Theravance Biopharma’s Recovery from Clinical Setbacks and Financial Turnaround in 2025

Theravance Biopharma transitions from losses to profitability post late-stage trial failures, leveraging YUPELRI sales and operational adjustments.

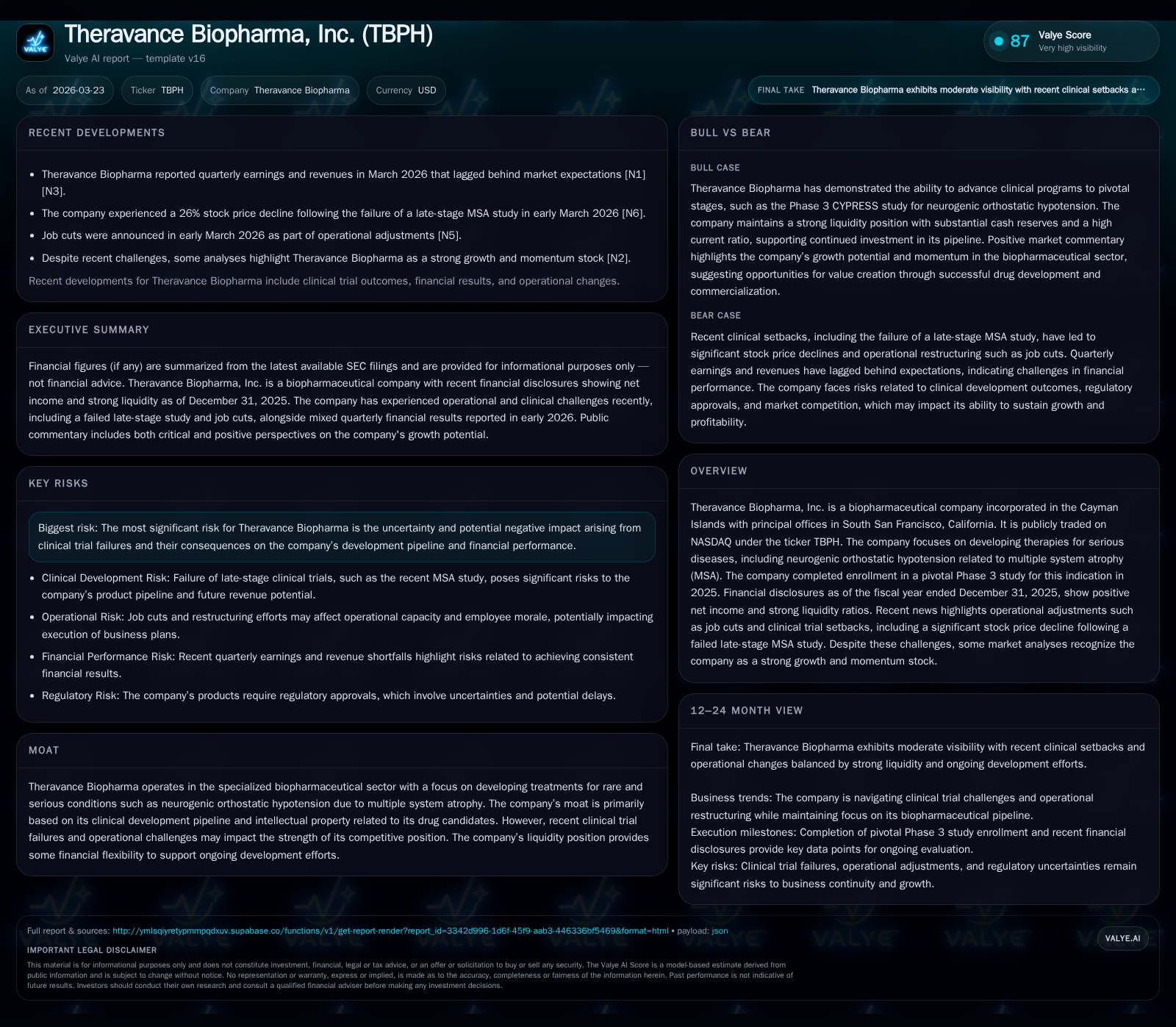

Theravance Biopharma (TBPH) experienced significant financial improvement in 2025 following years of operating losses linked to clinical development challenges. The company saw a strong rebound with $20 million operating income and $61 million net income, driven largely by steady growth in YUPELRI revenue despite competition and pricing pressures. However, setbacks such as the failure of a pivotal Phase 3 multiple system atrophy (MSA) study have prompted workforce reductions and underscore ongoing pipeline uncertainties. With ample liquidity and strategic cost management, Theravance aims to stabilize its performance while navigating patent litigation risks and competitive dynamics.

Overview

Theravance Biopharma, Inc., Cayman Islands-incorporated with US operations headquartered in South San Francisco, is focused on developing treatments for serious diseases including neurogenic orthostatic hypotension (nOH) related to multiple system atrophy (MSA). The company’s core commercial asset is YUPELRI, marketed through a collaboration with Viatris. After several years of operating losses tied to heavy R&D spend and pipeline volatility, Theravance achieved profitability in fiscal 2025 despite recent clinical trial setbacks ([S1], [N8]).

Historical Performance: Growth Drivers and Milestones

Theravance’s fiscal performance revealed a notable turnaround in 2025 compared to previous years marked by losses. Revenue recognition is primarily tied to royalties from YUPELRI sales by Viatris; implied revenue attributable to Theravance grew approximately 12% year-over-year to $93.3 million in 2025 ([S1]). This increment supports the company’s operational profitability which improved dramatically from an operating loss of $9.2 million in 2024 to an operating income of $20.0 million in 2025 ([F1]). Net income reversed accordingly, moving from a loss of $15.5 million in 2024 to a gain of $61.0 million in 2025 ([F1]).

The table below summarizes key financial metrics:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 61 | 239 | 20 | +493.0% |

| 2024 | -16 | -12 | -9 | -82.5% |

| 2023 | -9 | -27 | -6 | +17.9% |

| 2022 | -10 | -187 | -17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 20.6 |

| 2024 | 0 | -8.8 |

| 2023 | 197 | -4.0 |

| 2022 | 129 | -2.3 |

Source: SEC companyfacts cache [F1].

*Implied revenue; reported top-line includes other items as per SEC filings.[F1], [S1]

The significant jump in operating cash flow—from negative $11.54 million in 2024 to positive $238.54 million in 2025—also underscores improved operational efficiency and cash generation capacity ([F1]). Capital expenditures remain modest, consistent with typical asset-light biotech companies focused on drug development rather than manufacturing ([F1]).

Despite strong top-line momentum from YUPELRI royalties, the company faces commercialization risks given that YUPELRI competes against multiple short-acting bronchodilators with different dosing profiles ([S1]). Additionally, efforts by generic drug makers to challenge YUPELRI's patents have led Theravance into patent infringement litigation across several jurisdictions, increasing legal expenses and uncertainty over future revenue streams ([S1]).

Recent Clinical and Operational Challenges

Significant news emerged in early March 2026 that the company's pivotal Phase 3 CYPRESS study investigating treatments for symptomatic neurogenic orthostatic hypotension due to MSA did not meet primary endpoints, leading to a sharp stock price decline of approximately 26% on March 4 ([N8]). This setback has triggered operational adjustments including layoffs announced shortly thereafter ([N6]), highlighting the fragile nature of clinical-stage biotech fortunes.

This clinical failure impacts the prospect of expanding Theravance’s pipeline beyond its current approved products, placing pressure on existing revenue streams and necessitating prudent capital allocation going forward.

Future Growth Prospects

While recent pipeline disappointments create headwinds, Theravance Biopharma’s growth potential rests largely on several axes:

Continued ramp-up and expanded adoption of YUPELRI for COPD maintenance therapy through collaboration with Viatris remains the principal near-term growth engine ([S1]). While faced with pricing pressure due to channel mix evolution and generic threats, management anticipates more stable pricing dynamics and moderate demand growth beyond fiscal year 2026.

The company is conducting strategic reviews which may yield business development or alliance opportunities enhancing long-term pipeline prospects ([S1]).

Ongoing intellectual property enforcement against generic rivals aims to preserve exclusivity for YUPELRI's sales royalties for several more years ([S1]).

Advanced clinical assets aside from the failed MSA program may offer additional upside should further trials prove successful; these remain speculative without explicit milestone guidance provided ([N#]/[S#]).

In all cases, cautious capital stewardship will be needed given the clinical uncertainty inherent in specialty biopharma research.

Forecasts and Milestones: What To Watch

Though no explicit forward-looking guidance was disclosed beyond early-2026 filings ([S3]), external commentary points toward close monitoring of:

- Financial results for Q1–Q2 calendar year 2026 following the MSA trial failure impact.

- Outcomes from strategic review processes including any announced partnerships or licensing agreements.

- Resolution or progress in patent litigation defending YUPELRI’s market position.

- Updates on remaining pipeline candidates advancing through clinical stages.

- Trends in sales dynamics under Viatris collaboration reflecting market acceptance shifts.

Given prior volatility from both regulatory outcomes and clinical data releases, investors should watch official filings closely for material updates impacting organic growth outlooks.

Returns and Capital Allocation Strategy

Theravance displayed an impressive toggle from losses towards sustained profitability reflected by a calculated return on equity around 20.6% for fiscal year ended December 31, 2025 (based on net income over equity reported as $296.7 million) ([F1]).

Operating cash flows reached a robust $238.5 million while capital expenditures stayed relatively low—characteristic of R&D-heavy firms without major manufacturing footprint —resulting in an estimated free cash flow exceeding $236 million ([F1]).

Regarding capital deployment:

- Share repurchases were limited at approximately $0.45 million as part of a conservative allocation approach amid uncertain growth pathways ([F1], [S5]–[S8]).

- No dividends were declared nor indicated given reinvestment priorities into pipeline development.

- The company maintains excellent liquidity ratios (current ratio ~10.9), supported by cash holdings near $168 million that provide resilience against operational shocks ([F1]).

The measured buyback activity alongside strong cash reserves signals disciplined management focus on sustaining financial health while preserving optionality for future investments or transactional opportunities.

Market Position and Competitive Risks

Theravance operates within niche but intensely competitive biopharma sectors targeting rare conditions like neurogenic orthostatic hypotension due to MSA alongside maintenance therapies for COPD via YUPELRI ([S1], valye overview). Its moat largely depends on the proprietary clinical assets it advances plus protections afforded by patents—both currently challenged aggressively by generic entrants asserting Paragraph IV ANDA certifications ([S1]).

Increasing regulatory scrutiny around pricing policies and payor reimbursement trends also weighs on commercial outlooks especially amid continuing US healthcare cost containment efforts ([S1]) . The risk of losing exclusivity coupled with ongoing trial failures complicates the company's medium-term forecast.

Nevertheless, some analysts highlight Theravance as a 'strong growth stock' based on momentum from recent operational improvements counterbalancing headline setbacks ([N4], [N7]). Much depends on execution agility addressing challenges while progressing promising assets through required regulatory milestones.

Summary

Theravance Biopharma marked a critical inflection point in fiscal year 2025 by transitioning back into profitability after multi-year deficits driven by challenging development milestones and commercialization hurdles. Revenue growth chiefly powered by royalty streams from partnered sales of YUPELRI underpins this turnaround but faces patent litigation headwinds alongside intensified competition.

Clinical setbacks involving their late-stage MSA study introduced renewed uncertainty about the broader pipeline viability prompting workforce rationalization measures early in 2026 alongside vigilant cost control efforts.

Nonetheless, robust liquidity reserves backed by solid operational cash generation leave Theravance poised with flexibility to pursue strategic options aiming to restore developmental momentum and further capitalize on established commercial assets.

For stakeholders tracking this specialized biopharmaceutical company, key focus areas moving forward include patent dispute outcomes, success or failure signals from remaining clinical candidates, evolving market acceptance/pricing trends related to COPD therapies, and resultant impacts on investor confidence reflected through forthcoming quarterly disclosures.

This analysis is based solely on information contained within specified SEC filings [F1], official press releases [S#], earnings reports, and publicly available news sources [N#]. It is intended strictly as an informational review without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments