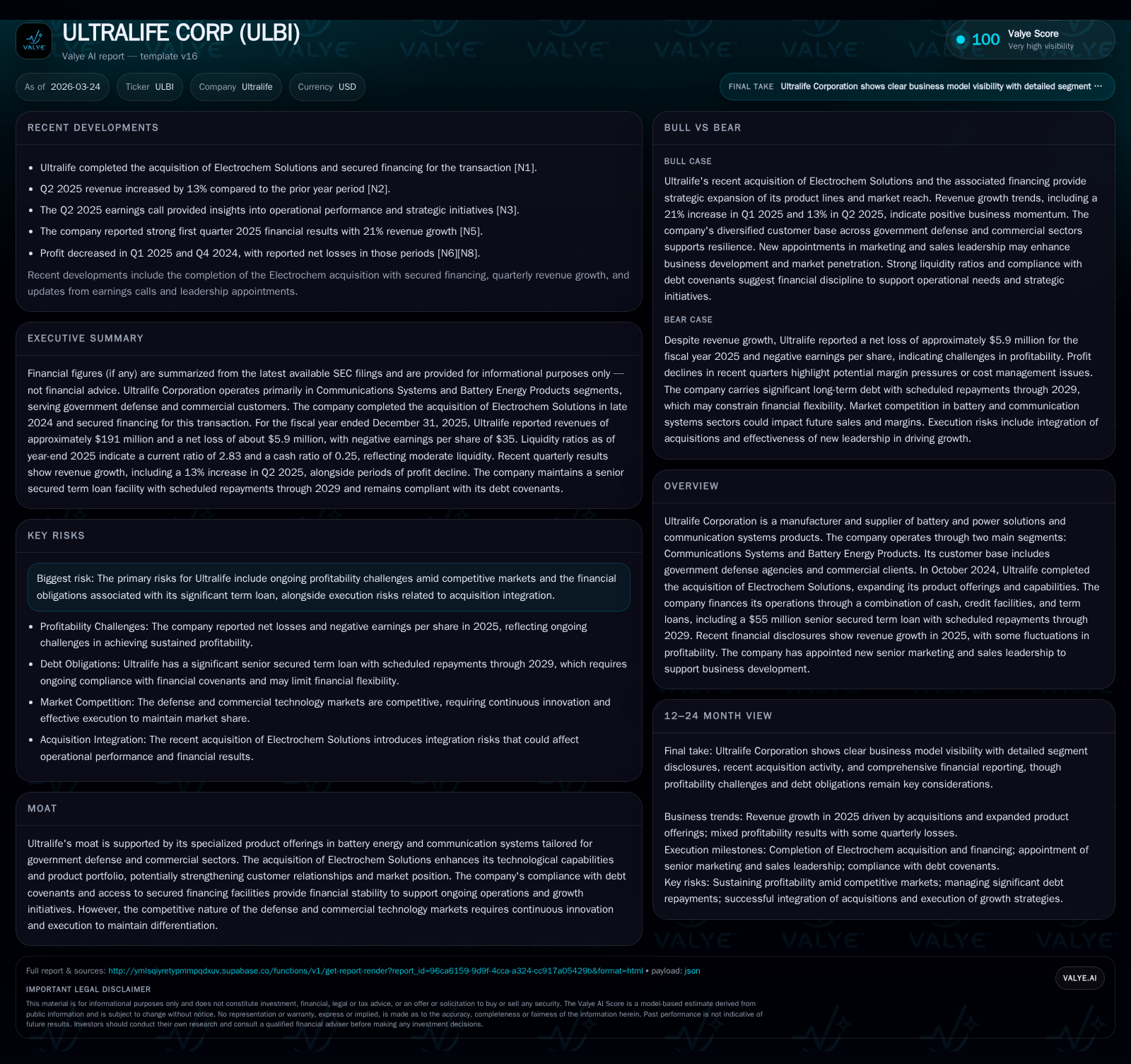

Ultralife Corp Grapples with Profitability and Leverage Post-Electrochem Acquisition

Revenue growth driven by acquisition contrasts with operating losses and elevated debt service obligations.

Ultralife Corporation expanded its scale and product offerings through the October 2024 purchase of Electrochem Solutions, driving revenue growth of over 16% in 2025. However, the integration has coincided with a swing into operating loss amid margin pressures and elevated interest expenses from a $55 million secured term loan. While cash flow remains positive, the company faces execution risks related to acquisition integration and a concentrated customer base heavily reliant on defense contracts. Capital allocation has prioritized financing growth initiatives, with no recent share repurchases or dividends.

Company Overview

Ultralife Corporation designs and manufactures specialized batteries, power solutions, and communications systems that primarily serve government defense agencies alongside commercial clients globally. The company's business split centers on two segments: Battery Energy Products and Communications Systems, with substantial sales generated from U.S. and foreign military contracts as well as prime defense contractors such as L3Harris Technologies which accounted for approximately 27% of revenues in 2025 [S1][F1].

In October 2024, Ultralife completed the strategic acquisition of Electrochem Solutions, a Massachusetts-based manufacturer known for primary lithium metal batteries and ultracapacitor cells used in critical industrial and defense applications [N1][S14][S16]. This marked an important expansion of Ultralife's product suite and customer base, particularly extending its reach into adjacent markets demanding high reliability.

Historical Performance

The company showed consistent revenue growth over recent years, accelerating notably post-acquisition:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 191 | -6 | 11 | -6 | +16.2% | -193.4% |

| 2024 | 164 | 6 | 17 | 10 | +3.7% | -12.3% |

| 2023 | 159 | 7 | 2 | 9 | +20.3% | +6147.9% |

| 2022 | 132 | 0 | -1 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 7 | -4.5 |

| 2024 | 15 | 4.7 |

| 2023 | -1 | 5.7 |

| 2022 | -3 | -0.1 |

Source: SEC companyfacts cache [F1].

Ultralife posted steady revenue increases driven by existing product demand and new market penetration strategies until reaching a significant inflection point in late-2024 when Electrochem was acquired.

Despite top-line expansion in fiscal year 2025 (+16.2%), operating income collapsed into negative territory (-$5.9 million), reversing prior profitability gains reported in both full years 2023 and especially strong year-end results in 2024 ($9.97 million operating profit). This swing mainly reflected acquisition-related costs including amortization expenses on purchased intangibles ($535k over nine months), increased cost of sales due to inventory step-ups ($120k), consulting fees for integration processes ($54k), and general expense inflation amid supply chain complexities documented through post-pandemic industry-wide inflationary disruptions [S1][S12][S16].

Net income correspondingly shifted from profits to losses by nearly the same magnitude (-$5.9 million vs prior +$6.3 million).

Cash flow from operations remained healthy at ~$11 million despite earnings shortfalls — highlighting solid working capital management even as capital expenditures doubled compared to prior year ($3.9 million vs $1.9 million) reflective of investment in manufacturing capabilities potentially linked to scaling opportunities unlocked by Electrochem’s addition.

Capital Structure and Liquidity

Ultralife finances its operations primarily via cash flows supplemented by debt instruments notably including a five-year $55 million senior secured term loan entered on October 31, 2024 coincident with the acquisition closing [S8][S14][S16]. The loan requires quarterly principal repayments starting Q1 ’25 with full repayment expected by Oct ’29 or earlier prepayment subject to notification.

Key terms include variable interest rates indexed to benchmarks plus margin adjusted per leverage tiers; as of September ’25 effective rate was approximately 6.62%. The debt is collateralized by substantially all company assets forming an enforceable lien for the lender KeyBank National Association.

At September ’25 end:

- Term loan principal outstanding was roughly $50.9 million (including current portion ~$3.8 million),

- No amounts drawn on revolving credit facility,

- The company complied fully with all covenant ratios — consolidated fixed charge coverage above minimum threshold (≥1.15x), senior leverage ratio below required limits (<3.50x tapering downward annually) [S4][S6][S21].

Current liabilities stood at about $37 million versus current assets exceeding $105 million yielding a favorable current ratio near ~2.83x providing liquidity cushion amid operational fluctuations.

Strategic Initiatives and Brand Consolidation

Alongside acquisition integration steps Ultralife undertook comprehensive rebranding measures launched October ’25 consolidating multiple sub-brands under unified “Ultralife” nomenclature aiming at streamlined market presence and simplified messaging across global geographies [S1].

This initiative involved de-emphasizing legacy trademarks including Accutronics, Southwest Electronic Energy, Excell Battery Group among others while retaining the Electrochem brand selectively for key products like primary cells — reinforcing continuity for existing customers while signaling holistic corporate alignment.

New leadership hires in sales & marketing sectors signal management focus on leveraging cross-selling opportunities tapping into Electrochem’s complementary technology base particularly targeting energy-dense lithium primary cells alongside ultracapacitors critical for defense-related portable power systems.

Growth Prospects and Risks

Ultralife’s future growth dynamics hinge critically on several factors:

- Full commercial synergy realization from Electrochem integration including vertical manufacturing optimizations poised to enhance gross margins through lean initiatives,

- Cross-selling expansions penetrating underserved adjacent markets requiring high-reliability battery chemistries not easily substituted,

- Stability or increase in U.S./foreign military spending sustaining significant contract volumes given DoD accounts comprised ~31% of Ultralife’s revenue directly or indirectly through large prime contractors [S1],

- Market conditions that continue exhibiting tariff impacts alongside persistent albeit moderating supply chain constraints influencing input costs,

- Execution risk related to assimilating diverse product lines without disrupting quality or customer service,

- Financial risk tied to servicing material term debt given profit compression observed during early integration phase.

Management disclosed no formal guidance but highlighted intention for margin improvements paired with investments underpinning long-term value creation [N1][S3]. No dividends were declared nor share buybacks reported beyond historical modest repurchase activity before COVID era (last notable buyback circa FY2019) implying reinvestment priority over capital returns currently [F1].

Returns and Capital Allocation Assessment

Approximated return metrics show subdued ROE near -4.5% based on net loss relative to equity base of approximately $130 million at fiscal year-end '25 demonstrating transitional challenges post-acquisition despite solid equity funding levels maintained since prior years.

Operating cash flow generation remains robust buffering discretionary investment capacity consistent with ongoing capex scale-up projects aimed at enhancing capacity utilization.

Capital allocation decisions favor deleveraging cautiously balanced against growth funding rather than shareholder distributions or aggressive buybacks reflecting prudence given debt profile and profitability recovery requirements.

Summary Table: Annual Financial Snapshot Selected Metrics(FY USD thousands)

| FY | Revenue | Oper Inc | Net Income | CFO | Capex |

|---|---|---|---|---|---|

| 2025 | $191,159K | $(5,902K) | $(5,898K) | $10,990K | $3,872K |

| 2024 | $164,456K | $9,965K | $6,312K | $16,636K | $1,932K |

| 2023 | $158,644K | $9,475K | $7,197K | $1,929K | $2,552K |

| 2022 | $131,840K | $129K | $(119K) | - $1,263K | $1,679K |

Capex includes investments aimed at expanding manufacturing footprints post-acquisition.

Disclaimer: This analysis is based solely on publicly available information extracted from SEC filings and news sources as of March-April 2026 without any forward-looking guarantees or investment advice intended.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments