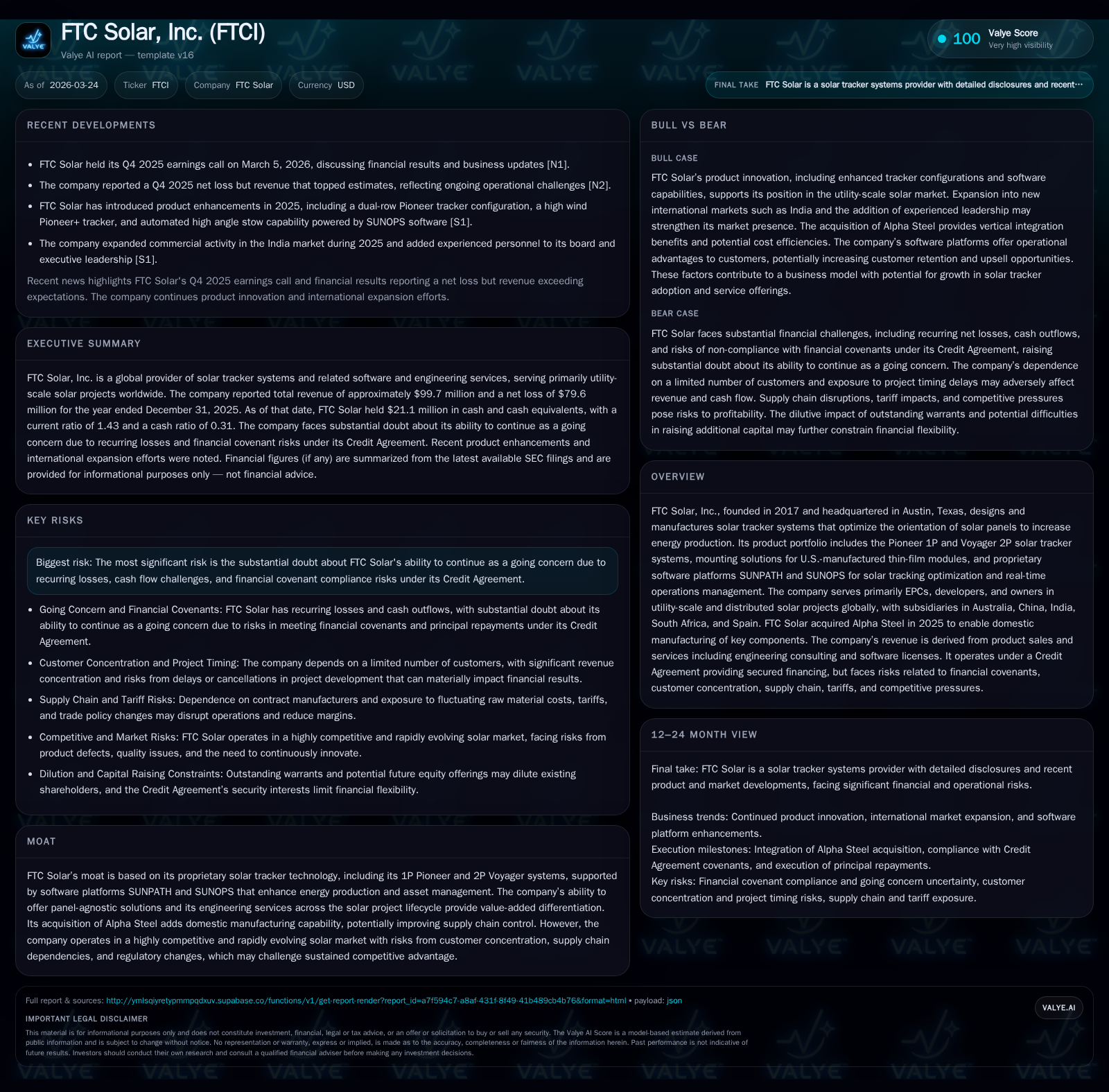

FTC Solar’s US Manufacturing Shift and Credit Risks Shape 2025 Financial Trajectory

FTC Solar grapples with growth-driven losses, expanding U.S. manufacturing, and stringent credit covenants in a volatile solar market.

FTC Solar, Inc. reported substantial revenue growth in 2025 driven by increased MW deployment and expansion into domestic manufacturing through its acquisition of Alpha Steel. Despite these operational gains and product diversification supported by proprietary software platforms, the company remains unprofitable with sizable net losses and negative operating cash flows, reflecting challenges in project timing and tariff impacts. Heightened credit agreement covenants and covenant breaches pose ongoing liquidity concerns, casting substantial doubt on the company’s ability to continue as a going concern beyond 2026. Customer concentration and supply chain risks further complicate the outlook.

Company Overview and Historical Performance

Founded in 2017 and headquartered in Austin, Texas, FTC Solar specializes in solar tracker systems designed to optimize panel orientation for enhanced energy capture. Its flagship products include the one module-in-portrait Pioneer (1P) and two modules-in-portrait Voyager (2P) tracking systems. Complemented by proprietary software platforms SUNPATH for optimal tracking configurations and SUNOPS for real-time operations management, FTC Solar serves primarily EPCs, developers, and owners engaged in utility-scale solar projects worldwide.[S21]

Financially, FTC Solar’s historical performance reveals persistent operating losses exacerbated by project timing uncertainty and fluctuating raw material costs affected by tariffs.[F1][S1] Revenue more than doubled from $47.4 million in 2024 to approximately $99.7 million in 2025.[F1][S9]

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -80 | -33 | -35 | 1129000 | -63.7% |

| 2024 | -49 | -35 | -53 | 1645000 | +3.3% |

| 2023 | -50 | -53 | -51 | 816000 | +49.5% |

| 2022 | -100 | -55 | -100 | 985000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -35 | 185.2 | |

| 2024 | -36 | -255.3 | |

| 2023 | 0 | -53 | -80.5 |

| 2022 | 0 | -55 | -149.9 |

Source: SEC companyfacts cache [F1].

Data extracted from fiscal year-end filings dated March 24, 2026.

Operating losses narrowed roughly by one-third year-over-year but remain significant at over $35 million negative.[F1] Net losses expanded substantially influenced by tariff accruals related to denied Customs & Border Protection assessments totaling around $2 million.[S9][S12]

The balance sheet shows distress with an equity deficit of approximately $42.9 million as of end-2025 compared to positive equity above $19 million the prior year.[F1]

Key Drivers Behind Growth

Revenue Expansion

Growth was driven by higher megawatt output—production increased roughly 168% year-over-year—and a corresponding surge in shipping/logistics activity by approximately 76%.[S9] Product sales accounted for around 80% of revenue while service revenues including engineering consulting and software licensing made up the rest.[S4]

Acquisition-Driven Manufacturing Shift

In November 2025, FTC Solar acquired Alpha Steel LLC enabling domestic production of key tracker components such as torque tubes and rails previously outsourced entirely.[S16] This move supports customers seeking U.S.-based content amid tariff volatility affecting steel/aluminum inputs sourced internationally (57% of purchase orders were U.S.-based suppliers with notable sourcing also from India and China).[S16][S24]

Software Platforms & Service Expansion

Proprietary software like SUNPATH and SUNOPS complement hardware sales by enabling optimized tracking configurations and real-time asset management, supporting scalable service revenues globally.[S21]

Profitability & Cash Flow Challenges

Tariffs imposed during the period increased product costs that could not always be passed fully onto customers due to fixed contract pricing or competition.[S2][S9] Project development delays caused by permit issues or financing difficulties also constrained margins resulting in a gross loss despite marked improvement over prior years.[F1][S10][S17]

Operating cash flow remains negative despite some progress; capital expenditures are modest but free cash flow continues deeply negative reflecting ongoing investment outlays exceeding cash collections.[F1]

Customer concentration is high—with four customers accounting for a large revenue share (~70%), three representing over half of receivables—payment delays or cancellations can cause material adverse impacts.[S10][S20]

Credit Agreement Covenants & Going Concern Risks

FTC Solar's credit facility allows up to $75 million via staggered term loans maturing July 2029,[S5][S19] but financial covenants require minimum unrestricted cash balances ($15 million mid-2026), escalating quarterly revenues ($25 million to $75 million across second half of 2026),[S18] EBITDA floors starting at $10 million from full year-end 2026,[S22][S28] direct tracker margin thresholds,[S18] and purchase order targets deferred until Q1 2027.[S3]

Breach of covenants occurred previously prompting lender waivers; however substantial doubt about continuing as a going concern within twelve months remains explicitly disclosed.[S1][S6][S8]

The company plans potential capital raises through ATM stock sales if needed alongside cost optimization including shifting headcount toward lower-cost regions.[S22]

Growth Outlook & Risks

Growth relies on expanding utility-scale solar projects driven by:

- Declining solar PV module costs tempered currently by tariffs[S16]

- Government incentives like tax credits and Renewable Portfolio Standards[S16]

- Rising electricity demand due to data center expansion and AI adoption[S16]

- Advances in panel efficiency aligned with proprietary tracker tech[S21]

- Expanding software service offerings enhancing asset optimization[S21]

- Geographic expansion including new commercial activity launched in India late-2025 alongside global presence across Australia, China, South Africa, Spain[S4]

Risks include intense competition,[S1] supply chain dependency on limited contract manufacturers,[S24] customer payment delays consistent with past write-offs (~$8.9 million recorded previously)[S20], ongoing tariff uncertainties,[S2][S27] legal disputes such as litigation against BayWa r.e.,[S12] and technological obsolescence risk if innovation lags competitors.[S23]

Returns & Capital Allocation Trends

Negative returns persist: approximate ROE based on latest net loss relative to equity implies severe capital erosion exceeding -185%.[F1] No share repurchases have occurred since fiscal year-end 2021 reflecting liquidity preservation needs.[F1]

Capital expenditures remain low under $1.2 million despite expanded manufacturing capabilities indicating incremental investments rather than large-scale expansions.[F1] Cash inflows remain insufficient to generate positive free cash flow necessitating external financing.

Milestones & Monitoring Points Ahead

Key metrics to watch include:

- Quarterly revenue progression against credit covenant benchmarks [$25M+ Q2'26 to $75M Q4'26+],[S18]

- Gross margin recovery signaling pricing power amidst cost inflation[S9]

- Operating expense efficiency amid workforce shifts[S15]

- Movement toward positive operating cash flow factoring receivables cycles[F1]

- Integration progress of Alpha Steel boosting domestic supply resilience[S16]

- Resolution status of key litigations impacting contracts[S12]

- Outcomes of capital raising or covenant renegotiations shaping liquidity runway[S6][S22]

- Order pipeline strength ensuring compliance with escalating purchase order covenants starting Q1'27[S18]

Conclusion

FTC Solar navigates an inflection point balancing near doubling revenues against persistent financial deficits driven by project timing volatility, tariff-related cost pressures, concentrated customer exposure, supply chain dependencies despite new U.S.-based manufacturing capacity, stringent credit facility terms requiring ambitious milestones, and ongoing liquidity risks flagged in SEC disclosures.

While proprietary product/software differentiation plus geographic expansion offer pathways toward sustainable profitability, robust execution will be critical amid tightening financial covenants.

Disclaimer: This analysis is based solely on publicly available information as of March 24, 2026, including SEC filings [F1], [S#], [N#]. It does not constitute investment advice or recommendations regarding FTC Solar securities or any other entity mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments