Braze Inc.: Balancing Rapid Growth with Persistent Losses

Braze experienced swift revenue expansion driven by subscription renewals and product investment, yet continues to face challenges from sustained operating deficits and competitive pressures.

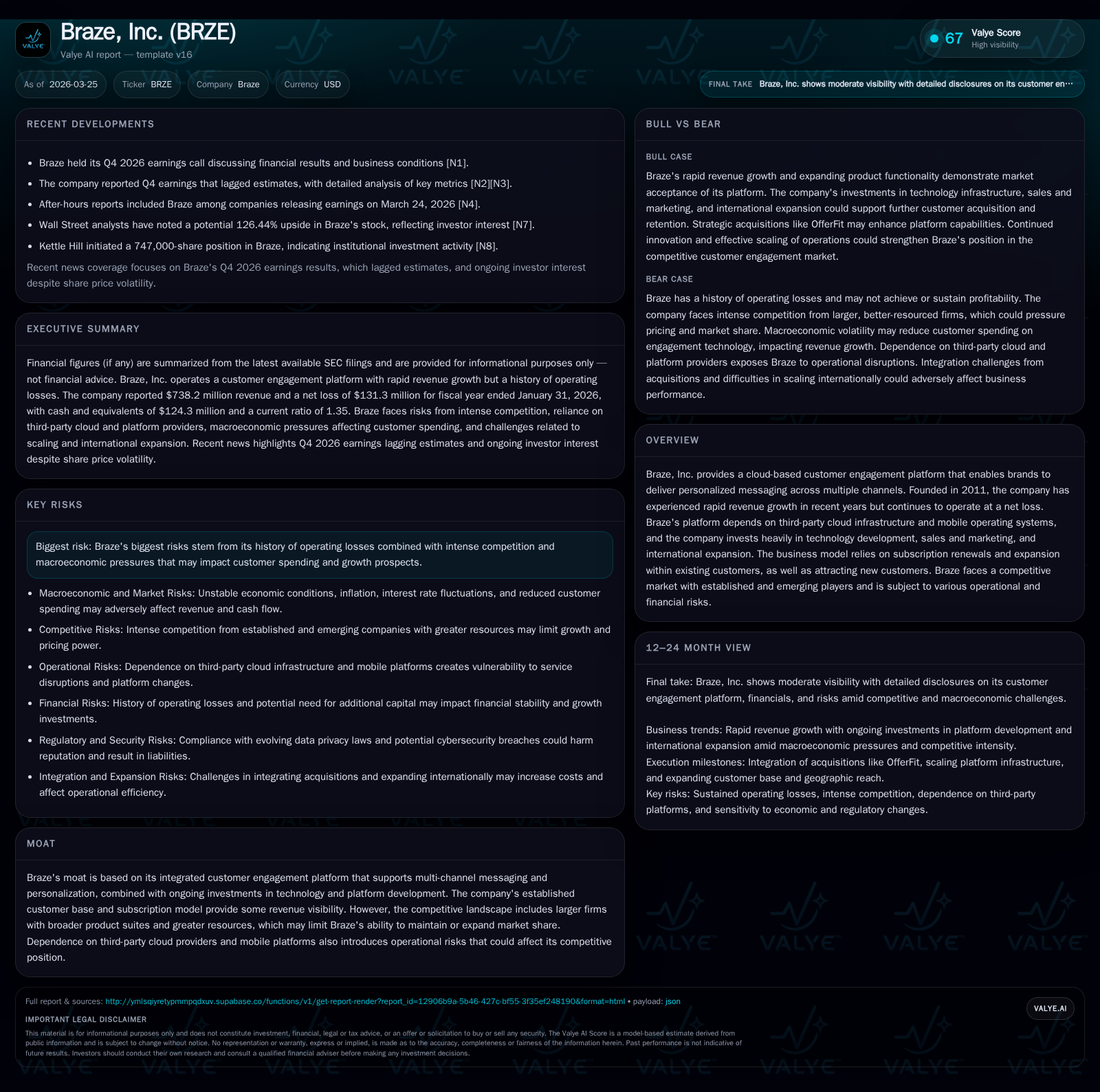

Braze, Inc. has delivered rapid top-line growth over the past several years, leveraging its cloud-based customer engagement platform and subscription model. Despite this expansion, the company remains unprofitable with a widening operating loss as it invests heavily in R&D, sales, and internationalization. Market headwinds including elongated sales cycles and cost pressures have recently weighed on sentiment, while Braze continues to navigate complex regulatory and competitive environments. Capital allocation reflects improving cash flows but a lack of profitability constrains returns. Key near-term metrics such as renewal rates and margin trends warrant close monitoring for inflection signs.

Recap of Historical Financial Trajectory and Growth Drivers

Since its founding in 2011, Braze has capitalized on increasing enterprise demand for personalized omni-channel customer engagement solutions. The company’s subscription-based model underpins most of its revenue growth via renewals and expansions within an established customer base complemented by new client acquisitions. Investment focus remains heavily tilted toward research & development (R&D), sales, marketing, and international expansion efforts.

Over the trailing four fiscal years ending January 31, 2026, Braze’s operating income has consistently been negative but relatively stable around the -$140 million mark with some fluctuation: -$148.1 million (FY2023), -$144.7 million (FY2024), -$122.2 million (FY2025), back up to -$144.8 million (FY2026) [F1]. This pattern illustrates persistent operating losses driven largely by elevated spending necessary to support platform enhancements, scale business infrastructure, and broaden market reach amidst aggressive competitors.

Concurrently, net income losses mirror this trend with a bottom line at -$139.0 million (FY2023) narrowing slightly mid-period before widening again to -$131.3 million most recently while simultaneously evolving positive cash flow dynamics (discussed later) indicate improved operational efficiency despite unprofitability [F1].

Subscription renewals remain central to sustaining revenue momentum as Braze leverages its integrated engagement platform that combines behavioral analytics with multi-channel messaging capabilities spanning mobile push notifications, email, SMS, and web channels—a complex data orchestration environment dependent on third-party cloud infrastructure providers [S16][S22]. This architecture affords some moat through platform scalability and depth of personalization options yet exposes Braze to risks from reliance on external cloud services as well as mobile OS ecosystem acceptance.

Revenue Dynamics and Operating Loss Evolution Over Four Years

A quantitative snapshot from FY2023 through FY2026 captures nuanced financial trends shaping Braze’s current standing:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -131 | 71 | -145 | 10 | -26.6% |

| 2025 | -104 | 37 | -122 | 13 | +19.7% |

| 2024 | -129 | 7 | -145 | 10 | +7.1% |

| 2023 | -139 | -22 | -148 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 62 | -21.0 | |

| 2025 | 23 | -21.8 | |

| 2024 | 165000 | -3 | -29.1 |

| 2023 | 0 | -38 | -31.2 |

Source: SEC companyfacts cache [F1].

Notice the operating loss narrowed notably between FY2024-FY2025 but reversed sharply in FY2026 by nearly 20%, signaling intensifying investment possibly tied to scaling or product launches despite positive free cash flow generation estimated at $61.85 million in FY2026 ( minus ) [F1]. Net income follows a similar volatility pattern with a marked increase in losses last year possibly reflecting transient costs or one-off expenses.

The steady rise in equity suggests successful capital raises or retained earnings accumulation despite losses. Operating cash flow’s strong improvement from negative in FY2023 to highly positive in FY2026 indicates progress on working capital management or higher recurring revenue quality supporting liquidity.

Beneath The Hood: Platform Features and Competitive Moat

Braze's technology foundation integrates a sophisticated customer engagement platform facilitating tailored messaging across mobile apps (push), emails, SMS texting and web interfaces employing granular behavioral signals and segmentation strategies—a critical factor enabling targeted personalization at scale [S16][S22]. Sector vernacular like "data orchestration" aptly describes Braze's capability to unify diverse consumer touchpoints through real-time event processing.

This integrated approach provides a competitive edge through seamless cross-channel engagement workflows; however it also ties the platform tightly to third-party cloud service providers (e.g., AWS or Google Cloud) and major mobile OS ecosystems like Apple iOS or Google Android . Such dependencies create operational vulnerabilities should these providers alter terms or introduce limitations impacting message delivery reliability or privacy compliance.

Braze is contending with entrenched incumbents that house broader marketing cloud solutions—Adobe Experience Cloud or Salesforce Marketing Cloud—that bundle customer engagement within extensive ecosystems including CRM or commerce platforms. This external pressure restricts Braze’s ability to broaden market penetration without materially expanding its own functionalities or forging strategic partnerships [S16][S22]. Emerging start-ups offering point solutions capable of rapid iteration further intensify competitive dynamics requiring accelerated innovation cycles.

Current Market Sentiments and Earnings Miss Impact

The most recent Q4 2026 earnings call disclosed that Braze missed revenue estimates causing immediate negative investor reaction ([N1],[N3]). Management commentary revealed an elongation of sales cycles attributed largely to macroeconomic headwinds affecting buyer confidence coupled with ongoing cost pressures tied to hiring and infrastructure expenditures ([N1]).

Analysts responded ambivalently—some seeing valuation downside risk due to profitability uncertainty while others point toward long-term growth potential supported by subscription renewal strength ([N7]). Notably amid the share price decline approaching 60%, dedicated funds increased stock purchases totaling over $25 million implying nuanced conviction among certain institutional investors about future recovery prospects ([N11],[N12]).

"Sales cycle lengthening" has become a theme connoting protracted deal closing times typically triggered by economic caution prolonging procurement decisions which translates into lagging near-term bookings although potentially deferred future revenue streams.

Future Growth Opportunities and Strategic Constraints

Braze continuously cites international market expansion as a strategic pillar with efforts underway targeting regions beyond North America leveraging translation/localization capabilities to attract global enterprises ([N1]; corroborated by S1/S5). Growth within verticals like retail or financial services featuring high consumer interaction frequency offers additional levers.

Yet these ambitions confront headwinds: intensified competition includes players willing to undercut pricing models especially where localized privacy policies differ influencing preferential vendor selection; additionally reliance on third-party cloud providers exacerbates operational cost exposure while regulatory uncertainties affect market confidence ([S1],[S5],[N1]).

Dependence on "subscription renewal" rates is a double-edged sword—while providing predictable revenue streams when high retention is achieved it also imposes immense pressure on continual feature enhancements meeting evolving customer demands lest churn rates accelerate undermining lifetime value .[S1]

Macroeconomic factors including inflation-induced IT budget tightenings among customers may dampen spending capacity further constraining upside growth trajectories.

Capital Allocation, Cash Flow Trends, and Shareholder Returns

Braze’s capital strategy currently prioritizes reinvestment over distributions or repurchases given its persistent net losses reported as about -$131 million in FY2026 juxtaposed against equity capital of roughly $624 million yielding an approximate negative ROE near -21% ([F1],[S7]). Operating cash flow expanded from negative territory four years ago reaching $71 million in FY2026 reflecting improved working capital discipline alongside structural recurring revenues.[F1]

Capital expenditures have moderated year-on-year falling almost 28% from FY2025 levels indicating possible efficiencies or deferment of certain infrastructure projects consistent with optimizing burn rates while maintaining platform development capacity.[F1]

Buyback activity remains negligible with only $165 thousand repurchased in FY2024 suggesting management focus fixed firmly on growth investment rather than shareholder distributions.[F1]

Free cash flow generation above $60 million currently supports runway extension although sustained profitability remains elusive necessitating further capital if scaling persists aggressively.

Regulatory, Operational, and Competitive Risk Factors

Braze operates amidst increasingly stringent data privacy laws encompassing GDPR in Europe as well as HIPAA regulations related to protected health information within the U.S., alongside many emerging jurisdictional restrictions impacting cross-border data transfers ([S4],[S5],[S6]). Failure—or perceived failure—to comply could lead to substantial fines or litigation risk potentially harming reputation.[S20]

Operational risks stem from dependence on third-party cloud hosting services along with Apple iOS/Google Android push notification policies which if altered unpredictably could disrupt messaging functionality key to user engagement consistency.

The intellectual property landscape remains contested; past patent infringement allegations that were unfounded signal latent exposure common in SaaS tech sectors given frequent inter-company patent assertion strategies.[S21]

Competition remains fierce with legacy marketing clouds bundling products more extensively plus nimble startups innovating rapidly potentially capturing niches or offering lower cost structures.[S16],[S22]

Macroeconomic uncertainty including inflationary pressures can reduce client budgets accelerating price competition thereby margin contraction possibilities linked closely with strategic adaptations noted previously.

Key Milestones Ahead: Metrics to Watch

Absent explicit forward guidance beyond qualitative outlooks ([N1],[N2]), investors should monitor key SaaS performance indicators embedded in management narratives such as:

- Dollar-based net retention rate recovery signaling stickiness of subscriptions;

- Improvement trend in operating margins evidencing cost leverage economies;

- Free cash flow stability indicating self-funded growth sustainability;

- Sales cycle duration normalization accelerating bookings;

- New client acquisition pace relative to churn dynamics emphasizing top-line durability.

Given the mixed signals from recent earnings misses balanced against ongoing sizeable investments one must watch these metrics closely for inflections before concluding sustainable profitability appears viable.

This analysis synthesizes publicly available financial filings reported through fiscal year end January 31st 2026 combined with contemporaneous news sources without extrapolating unaudited forward-looking estimates or unsupported figures. It neither constitutes investment advice nor recommendations but aims for an objective assessment grounded solely on documented evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments