Yunhong Green CTI Ltd. Faces Intensifying Losses Amid Modest Growth and Liquidity Pressures

The company’s core foil balloon and flexible film products see slow revenue gains overshadowed by widening losses, customer concentration, and tight liquidity.

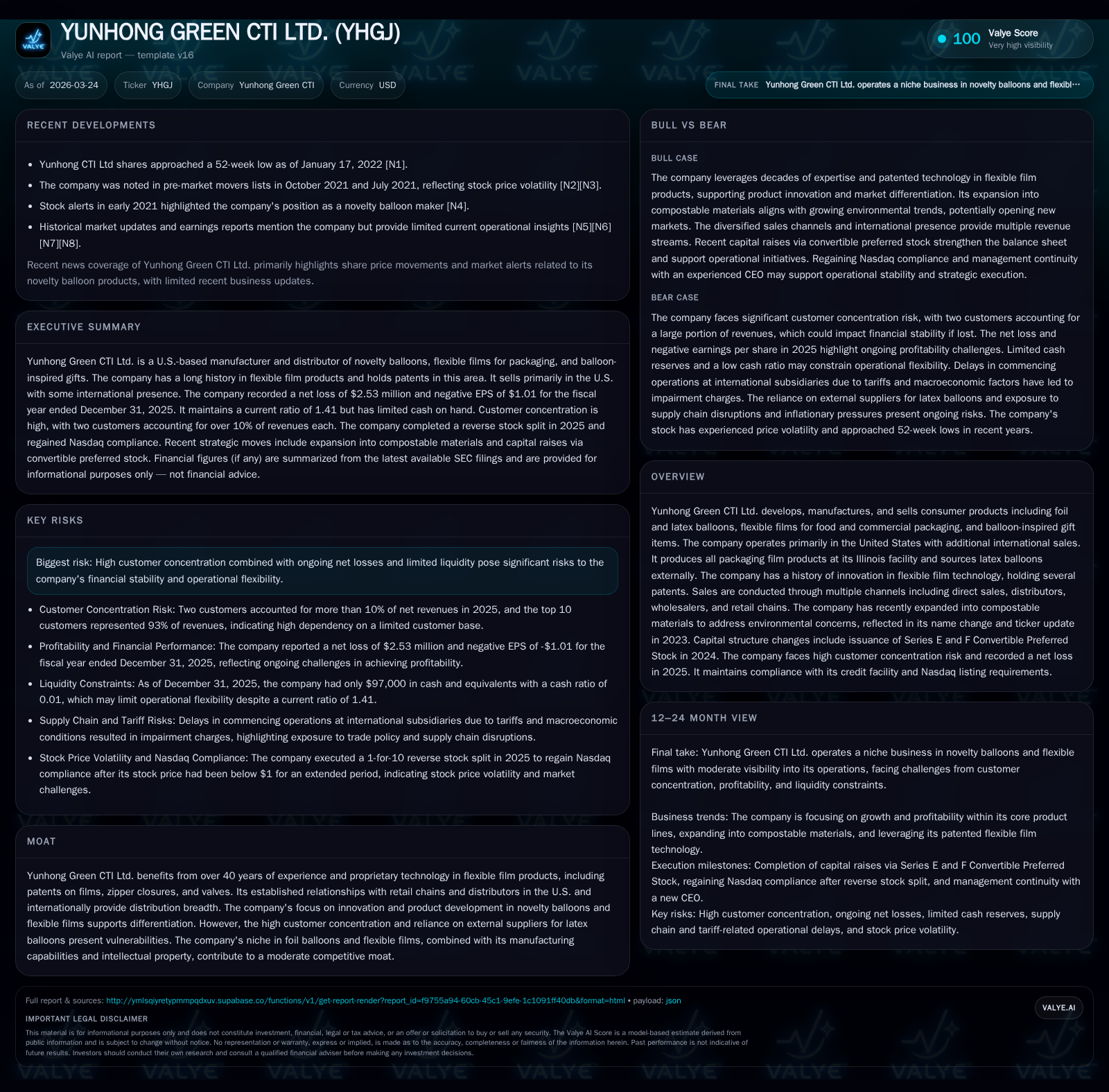

Yunhong Green CTI Ltd., a manufacturer of foil and latex balloons alongside flexible film packaging products, operates primarily in the U.S. with some international exposure. Total revenues increased modestly to approximately $19.7 million in 2025, led by foil balloons which represent the largest sales segment. Despite this growth, operating losses deepened significantly to $2.05 million in 2025 from $612,000 in 2024, while net losses widened to $2.53 million. Liquidity remains constrained with cash and equivalents at just $97,000 at year-end 2025 against current liabilities exceeding $10.6 million, yielding a current ratio of about 1.41. The company relies heavily on two major customers who accounted for roughly 93% of revenues in both 2024 and 2025, posing notable concentration risk. Capital structure changes include the issuance of Series E and F Convertible Preferred Stock in 2024 raising approximately $2 million combined; however, profitability challenges persist. A reverse stock split was executed in late 2025 to maintain Nasdaq listing compliance. Near-term growth depends on expanding distribution channels, introducing new product innovations including compostable materials, and stabilizing supply chain dynamics amid inflationary pressures.

Company Overview

Yunhong Green CTI Ltd., rebranded from CTI Industries in 2023 to highlight its focus on sustainable materials, develops and manufactures novelty consumer products including foil balloons and latex balloons (the latter sourced externally) alongside printed and laminated flexible films primarily used for packaging applications [S1][S23]. The company operates principally from its Lake Barrington, Illinois facility where all film production occurs [S1][S7]. Its balloon products are distributed through multiple channels including retail chains, wholesalers, independent sales representatives, and direct foreign sales managed from the U.S. market [S7][S9]. The firm also assembles balloon-inspired gift items such as candy bouquets [S21].

The company holds various patents protecting its proprietary technologies related to film closures and valves developed over four decades [S23]. While it leverages affiliated entities within the Yunhong China Group for sourcing support, plans for manufacturing expansion in China have been delayed due to tariff and macroeconomic conditions [S24].

Historical Financial Performance

Yunhong experienced moderate revenue growth but persistent widening losses through fiscal year-end 2025. Total net revenues rose approximately 9.8% from around $17.95 million in FY24 to about $19.7 million in FY25 [F1]. This increase was primarily driven by foil balloon sales which constitute the majority segment (65%), with additional contributions from film product lines (6%) and other products including balloon-inspired gifts (29%) [S22][F1].

Operating income deteriorated substantially from a loss of $612,000 in FY24 to a loss of approximately $2.05 million in FY25—a more than threefold increase—while net income declined from a loss of about $1.5 million to a loss of $2.53 million over the same period [F1]. Operating cash flow remained negative at -$172,000 but showed improvement compared with prior years’ larger deficits [F1]. Capital expenditures increased moderately to approximately $331,000 largely due to investments related to newly acquired equipment for planned operations in China that remain unrealized [F1][S24].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | 0 | -2 | -68.8% | |

| 2024 | -1 | -1 | -1 | 331000 | -537.9% |

| 2023 | 0 | -1 | 0 | 221000 | +84.0% |

| 2022 | -1 | 2 | -1 | 163000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -29.6 | |

| 2024 | -2 | -14.0 |

| 2023 | -1 | -6.3 |

| 2022 | 2 | -53.4 |

Source: SEC companyfacts cache [F1].

Customer Concentration & Market Risks

The company's revenue is highly concentrated with two customers accounting for approximately 93% of total revenues during both FY24 and FY25; one customer alone represented about 41% of revenues [S4][S9]. This concentration exposes Yunhong to significant risk if either major customer reduces purchases or shifts suppliers.

Latex balloons are sourced externally following the sale of the Mexican subsidiary that formerly manufactured these products [S23]. The company’s largest product line—helium-filled foil balloons—is sensitive to helium price volatility which directly impacts demand as customers may reduce orders when helium costs rise sharply [S10][S25]. Competitive pressures are intense across both novelty balloon and flexible film markets given numerous global competitors competing on price and innovation [S15][S25]. Although intellectual property protections exist for certain designs and technologies, enforcement remains uncertain.

Capital Structure & Liquidity

In early-to-mid 2024, Yunhong issued Series E and Series F Convertible Preferred Stock raising gross proceeds totaling approximately $2 million ($1.3 million Series E; $0.7 million Series F) along with warrants exercisable through March 2027 [S13][S28]. Some proceeds were initially recorded as liabilities prior to share issuance then reclassified as equity.

Despite capital raises, shareholders' equity declined from roughly $10.7 million at end-2024 to about $8.56 million at end-2025 primarily due to accumulated losses reducing retained earnings [F1]. Cash and equivalents fell sharply to just $97,000 against current liabilities exceeding $10.6 million resulting in a current ratio near ~1.41 indicative of tight liquidity but not immediate distress [F1]. Free cash flow remained negative at approximately -$503,000 (operating cash flow minus capex), underscoring ongoing cash burn risks absent profitability improvements [F1].

No dividends were paid during recent years consistent with loan covenant restrictions prohibiting distributions while losses persist [S13][F1]. The company implemented a reverse stock split (1-for-10) effective October 1, 2025 aimed at maintaining Nasdaq listing compliance after trading below minimum bid price requirements; compliance was restored by mid-October [S19].

Operational Challenges & Impairments

During FY25 Yunhong recorded an impairment charge of approximately $351,000 related to delays commencing operations linked to machinery acquired for its China subsidiary expansion efforts amid tariff disputes and macroeconomic uncertainty [F1][S24]. Depreciation expense related to these assets was approximately $500,000 during the year even though operations have yet to begin fully utilizing them.

Returns & Capital Allocation Summary

With net losses totaling around -$2.53 million against shareholders’ equity near $8.56 million at year-end FY25, the approximate return on equity stands near negative -29.6%, reflecting persistent unprofitability despite modest revenue gains [F1]. Capital allocation has prioritized sustaining operational capacity rather than shareholder returns; no share repurchases or dividends occurred recently due to credit facility restrictions tied to financial covenants [F1][S13][S14].

Outlook & Considerations

Growth initiatives focus on expanding distribution channels domestically and internationally while developing new product lines emphasizing compostable materials aligned with environmental trends following the company's rebranding in 2023 [S23][N/A]. Stabilizing supply chains amid inflationary pressures remains critical given cost increases only partially passed through without materially dampening volume demand yet [S10]. Reducing customer concentration risk is also an important strategic priority.

Investors should monitor progress on launching manufacturing operations at overseas subsidiaries, helium price trends impacting demand elasticity within their core balloon segment, liquidity management efforts including refinancing needs given limited cash reserves, and execution on innovation pipelines targeting sustainable packaging solutions.

This analysis is based solely on publicly available company filings without investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments