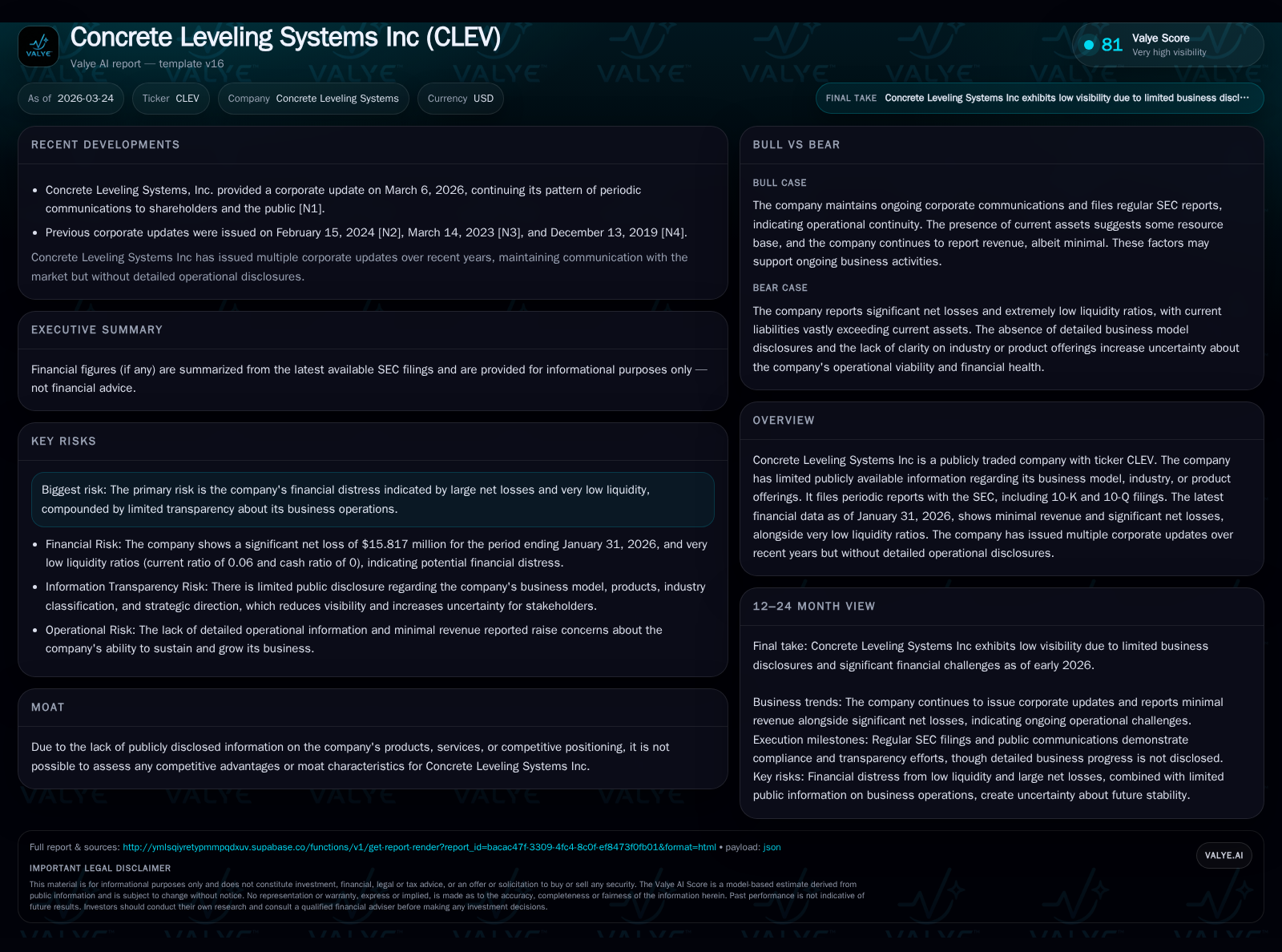

Concrete Leveling Systems Inc Faces Tight Liquidity and Revenue Retraction

Concrete Leveling Systems Inc exhibits significant financial stress marked by declining revenues, mounting losses, and critical liquidity shortages undermining its operational stability.

Concrete Leveling Systems Inc has undergone persistent revenue contraction and escalating net losses over the past four fiscal years, with its latest reported revenue dropping nearly 10% year-over-year to a mere $703. Operating cash flow remains virtually nonexistent, highlighting minimal commercial traction. The company's balance sheet reveals an acute liquidity crisis reflected in an alarmingly low current ratio of approximately 0.06, raising solvency concerns. Compounding this financial fragility is a notable opacity in corporate governance and transparency following leadership disruptions and auditor transitions. Future growth prospects appear bleak given the absence of strategic disclosures or turnaround initiatives, necessitating vigilant monitoring of forthcoming filings and capital structure developments.

Revenue and Profit Trends Reveal Ongoing Contraction

Concrete Leveling Systems Inc has exhibited a clear and steady contraction in operational scale over the last four fiscal years ending July 31. Revenue declined from $1,082 in FY2022 to $703 by FY2025, marking a nearly 35% erosion over this period with a notable -9.6% YoY drop most recently [F1]. This shrinking top line is accompanied by worsening operating losses that rose from -$39,078 in FY2022 to -$51,113 in FY2025; operating income has failed to approach break-even levels at any point [F1]. Net income reflects similarly dire trends: despite slight improvement from -$65,985 in FY2024 to -$61,390 in FY2025, the company remains deeply unprofitable [F1].

Operating cash flow has traditionally lagged operating losses but saw a near-neutral figure of -$63 during FY2025 compared to significant cash burn prior [F1]. Though this may indicate marginal stabilization at cash level activities, the amounts are minuscule and highlight minimal commercial momentum.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | ||||||

| 2025 | 703 | -61390 | -63 | -51113 | -9.6% | +7.0% |

| 2024 | 778 | -65985 | -49781 | -48800 | -10.6% | -22.8% |

| 2023 | 870 | -53730 | -44433 | -43493 | -19.6% | -9.7% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2026 | |

| 2025 | 9.9 |

| 2024 | 11.8 |

| 2023 | 10.9 |

Source: SEC companyfacts cache [F1].

FY data ends July each year; CFO for FY2025 indicates negligible operational cash burn compared to prior years [F1].

Drivers Behind the Contracting Top Line and Profitability Setbacks

The consistent revenue decline aligns with limited disclosures regarding Concrete Leveling Systems' operations or product offerings [N1][S1][S2]. Management commentary via recent corporate updates reiterates persistent financial distress but lacks substantive explanation on market dynamics or internal strategic levers [N1]. The scant top-line figures suggest either severe demand contraction or inability to execute on commercial activities effectively.

Liquidity constraints disclosed throughout filings have further restricted operational capacity and growth investment possibilities [S8][S9]. Without transparency into segments or customers served, it is challenging to diagnose root causes of underperformance beyond structural financial deficiencies.

The company’s failure to generate positive operating margins despite ongoing expenses signals entrenched structural challenges rather than cyclical weakness [F1]. Persistent net losses also reflect these hurdles.

Liquidity Challenges Deepen – Exploring Capital Structure Dynamics

Concrete Leveling Systems confronts profound liquidity shortfalls materially undermining near-term viability considerations. As of January 31, 2026, current assets stood at only $40,910 versus crushing current liabilities totaling $662,730—a ratio calculation yielding an extremely precarious current ratio near 0.06 [F1][S14][S16]. This imbalance exposes acute working capital deficits that critically impair day-to-day operations and creditor confidence.

Cash and equivalents were measured at merely $516 as of April 30, 2023 indicating an almost complete depletion of readily accessible funds [F1].

Such capital structure stress typically forces reliance on external financing or restructuring processes; however, no confirmed events or raised capital have been disclosed thus far [N1][S13][S14]. Dismissal of audit firm Astra Audit & Advisory LLC followed by engagement of Stephano Slack LLC as new independent auditor potentially signals attempts at governance recalibration amidst fiscal stress [S16], though no operational turnaround announcements accompanied this transition.

Overall solvency risk remains elevated given pervasive negative equity ($-621,649 at FY2025 end) with no resolution pathway made public [F1]. This degree of imbalance classifies Concrete Leveling Systems firmly as a microcap distressed entity struggling for sustainable liquidity.

Corporate Governance Changes and Transparency Issues

Corporate governance has been unsettled recently due mainly to unforeseen personnel changes and audit disruptions. The unexpected death of long-serving director Secretary Eugene H. Swearengin on June 13, 2025 removed institutional knowledge critical for continuity; his roles have been temporarily assumed without permanent replacement identified yet [S17].

Simultaneously, the company replaced independent registered public accountant Astra Audit & Advisory LLC with Stephano Slack LLC effective September 22, 2025 after routine transitions without adverse audit opinions reported for prior years [S16]. However, lack of explanatory context for this shift may heighten market skepticism especially given overall data opacity.

Regulatory filings continue with standard disclosures but omit granular operational descriptions—typical for smaller reporting companies but problematic amid existing financial frailty [S1][N1]. Such gaps exacerbate uncertainty about business fundamentals and strategic direction.

Assessing Future Growth Prospects Amid Operational Opacity

No explicit guidance or forward-looking projections have been provided in recent disclosures or corporate communications [N1][S2], leaving future growth drivers speculative at best. The absence of any new product launches or service diversification initiatives hints that sustainable earnings improvements remain elusive.

Continuous losses and negligible operating cash flows diminish feasibility for internal expansion funding while liquidity shortages limit external raising options. These factors collectively suggest limited short-to-medium term growth prospects unless management unveils credible turnarounds or capital infusion strategies.

Furthermore, no moat characteristics are discernible due to the lack of operational detail impeding competitive positioning assessment .

Key Milestones to Watch Following Recent Corporate Updates

Investors should focus on scheduled filings such as upcoming quarterly or annual reports which may reveal updated liquidity status or auditor communications confirming independent assessments post-accounting firm transition [N1][S2].

Potential milestones include:

- Publication of FY2026 annual report evidencing any financial improvement or further deterioration.

- Any announcements regarding capital raises or restructuring plans addressing working capital deficits.

- Disclosure of board appointments filling governance vacancies created by Mr. Swearengin’s passing.

- Auditor’s opinions on going concern status post-September 2025 engagement. These events will significantly influence assessment of structural recovery capability versus continued distress risks.

Capital Allocation Review: Absence of Positive Cash Flows and Return Metrics

Concrete Leveling Systems has demonstrated persistent negative free cash flow as operating cash flow barely registers near zero (-$63 most recently), while capital expenditures data is not explicitly detailed but inferred minimal given microcap scale [F1]. This leaves no evidence for organic reinvestment or expansion spending fueling future gains.

Equity stands profoundly negative (~-$621k), resulting largely from cumulative net losses eroding shareholder value over time [F1]. Conventional return metrics like ROE become mathematically distorted taking positive percentage due to negative denominator rather than representing genuine profitability—a phenomenon occasionally termed "backwards ROE" requiring cautious interpretation.

No dividends or buyback programs have been reported since these would be nonviable against such loss-making circumstances [F1]. Resultantly, shareholder returns are notably absent reflecting the company’s severe capital constraints.

Analyst Perspective: What Investors Should Monitor Going Forward

Given Concrete Leveling Systems’ combination of deteriorated revenue streams, exacerbated liquidity constraints evidenced by a critically weak current ratio (~0.06), and governance opacity intensified by auditor turnovers and director departure, several key indicators merit close observation:

- Liquidity position shifts disclosed in forthcoming SEC periodic filings are paramount for evaluating survival prospects.

- Auditor reports potentially flagging material uncertainties about going concern status post-accounting firm change may signal intensifying financial distress.

- Any management communications outlining restructuring measures or new financing avenues could materially alter outlooks.

- Updates on regulatory compliance issues including litigation risk sections found consistently across recent forms (see [S3]-[S7]) provide risk framing relevant to microcap distressed environments.

- Board composition changes resolving vacancy from Mr. Swearengin’s passing could enhance governance stability if promptly addressed. Overall transparency improvements will be essential to moving beyond speculation towards validated performance appraisal.

Concrete Leveling Systems currently exemplifies typical microcap companies trapped within a tight financial straitjacket compounded by informational opacity that complicates thorough valuation efforts outside discrete quantitative metrics presented here.

Disclaimer: This analysis is based exclusively on publicly available data up to March 24, 2026 including SEC filings and news releases without speculative assumptions regarding future performance or undisclosed business developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments