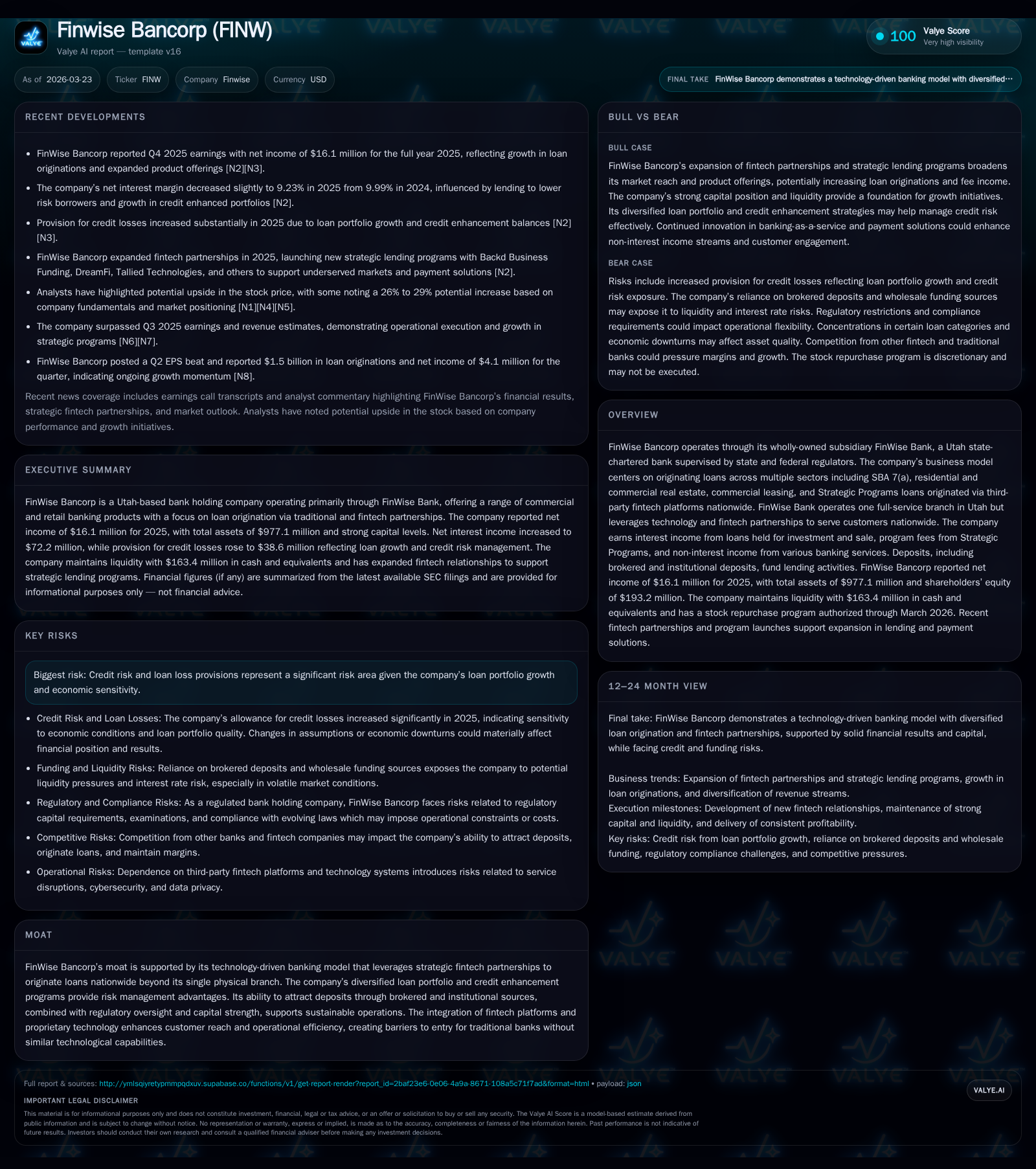

FinWise Bancorp’s Strategic Blend of Fintech Partnerships and Loan Diversification

FinWise Bancorp combines technology-driven nationwide lending with a diversified loan portfolio, fueling prudent growth and financial resilience.

FinWise Bancorp operates through FinWise Bank, leveraging a single Utah branch alongside fintech partnerships to originate loans nationally across SBA, real estate, commercial leasing, and Strategic Programs. While its net income rose 26.3% in 2025 supported by expanding Strategic Program loans, operating cash flow declined sharply due to changes in loan portfolio dynamics. The bank maintains robust capital adequacy with an equity ratio near 20%, funded predominantly via brokered and institutional deposits. Credit risk management remains pivotal amid portfolio growth and fintech reliance, with regulatory compliance and operational scalability critical to sustaining growth momentum.

Historical Financial Performance & Growth Drivers

FinWise Bancorp has demonstrated oscillating profitability trends over recent years with notable improvement in net income during FY2025. Net income for this period reached $16.1 million, a significant increase of approximately 26.3% compared to $12.7 million in FY2024 [F1]. This rebound followed declines observed in the two prior years (FY2023 down ~30.6%, FY2024 down ~27%), reflecting a renewed contribution from growing Strategic Program loans and effective portfolio diversification.

However, alongside this income rise, the bank experienced markedly deteriorated operating cash flows (CFO). CFO swung from positive values of $12.3 million in FY2023 to negative outflows reaching -$28.4 million by FY2025, a near 90% decrease year-over-year [F1]. This divergence between accrual earnings and cash generation warrants close scrutiny as it may signal timing effects related to loan sales or working capital changes.

Capital expenditures contracted sharply by over 95% in FY2025 relative to prior years ($0.22 million vs multi-million-dollar spends previously), indicating restrained investment possibly linked to stabilization of technology platform outlays or strategic cost discipline measures [F1]. Meanwhile, shareholders’ equity increased steadily over the four-year horizon (+11.2% YoY from $173.7M to $193.2M in FY2025), driven largely by retained earnings supporting balance sheet expansion and regulatory capital buffers.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 16 | -28 | 0 | +26.3% |

| 2024 | 13 | -15 | 5 | -27.0% |

| 2023 | 17 | 12 | 7 | -30.5% |

| 2022 | 25 | 61 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -29 | 8.3 |

| 2024 | 0 | -20 | 7.3 |

| 2023 | 5 | 5 | 11.3 |

| 2022 | 1 | 54 | 17.9 |

Source: SEC companyfacts cache [F1].

This table encapsulates FinWise's mixed yet progressively strengthening financial performance profile over the past four years.

Diversified Loan Origination and Strategic Programs Overview

At the core of FinWise Bancorp's business is a diversified loan book balanced across several key segments: Small Business Administration (SBA) Section 7(a) loans, residential and owner-occupied commercial real estate lending, commercial leasing loans, and Strategic Programs initiated through fintech partnerships [S1][S24].

The SBA portfolio constitutes a meaningful share — approximately $205 million as of year-end 2025 — down from about $255 million the prior year but representing roughly a third of total held-for-investment loans at about 35%. These SBA loans are underpinned by guaranties from the U.S federal government with primary repayment based on borrower cash flow metrics rather than collateral valuation alone [S24]. This segment benefits deeply from a referral arrangement with Business Funding Group (BFG), a Connecticut-based fintech that actively markets SBA loans nationwide while FinWise leverages its charter to originate and service them broadly despite having physical operations concentrated around Salt Lake City.

Strategic Programs represent an innovative dimension for FinWise whereby unsecured consumer and secured/unsecured business installment loans are originated via third-party fintech platforms employing proprietary origination systems and data analytics technology developed or integrated within FinWise Bank itself [S13][S14]. These programs have driven strong loan originations growth ($6.1 billion total originations reported for FY2025 across all segments), illustrating the agility and scale opportunity of technology-enhanced lending versus traditional brick-and-mortar constraints.

Residential and commercial real estate lending remains localized primarily within Utah's Salt Lake City metropolitan area but provides foundational stability given these are secured lending assets serviced directly through the branch [S24]. Commercial leasing further diversifies exposure albeit representing a smaller portion.

Technology-Enabled Nationwide Reach Beyond Physical Branches

FinWise's hallmark competitive advantage lies in its hybrid model — operating one full-service banking branch physically located in Utah coupled with extensive digital origination channels built on proprietary platforms integrated with multiple third-party fintech firms nation-wide [S13].

Nationwide geographic reach achieved through these fintech partnerships allows FinWise to underwrite and fund SBA loans, Strategic Program loans, and equipment financing remotely at scale without incremental fixed costs typical of expanding physical branch networks.

Their proprietary technology infrastructure enables efficient credit decisioning workflows supplementing traditional underwriting while automating onboarding processes for participating fintech originators — thus reducing cost-to-serve per loan significantly relative to legacy banks lacking digital frameworks.

This model supports operational leverage benefits especially if continued adoption or expanded program launches yield higher volumes without commensurate increases in staff headcount or physical footprint costs [S4]. Moreover, deposit gathering efforts complement nationwide lending via online/mobile banking solutions alongside rate-competitive products attracting both retail consumers and institutional depositors beyond Utah's borders.

Capital Structure, Liquidity Management, and Funding Sources

FinWise Bancorp maintains solid capital adequacy ratios compliant with regulatory mandates administered mainly by Utah Department of Financial Institutions (UDFI), FDIC oversight for insured deposits, and Federal Reserve regulations applicable to its holding company structure [S4][S6]. At December 31, 2025:

- Total shareholders’ equity was $193.2 million, up $19.5 million or +11% year-over-year primarily attributable to earnings retention rather than capital raises or dividends paid [F1][S6];

- Equity-to-assets ratio stood at approximately 19.8%, slightly below prior-year’s elevated level of ~23%, reflecting accelerated asset growth mainly via loan expansions tied to Strategic Programs [F1][S6];

- Return on average equity rose moderately to ~8.9%, evidencing steady profit generation relative to invested capital base [F1][S6];

- Liquid assets encompassing cash plus due-from bank balances totaled $163 million (~16.7% of total assets), providing ample buffer for short-term funding needs amid market uncertainties [F1][S4];

- The Bank holds access to sizable secured borrowing capacity at the Federal Reserve Discount Window totaling nearly $194 million collateralized by pledged loans/securities — none drawn as of latest reporting period — reflecting contingency funding availability if needed without reliance on wholesale debt issuance currently [S4][S6];

- Additional unsecured short-term lines with correspondent banks totaling approximately $16 million further underscore liquidity flexibility though were inactive at period end suggesting sufficient internal resources [S5];

- Deposits constitute the predominant funding source accounting for over three quarters (~77%) of total liabilities; growth during FY2025 came primarily from brokered time deposits increasing nearly $153 million reflecting strategic funding augmented by institutionally sourced depositors attracted via competitive rates offered relative to asset yields on loans held-for-investment [S16][S26].

This layered funding approach blends core deposit gathering efforts supplemented by brokered/non-core deposits enabling favorable asset-liability management matching term structures where feasible while balancing funding costs against net interest margins.

Returns, Capital Allocation Policies, and Shareholder Distributions

While FinWise has grown earnings moderately increasing net income by over one-quarter in FY2025 amid rising loan portfolio complexity, it maintains disciplined capital allocation reflective of regulatory prudence typical within regional-scale federally supervised institutions:

- Return on average equity was reported at approximately 8.9%, up from ~7.7% prior year — reasonable for a lender undergoing strategic expansion into higher risk-adjusted yield fintech-driven portfolios without sacrificing credit standards outright [F1][S6];

- There have been no dividend payments since inception — consistent with stated intent focusing on capital retention required for sustained organic growth under regulatory frameworks governing banks' dividend distributions tied to supervisory approval reflecting well-capitalized status maintenance priorities [S8][S12];

- An authorized stock repurchase program exists permitting open market repurchases up to roughly 641K shares since March 6, 2024; however actual buybacks ceased during the second half of FY2025 after limited activity totaling approximately $0.5 million spent previously — indicating conservative deployment possibly awaiting market conditions or internal liquidity thresholds allowing flexibility without committing capital prematurely amidst rising credit risks or macroeconomic uncertainty [F1][S8];

- Management continues emphasizing payout restraint favoring reinvestment into technology infrastructure enhancements alongside scaling partnerships that underpin future organic revenue streams rather than returning cash via distributions presently.

Risk Profile: Credit Risk, Regulatory Environment, and Operational Considerations

Key risks affecting FinWise primarily emanate from its expanded exposure across diverse but credit-sensitive sectors combined with operational dependencies inherent in its tech-enabled origination model:

- Credit risk concentration exists notably within construction-related loans and small-to-medium business exposures including SBA portfolios where regional economic downturns could pressure borrower repayments; ongoing enhancements to underwriting policies mitigate but do not eliminate this vulnerability given economic cyclicality implications inherent in banking portfolios [S1][S24];

- The allowance for credit losses (ACL) rose materially from $13 million at end-FY24 to nearly $37 million at end-FY25 propelled by both absolute loan growth and increased credit enhanced balances embedded within Strategic Programs requiring nuanced loss provisioning practices factoring in counterparty indemnifications against incurred losses—reflecting proactive conservative accounting aligned with CECL standards though sensitive to macroeconomic scenario shifts such as unemployment stress tests conducted internally showing manageable moderate incremental provisioning needs under adverse assumptions [S9];

- Reliance on third-party fintech service providers for referral origination pipelines and program management introduces operational risk including data security/privacy challenges highlighted by recent class action litigation relating to alleged employee data breaches implicating reputational damages potential—a ubiquitous concern for digitally oriented lenders subject also to evolving regulations governed by CFPB privacy mandates alongside cybersecurity compliance burdens escalated by sophisticated threats landscape nationally [S19];

- Regulatory scrutiny intensifies especially around areas such as fair lending laws compliance including Community Reinvestment Act (CRA) considerations given FinWise’s national lending footprint juxtaposed against single-state physical presence—requiring careful adherence to nondiscriminatory practices as well as adaptable credit policies mindful of state usury laws impacting 'true lender' scrutiny particularly within marketplace-derived portfolios; continuous monitoring mandatory alongside investment in compliance infrastructure due to heightened examination risks under Dodd-Frank Act enforcement regimes managed partly via FDIC/UDFI/Federal Reserve supervision overlap typical for Utah-chartered banking groups [S19];

- Operational scalability risks loom related to rapid technological change including artificial intelligence adoption ambitions that may impose implementation complexities or governance challenges if improperly handled affecting underwriting accuracy or customer experience reliability necessitating sustained R&D investment balanced cautiously against cost control objectives while safeguarding intellectual property rights connected to proprietary credit analytics tools integral to competitive moat around tech-enabled operations.

Overall risk management strategies prioritize layered oversight integrating both quantitative portfolio monitoring metrics alongside qualitative governance emphasizing cross-functional coordination between credit risk management teams, legal/compliance functionaries, IT cybersecurity operations teams plus vendor oversight committees focusing on alignment with long-term financial resiliency goals.

Key Metrics & What to Watch Moving Forward

Absent explicit forward guidance beyond routine filings through early Q1 FY26 events disclosure does not specify upcoming milestone targets necessitating focus on qualitative indicators:

- The pace of loan portfolio expansion particularly within high-yielding fintech-originated Strategic Programs balanced against quality trends such as delinquency upticks or vintage loss emergence will be critical signals informing sustainability of recent income gains versus provisioning drag potential causing margin compression;

- Deposit base composition shifts particularly monitoring brokered vs core deposit ratio changes provide insights into asset-liability matching efficiency as well as liquidity risk dynamics given heavy reliance on institutional sources requiring competitiveness retention amid fluctuating rate environments simultaneously feeding into net interest margin variability considerations influencing overall profitability trajectory;

- Capital adequacy metrics retention above regulatory well-capitalized thresholds remains fundamental especially if new product launches or acquisitions accelerate growth requiring supplemental earnings retention or external capital raises impacting shareholder return policies;

- Progression leveraging existing platform investments towards operational leverage improvements indicated through stabilized or normalized capex spend levels coupled with improved operating cash flow conversion ratios would reflect maturation phase realized gains enhancing free cash flow outlook amid cyclical economic conditions uncertainties;

- Evolving regulatory developments including CFPB enforcement actions targeted towards fintech-enabled lenders implementing 'true lender' principles may impose structural adjustments potentially constraining permissible product offerings thereby influencing future revenue mix composition;

- Management execution effectiveness building deeper integration amongst multiple Strategic Program partners such as Backd Business Funding or DreamFi affecting customer penetration depth offering diversification benefits beyond current SBA/referral dominant channels remains a transformational element worth tracking qualitatively given its bearing on long-term competitive positioning.

Disclaimer: This analysis is based solely on information available up to March 23, 2026 from SEC filings and associated disclosures without extrapolation beyond confirmed data points; no investment advice or recommendations are provided.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments