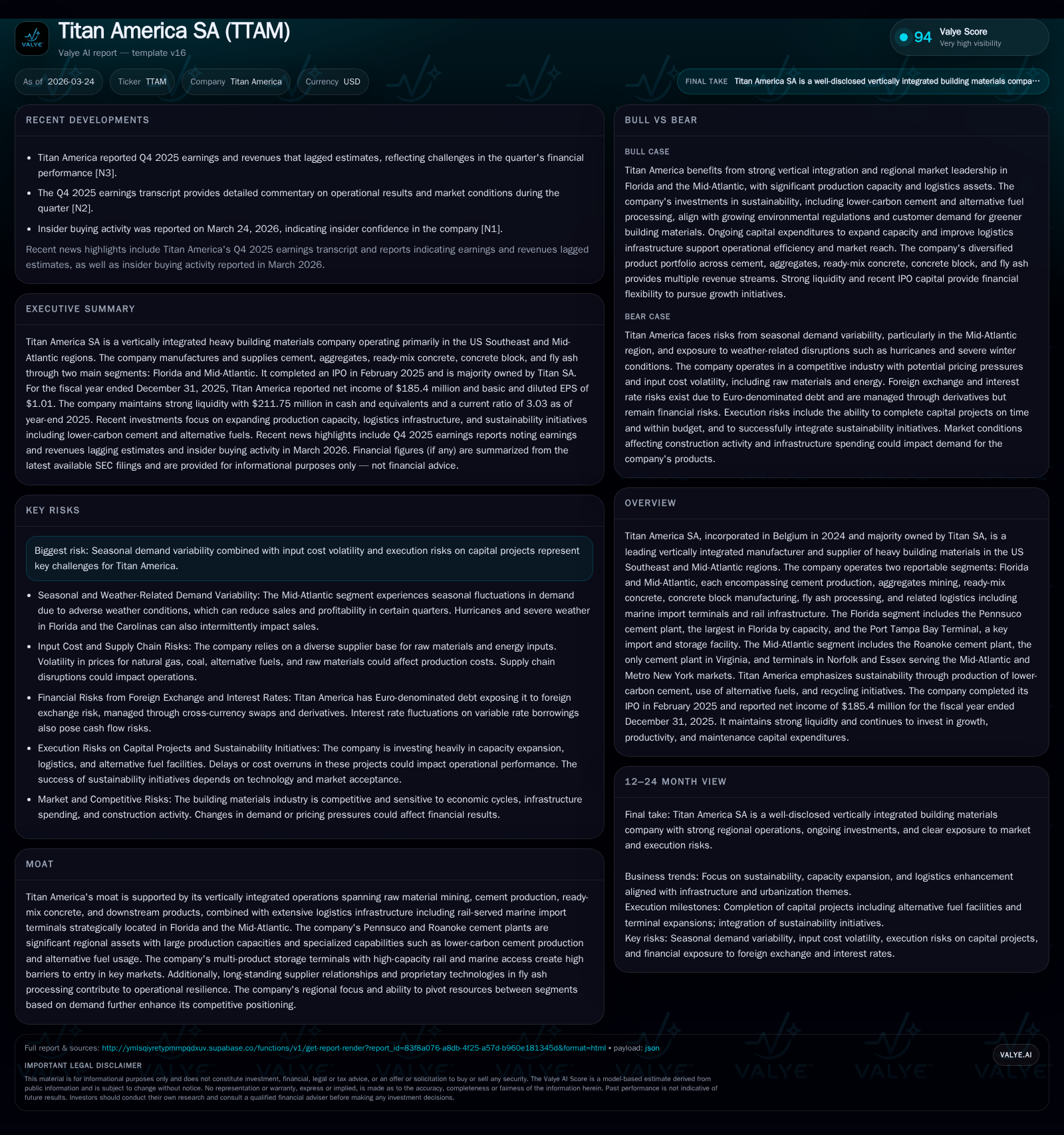

Titan America SA, a Belgium-incorporated firm majority-owned by Titan SA, commands a strong regional presence in the U.S. Southeast and Mid-Atlantic heavy building materials market. Its vertically integrated model spans raw materials to downstream concrete block production, supported by key regional assets such as the Pennsuco and Roanoke cement plants and multi-modal import terminals. The company exhibits steady revenue expansion driven by infrastructure demand and capacity investments, balanced against exposure to seasonal market swings and input cost volatility. Capital allocation emphasizes reinvestment for growth, with limited dividend payouts amid leverage management.

Company Overview and Historical Performance

Titan America SA was incorporated in Belgium in mid-2024 under Belgian law as a majority-owned subsidiary of Titan SA, the Greek multinational cement producer established in 1902. Titan America focuses on heavy building materials production predominantly across Florida (the Southeast) and the Mid-Atlantic U.S., offering a comprehensive product suite including cement, aggregates, ready-mix concrete, concrete blocks, fly ash processing, supported by logistics assets like marine terminals and rail infrastructure [S1][S15].

Key assets include the Pennsuco cement plant—the largest capacity plant in Florida—and Port Tampa Bay Terminal for marine imports. Meanwhile, the Roanoke Plant serves as Virginia’s sole cement producer with planned capacity expansion [S14][S19]. These operational centers support vertically integrated operations reaching from mining to downstream concrete-related products.

Financially, the company has demonstrated steady growth post-IPO (completed February 2025), with total external revenues increasing marginally from approximately $1.63 billion in 2024 to $1.66 billion in 2025 [F1][S26]. A breakdown by segment shows Florida as the larger contributor ($1.02 billion external revenue) versus Mid-Atlantic ($640 million) [S10][S24].

Segment product revenue growth has been supported by increases especially in aggregates (+24% YoY at Florida segment) and ready-mix concrete volumes across both regions [S10][S24]. Cement revenues declined slightly year over year but remain significant.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 185 | +11.7% |

| 2024 | 166 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 6 | 17.9 |

| 2024 | 85 | 22.1 |

Source: SEC companyfacts cache [F1].

*Adjusted EBITDA subtotal of Florida + Mid Atlantic segments before adjustments including corporate costs [S11][S26]

Future Growth Prospects

Titan America is actively investing to augment capacity and enhance sustainability initiatives that align with evolving market needs:

Capacity Expansion: At Roanoke Plant, an ongoing project targets increasing cement production capacity from approximately 1.5 million tons toward an anticipated goal of around 1.8 million tons by 2030 [S24].

Terminal Upgrades: Recent investments enhanced terminal storage — notably at Port Tampa Bay and Norfolk — adding domes capable of holding ~70,000 tons each plus multi-product silos [S15][S23]. These improvements facilitate flexible products handling while addressing stringent market entry barriers.

Alternative Fuels & Lower Carbon Products: Initiatives include incorporation of alternative fuels for kiln operations at Pennsuco and distribution of Low-Carbon Cement via strategic terminals supporting circular economy objectives , positioning Titan America competitively amid tightening environmental regulation.

Vertical Integration & Innovation: The company leverages proprietary fly ash beneficiation technologies inherited via former STET operations and supports innovation through proprietary mix design optimization fostering customer collaboration .

Growth could be capped by inherent fluctuations tied to construction demand variability—subject to economic cycles influencing infrastructure spending—and volatility in fuel/raw material costs (energy-intensive cement manufacturing being particularly sensitive) [S18]. Additionally, Titan America's noted weaknesses in internal controls over financial reporting may present operational risks affecting timely delivery on growth projects [S1].

Forecasts / Milestones / What To Watch

While explicit forward guidance has not been released per recent filings or earnings transcripts [N1][N2][S1], investors might monitor:

- Progress on Roanoke capacity expansion milestones aimed at raising cement output over the next five years.

- Integration success of recent terminal capacity increases especially regarding utilization rates impacting operating margins.

- Trends in raw material input costs such as natural gas prices though derivative hedging minimizes volatility impact near term [S9].

- Developments regarding any remediation measures or refinements implemented following disclosure of material control weaknesses impacting reporting accuracy [S1].

- Capital deployment decisions around acquisitions or technology investments as hinted by incremental due diligence expenses related to Keystone Cement Company acquisition efforts [S21].

Returns / Capital Allocation

Titan America displayed solid profitability management with net income reaching approximately $185 million for FY2025—an increase of nearly 12% over FY2024’s $166 million—delivering an approximate return on equity close to 18% based on year-end equity levels exceeding $1 billion [F1]. This suggests effective utilization of equity capital to generate shareholder returns.

Cash generation reflects strength as well; available cash & equivalents stood robust at about $212 million at end-2025 alongside a comfortable current ratio above three times, signaling liquidity adequacy for short-term obligations [F1].

Dividends paid plummeted from roughly $85 million in FY2024 to only about $6.4 million in FY2025—indicating a strategic scaling back of distributions likely aimed at preserving cash for reinvestment into growth capex exceeding $160 million annually recently and managing leverage levels associated predominantly with related party Euro-denominated loans hedged via currency swaps [F1][S7][S12].

Long-term debt is significantly linked to parent group financing arrangements denominated mostly in Euros—with risk mitigated by derivative instruments fixing currency exposure —as visually detailed within liability maturity profiles out beyond five years totaling sizable obligations but without near-term refinancing concerns noted [S7][S12].

Industry Positioning & Risks

Titan America's moat derives chiefly from its vertically integrated business model coupling production assets directly upstream from distribution channels combined with high-barrier logistics infrastructure inclusive of rail-served marine terminals tailored precisely for regional markets constrained by geographic supply dynamics . Such integration reduces dependency on third-party suppliers while allowing resource shifts between segments responsive to demand.

Risks remain pertinent including:

- Construction cyclical seasonality impacting volume timing,

- Raw material cost volatility notably fluctuating energy prices,

- Execution risk on ramping up new capacity projects,

- Material control weaknesses potentially affecting governance and transparency.

Externally governed environmental compliance demands impose further capital allocation needs but also contribute toward differentiating lower-carbon product offerings which increasingly influence buyer preferences under tightening sustainability policies [S18].

Conclusion

Titan America stands as a regionally focused heavy building materials leader benefiting from vertical integration reducing supply chain risk while commanding critical cement production capacities complemented by strategically located import terminals facilitating cost-efficient delivery throughout complex Eastern U.S. urban and infrastructure corridors.

Historical financial trends reflect steady topline expansion fueled by diversified product lines within two major segments imbued with strategic capex investments targeting capacity growth and product innovation demanding disciplined cash flow stewardship evident through adjusted dividend policies.

Operational vigilance will be key amidst macroeconomic headwinds characteristic of construction cycles plus ongoing focus required on remediating disclosed internal control deficiencies to ensure sustained organizational robustness going forward.

This report synthesizes publicly available SEC filings including Titan America’s latest Form 20-F filed March 24, 2026 ([S1]), supplemented by recent earnings disclosures ([N1],[N2]) along with internally sourced company facts data ([F1]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments