TGE Value Creative Solutions Corp: Evaluating the SPAC Journey Before a Business Combination

An early-stage SPAC with $150 million raised and no operations, focused on completing a strategic business combination.

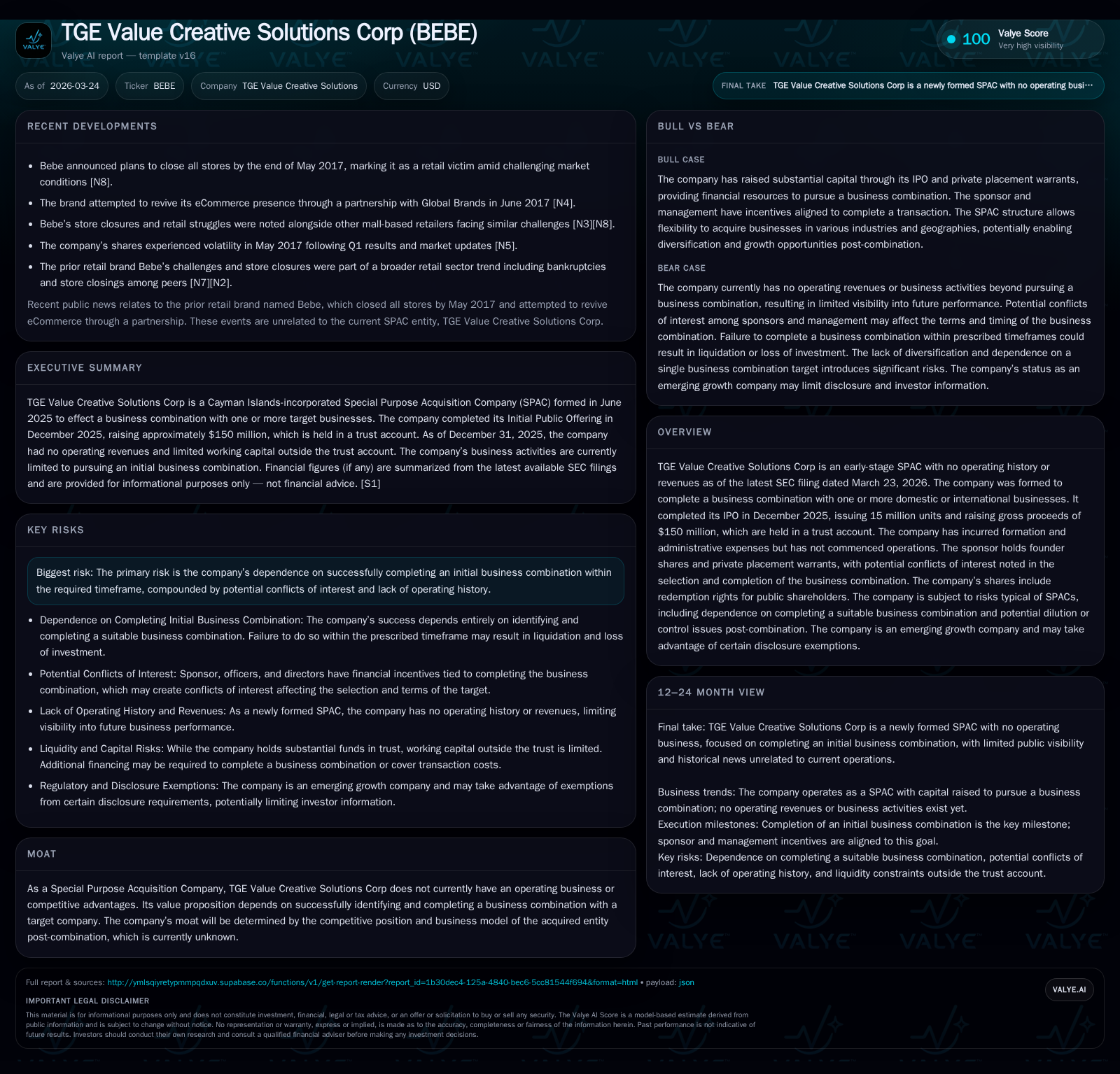

TGE Value Creative Solutions Corp (BEBE) is a Cayman Islands-based special purpose acquisition company (SPAC) formed in mid-2025 to identify and merge with one or more target businesses. It completed its IPO in December 2025, raising $150 million which is held in trust pending an initial business combination. The company has incurred formation and administrative expenses but has not generated any revenues or conducted operations to date. Sponsor founder shares and private placement warrants create potential conflicts around deal selection, while redemption rights and market conditions introduce additional risks. Growth prospects hinge entirely on successfully closing a timely business combination, which remains uncertain as no targets have been selected so far.

Formational Growth: From Incorporation to IPO Completion

TGE Value Creative Solutions Corp was incorporated on June 13, 2025, in the Cayman Islands as an exempted limited liability company designed specifically as a blank check company or SPAC. Its core mandate is to identify and complete a business combination via merger, share exchange, or asset acquisition with one or more businesses domestically or internationally [S1].

The company launched its initial public offering on December 22, 2025, issuing 15 million units priced at $10 each, thereby generating gross proceeds of approximately $150 million. Each unit comprises one Class A ordinary share and one-half of one redeemable warrant exercisable at $11.50 per share [S1][S3]. Concurrently, the sponsor acquired 5.3 million private placement warrants at $0.50 each, while the underwriter purchased an additional approximately 1.76 million warrants at $0.85 apiece—collecting aggregate proceeds of about $4.15 million outside the IPO funds [S1].

Offering costs totaled near $9.79 million including underwriter fees of which $6 million are deferred under standard SPAC structures pending successful business combination completion [S1][S4]. After deducting underwriting discounts (approximately $3 million) and offering expenses—excluding the deferred component—the full $150 million raised from public investors was deposited into a segregated trust account as per regulatory requirements aimed at protecting shareholder funds pre-combination [S1][S5].

The sponsor also holds founder shares totaling 5.75 million granted at nominal cost ($25,000), subject to forfeiture if no business combination occurs [S1]. A portion of these founder shares was redistributed to officers and directors pre-IPO but part was surrendered back at offering close [S1]. This arrangement creates alignment issues given the sponsor’s investment is essentially worthless without transaction execution.

Assessing Organizational Costs and Initial Financial Position

During the inception-to-December 31, 2025 period, TGE Value Creative Solutions incurred primarily organizational and administrative expenses totaling approximately $89,950 aimed at legal compliance, SEC filings, auditing preparation, and preliminary due diligence activities typical for nascent SPACs preparing for future acquisitions [S1][S10].

Operating revenues were nonexistent as the entity has yet to engage in any substantive commercial activity or earn income outside nominal trust account interest. The net income recorded of about $145,831 for the period resulted primarily from interest income ($109,781) earned on investments held within the trust—money market funds classified as trading securities—and a positive adjustment related to over-allotment liability changes ($126,000), partially offset by costs [F1][S1][S5][S8].

Cash balances split between approximately $683,798 held outside the trust for working capital purposes versus about $150.1 million locked in the trust indicate solid liquidity buffers appropriate for ongoing operational needs during target search phase [F1][S5][S8]. Working capital stood at roughly $349,767 underscoring runway sufficiency for pre-business combination activities without need for additional financing so far [F1][S6].

| Metric | Amount (USD) | Period Ended |

|---|---|---|

| Net Income | 145,831 | Dec 31, 2025 |

| Interest Income | 109,781 | Dec 31, 2025 |

| Offering Costs | ~9.79 million | Dec 31, 2025 |

| Cash Outside Trust | 683,798 | Dec 31, 2025 |

| Trust Account Balance | ~150.1 million | Dec 31, 2025 |

| Working Capital | ~349,767 | Dec 31, 2025 |

Capital Structure and Liquidity Stance With Sponsor Participation

The capital structure features standard SPAC elements: public shares with redemption rights backed by the trust account assets; founder shares unredeemable but dilutive post-business combination; redeemable public warrants; sponsor-held private placement warrants; and deferred underwriting fees contingent on deal completion [S4][S6][S7].

A noteworthy structural feature is the deferred underwriting fee of up to $6 million reserved within the trust account payable only once a business combination closes—ensuring alignment between underwriters’ interests and deal consummation without risking premature cash depletion [S4]. Additionally, monthly administrative services fees of up to $2,500 payable to the sponsor commenced post-listing supporting office space and secretarial services essential for deal execution [S4][S7].

The sponsor extended an unsecured promissory note facility capped at $250K (non-interest bearing), of which approximately $150K remained outstanding as of fiscal year-end for funding formation costs—a mechanism commonly used in SPACs to cover interim expenses without involving third-party lenders or dilutive equity issuances [S7]. Registration rights agreements afford holders of founder shares and private placement warrants opportunities to demand up to three registrations to facilitate resale after lock-up periods end [S4][S7]. Overall liquidity management emphasizes preserving cash outside the trust solely for working capital while ensuring robust protection for shareholders’ principal within the trust.

Risk Profile: Key Conflict-of-Interest and Timing Pressures

As is typical for early-stage SPACs like TGE Value Creative Solutions Corp., dependency on timely closing of an initial business combination by a preset deadline—in this case December 22, 2027—is paramount. Failure triggers mandatory winding up and dissolution with proceeds distributed pro rata from trust accounts subject to regulatory constraints [S1][S18].

Sponsor incentives introduce conflict-of-interest risks since their founder shares and private placement warrants become worthless absent transaction completion while public shareholders can redeem shares potentially diluting sponsor control or complicating deal financing [S1][S14][S18]. This dynamic pressures sponsors towards deal consummation near deadline possibly at disadvantageous terms unless mitigated by fiduciary oversight.

Additional systemic risks stem from macroeconomic conditions including geopolitical instability referenced through ongoing Russia-Ukraine conflict effects that may impact currency fluctuations if non-U.S. targets are pursued—an important consideration given no targets have yet been identified but international deals remain possible [S17][S22]. Moreover, cybersecurity vulnerabilities noted underscore operational risks due to limited investments in data security protections typical of nascent enterprises prior to substantive scale-up [S22]. Regulatory changes continue introducing compliance complexity elevating general administrative costs.

Prospective Growth Pathways and Business Combination Parameters

Growth prospects remain theoretical until TGE identifies suitable acquisition targets. The proposed model relies heavily on leveraging the substantial IPO proceeds combined with potential debt financing or equity issuance tailored around deal structure specifics negotiated with prospective targets or partners post-combination [S1][S24].

While details on pipeline candidates are undisclosed currently, TGE retains flexibility to execute either single or multiple simultaneous transactions subject to SEC accounting requirements necessitating consolidated financials when multiple targets are acquired concurrently—a complexity sometimes disruptive depending on seller alignment and transaction timing [S24]. Lender waivers protecting trust funds enhance confidence that any debt incurred will not diminish redemption values available to public shareholders post-merger completing obligations safeguarding shareholder interests amidst leverage considerations [S18].

The ability to relocate domicile post-combination also affords operational latitude but introduces jurisdictional legal enforcement variances affecting contract integrity—a factor influencing choice of final corporate location after deal closure according to stated risk disclosures [S17].

Capital Allocation Strategy Amid Pending Transaction Risks

Capital deployment since inception has been conservative with zero dividends declared or share repurchases conducted reflecting prudent stewardship typical during pre-operating SPAC phases where IPO proceeds await transaction utilization within stringent escrow-like trust accounts [F1][S20][S25]. All fundraising cash remains dedicated within regulated trusts subject primarily to redemption obligations by public shareholders exercising put rights upon approval votes or tender offers connected with business combinations [S25].

Given absence of operating revenues currently there are no returns metrics such as ROE or free cash flow available; instead focus lies exclusively on managing administrative overhead consumption financed through segregated working capital reserves independent from IPO escrowed amounts representing core value preservation mechanism built into SPAC frameworks nationally recognized by regulators across exchanges supporting this vehicle type.

What Investors Should Watch: Triggers for Unlocking Shareholder Value

With no announced targets so far nor formal guidance beyond regulatory deadlines established at time of IPO launch investors must monitor several critical indicators:

- Formal announcements regarding potential targets entering into definitive agreements signal operational momentum toward closing deals.

- Any proposed amendments or waiver requests extending initial business combination deadlines beyond December 22, 2027 bear importance since failure prompts liquidation.

- Redemption levels ahead of shareholder votes on announced deals provide insight into confidence levels influencing available merger funding capacity.

- Progress around registration rights exercises may denote insiders’ reflections on anticipated liquidity events post-combination.

- Noticeable shifts in geopolitical risk environments or capital market volatility impacting financing feasibility.

Collectively these signals will elucidate how TGE Value Creative Solutions navigates early inherent uncertainties tied uniquely to its SPAC stage lifecycle emphasizing that eventual value must derive from astute target selection execution rather than legacy operations or prior earnings track record.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments