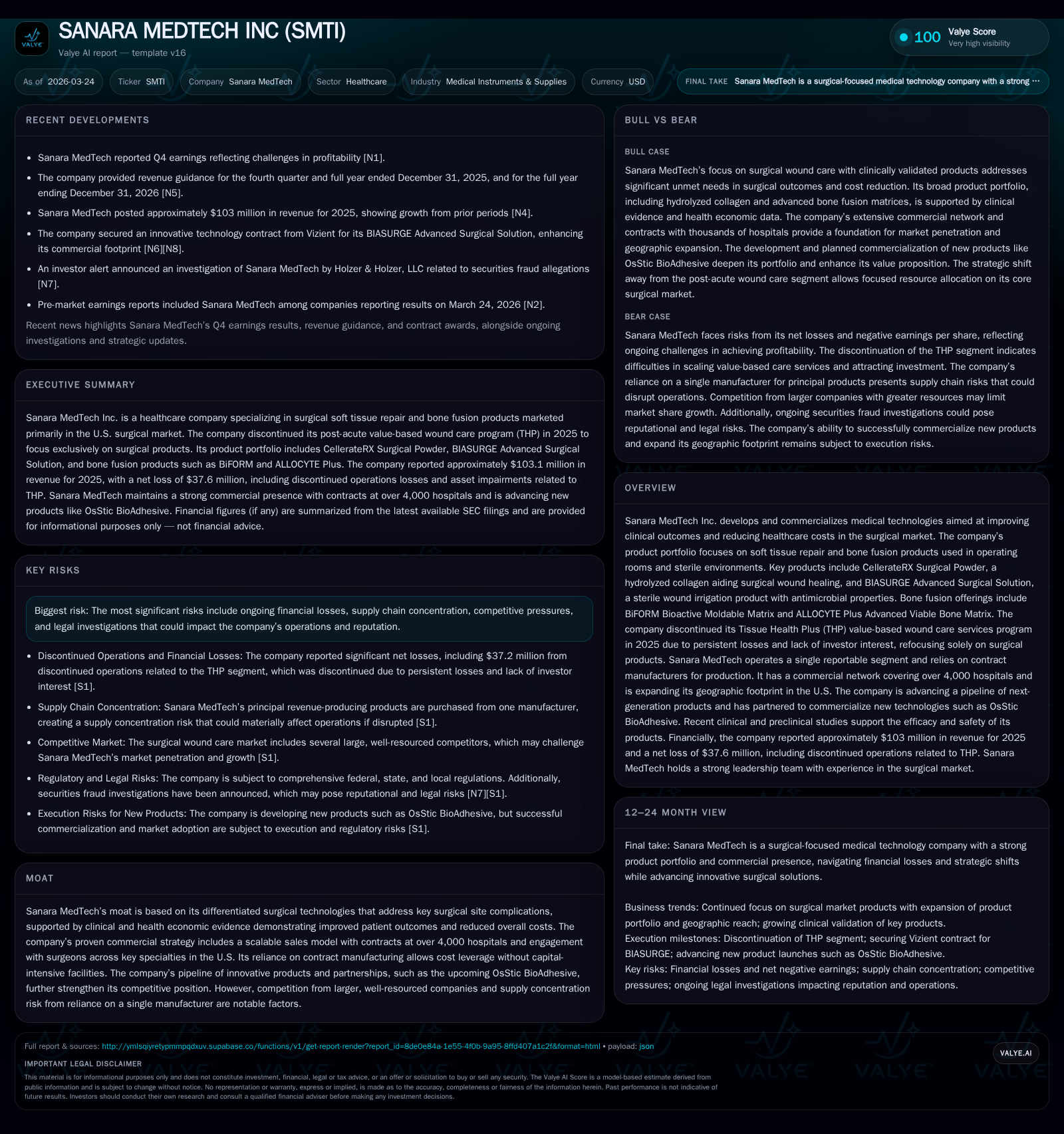

Sanara MedTech's Financial Recovery Amid Surgical Market Concentration Risks

A comprehensive analysis of Sanara MedTech’s rebound after exiting value-based wound care and focusing on its core surgical product line amid industry headwinds.

Sanara MedTech Inc. has recently achieved a significant turnaround in operating profitability following its strategic exit from the loss-making Tissue Health Plus (THP) program. By concentrating resources exclusively on its surgical portfolio—primarily soft tissue repair and bone fusion products—the company leveraged contract manufacturing efficiencies to improve margins, increasing operating income from a loss position to $7.3 million in 2025. Despite the operating income rebound and stronger cash flow, net losses deepened due to non-operating factors. The company faces risks from supplier concentration and competitive pressures as it advances pipeline innovations such as the OsStic BioAdhesive. Monitoring execution and adoption of new surgical technologies will be critical to sustaining growth.

Transforming Surgical Care: Core Product Portfolio Overview

Sanara MedTech’s strategic foundation lies in developing medical technologies designed for sterile surgical environments with an emphasis on improving clinical outcomes while controlling costs. Its soft tissue repair product line centers around CellerateRX Surgical Powder—an FDA-cleared hydrolyzed collagen that facilitates accelerated healing in surgical wounds—and BIASURGE Advanced Surgical Solution, a sterile no-rinse irrigation fluid featuring antimicrobial properties important for reducing infection risk intraoperatively [S1]. These products are tailored for diverse specialties where managing surgical site complications determines postoperative recovery trajectories.

On the orthobiologics front, Sanara markets BiFORM Bioactive Moldable Matrix, an osteoconductive porous implant promoting bony ingrowth, and ALLOCYTE Plus Advanced Viable Bone Matrix—a human allograft enriched with viable progenitor cells combined with conformable bone fibers—to address challenges in bone fusion procedures [S1]. The portfolio reflects an understanding of surgeon preferences for bioactive scaffolds that integrate biologically to enhance fusion rates without excessive complication risk.

The in-house R&D subsidiary Rochal Technologies underpins ongoing innovation focusing on the "Prepare, Promote and Protect" framework—preparing tissue beds, promoting healing pathways, and protecting wounds from microbial invasion [S1]. This orientation anticipates evolving OR practices emphasizing minimally invasive techniques coupled with efficacious adjuncts to reduce both complications and associated healthcare spend.

Historical Growth Trajectory and Key Performance Drivers

Sanara MedTech has experienced notable financial oscillations over the past decade as it balanced expansion ambitions against market execution realities. Revenue grew steadily from $5.5 million in FY2016 to nearly $15.6 million by FY2020 [F1]. However, real inflection arrived post-2020 coinciding with intensified product distribution efforts across over 4,000 U.S. hospitals, particularly within key surgical specialties leveraging soft tissue repair solutions.

The year-over-year revenue jump was pronounced by 167% in FY2025 compared to FY2024 driven primarily by burgeoning sales of core soft tissue repair items like CellerateRX Surgical Powder as well as BIASURGE irrigation solution [F1], [S9]. Operating income likewise recovered sharply from a $6.7 million loss in FY2024 to a positive $7.3 million in FY2025—a swing underscoring scaled operational leverage and tighter control over selling, general & administrative expenses despite investments in salesforce expansion [F1].

Net income painted a more complex picture; losses deepened to -$37.6 million reflecting substantial non-operating expenses including interest costs tied to debt facilities drawn for acquisitions and working capital [F1], [S4]. Still, the improvement at the operational level signals a transition phase toward stabilization.

Operating cash flow rebounded robustly to nearly $6.8 million indicating effective conversion from earnings before non-cash charges and debt servicing costs coupled with disciplined working capital management [F1]. Capital expenditures more than doubled reaching $4.6 million as management invested strategically into manufacturing capabilities through acquisitions and product pipeline development initiatives [F1], [S9].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -38 | 7 | 7 | 5 | -288.7% |

| 2024 | -10 | 0 | -7 | 0 | -124.6% |

| 2023 | -4 | -3 | -4 | 0 | +45.8% |

| 2022 | -8 | -6 | -12 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 2 | -632.5 |

| 2024 | 0 | -24.5 |

| 2023 | -4 | -9.6 |

| 2022 | -6 | -19.0 |

Source: SEC companyfacts cache [F1].

Note: Exact revenue figures for fiscal years 2024 and 2025 are not explicitly stated but growth rates are derived from SEC narratives and company disclosures.

Exit from Tissue Health Plus (THP): Rationale and Implications

The discontinuation of THP in mid-September 2025 marks a definitive pivot away from diversified but unprofitable ventures toward core competencies centered on surgical devices [S1], [N1]. Initially incubated as a value-based wound care program targeting payers and risk-bearing entities aiming to reduce hospitalization rates via enhanced post-acute care coordination and telehealth integration [S1], THP consistently failed to attract sufficient external investment or generate meaningful margins despite strategic acquisition support.

Multiple outreach efforts through venture capital channels and strategic buyers culminated unsuccessfully leaving continued losses unchecked—informed both board-level decisions to cease operations and redirect capital [S1]. This termination trimmed complexity out of financial reporting with management consolidating focus solely on product lines underpinning positive operating income metrics [N1].

Operationally this reduced overhead burdens associated with service delivery infrastructure while recasting sales channels around tangible medical instruments favored by surgeons in hospital settings rather than extended care ecosystems [S1], yielding margin improvement prospects going forward.

Financial Turnaround: Revenue Surge and Operating Income Improvement

Despite a Q4 earnings miss reported on March 24, 2026 [N1], full-year performance reflected dramatic operational improvements juxtaposed against prior years’ erosion [F1], [S3]. Sanara generated gross profit exceeding $95 million on revenues surpassing $103 million mainly attributable to heightened sales velocity of soft tissue repair products including flagship CellerateRX Surgical Powder whose manufacture became less costly translating into gross margin expansion north of 90% for FY2025 [S9].

SG&A increased modestly due largely to expanded direct sales expenditures necessary for broader U.S. market development offset partially by leaner service layer post-THP shutdown; R&D spending doubled as well consistent with roadmap enhancements on its core biologics platforms [S9]. Depreciation rates remained stable suggesting capital investments focused more heavily on intangible asset development related to licensing deals such as BMI partnership for OsStic distribution rights secured during calendar year 2025 [S16], [S19].

Cash flows tell a complementary story; operating cash inflows rebounded robustly supporting capex needs while eliminating negative working capital swings evident in prior periods [F1]. These figures collectively indicate foundational business health improving notwithstanding overarching net loss pressures rooted outside operating activities.

Growth Prospects in Surgical Technologies and Pipeline Innovation

A keystone growth vector for Sanara rests on advancing OsStic BioAdhesive commercialization under an exclusive license agreement with BMI acquired early in 2025 targeting trauma indications alongside expansions into sports medicine and spinal applications negotiated mid-year—the so-called “Prepare, Promote and Protect” strategy at work identifying segments poised for adoption of bioactive bone adhesives promising better fixation outcomes than conventional materials used today [S1], [N2], [S19].

This initiative complements an expanding footprint with core products gaining traction across existing hospital accounts while bolstering independent distributor networks servicing broader geographic regions within the U.S.—an acknowledged competitive edge given large institutional purchasers’ demand for proven clinical efficacy balanced against total cost reduction claims supported by clinical evidence [S1],[S9].

Conversely, prospects for renewed investments into post-acute wound care appear limited following THP shuttering reducing diversification but sharpening focus toward higher-margin surgical interventions unlikely matched easily by competitors given intellectual property licensing frameworks combined with contract manufacturing structures enabling scaled cost control.

Capital Allocation Strategy: Cash Flow Stability Amid Debt Obligations

Sanara maintained liquidity prudently exiting fiscal year-end December 31, 2025 with approximately $16.6 million cash balance amid senior secured indebtedness totaling about $46.9 million maturing March 30, 2029 under CRG Term Loan facilities bearing effectively about 13% interest including deferred components subject to quarterly payment obligations—covenants stipulate escalating revenue floors reaching $105 million by calendar year-end 2027 ensuring top-line discipline according to loan agreements disclosed [F1], , [S21].

Capital expenditure accelerated substantially to roughly $4.6 million representing investments into acquisition integration (e.g., CarePICS), technology augmentation as well as infrastructure supporting commercial scale-up efforts ([F1],[S9]). Operating cash flow turnaround contributed positively toward free cash flow generation estimated near $2.2 million after capex consideration demonstrating improving internal funding ability absent reliance solely on debt or equity injections.

No dividends or share repurchase programs were noted indicating retained earnings focused internally consistent with tech commercialization phase requiring reinvestment prior to shareholder distributions ([F1],[S4]). Contract manufacturing reliance minimized fixed asset intensity contributing to relatively low capex relative to revenue scale while preserving flexibility responding rapidly to demand fluctuations.

Risks on the Horizon: Supply Concentration and Competitive Pressures

A prominent vulnerability surfaces from reliance on a single contract manufacturing partner responsible for producing critical components of Sanara’s soft tissue repair products elevating operational risks related to supply disruptions or quality control mishaps potentially impairing delivery schedules amid tight hospital inventory cycles—a risk characterized within medical device supply chain concentration concerns widely documented across peer companies facing raw material scarcity or geopolitical interruptions ([S11]).

Competitive dynamics remain challenging; Sanara confronts entrenched larger players possessing extensive salesforces along multiple surgical specialties who can bundle offerings or engage pricing at scale difficult for emerging companies to counterbalance despite clinical differentiation claims manifesting through licensing intellectual property horizons ([S1],[N2]). Regulatory scrutiny also imposes complexity navigated through FDA clearances notably via the expedited but rigorous Section 510(k) pathway which governs approval timelines shaping market entry pace especially relevant for upcoming OsStic adhesive launches ([S16]-[S18]).

While currently no material litigation threatens operations ([S22]), continuous vigilance regarding stringent fraud/abuse statutes applicable within federal healthcare reimbursement environments remains mandatory given evolving enforcement policies potentially impacting advertising or reimbursement practices ([S12],[S14]).

Key Milestones and What To Watch Next

Looking ahead into mid-2026 onwards key indicators include successful regulatory approvals accompanying OsStic BioAdhesive commercial introduction alongside expanded field applications negotiated through BMI partnership potentially activating royalty streams supporting top-line growth forecasts—though explicit guidance remains undisclosed necessitating cautious monitoring around quarterly reports highlighting adoption rates post-launch ([N2],[N3],[S19]).

Additional strategic partnerships or acquisitions could emerge enabling augmentation of the product pipeline primarily directed at enhancing the "Promote" aspect of their Prepare-Promote-Protect framework while solidifying presence inside high-volume orthopedic sub-specialties frequently utilizing bioactive matrices.

Investor attention will also focus tightly upon sustained operating margin improvements translating higher revenues into bottom-line progress addressing lingering net loss headwinds documented since earlier years ([F1],[N1]). Improvements or setbacks concerning supply chain resiliency against single-source exposure will be consequential given industry volatility broadly observed recently due to pandemic-era disruptions compounded by global logistics constraints.

This analysis is based strictly on disclosed filings from Sanara MedTech Inc., supplemented by news coverage without offering investment advice or price targets. It aims solely to inform readers about historical performance trends alongside forward-looking structural shifts within the company's business model and market environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments