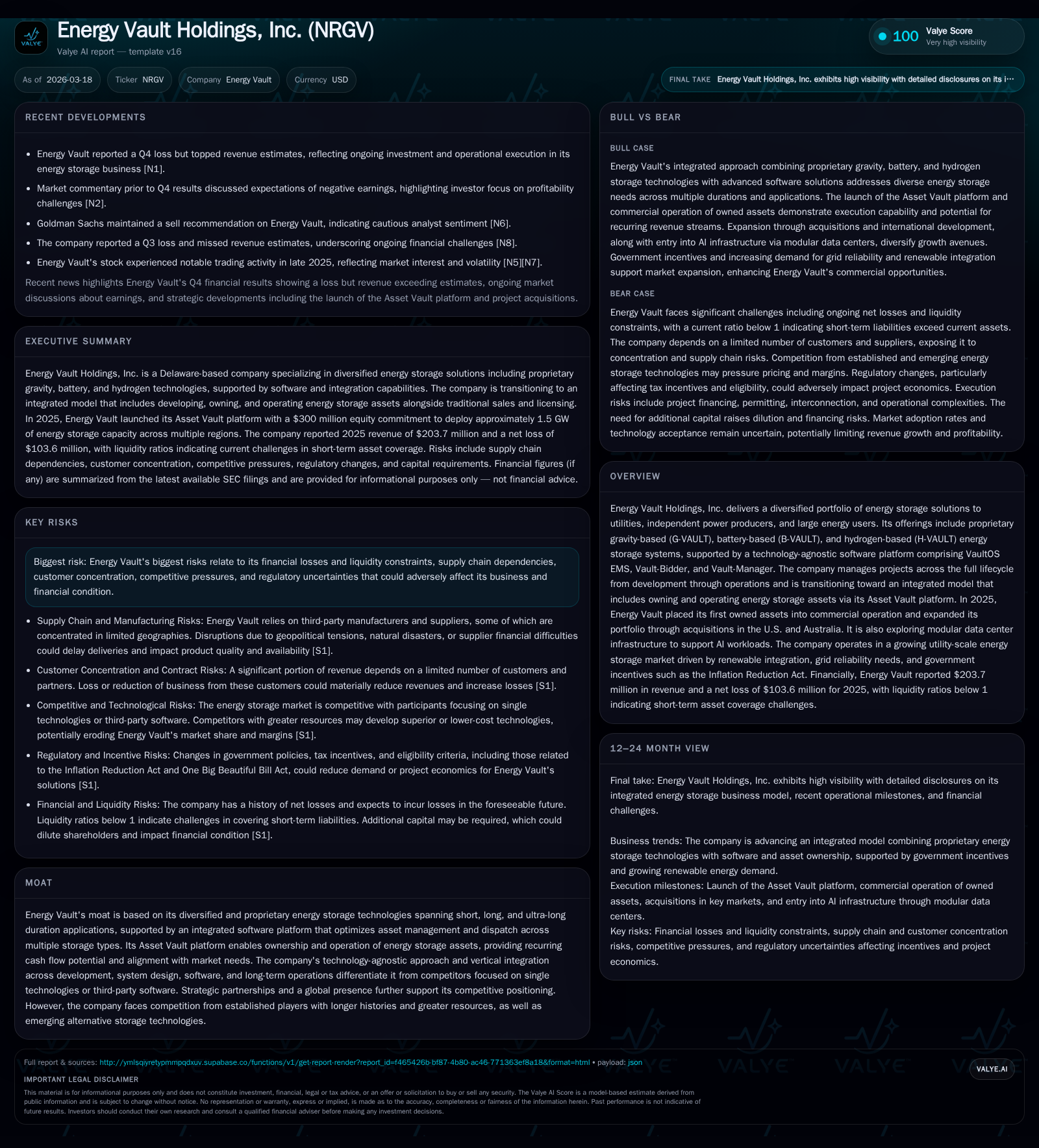

Energy Vault’s Transition to Own & Operate Model Constrains Profitability Amid Growing Storage Demand

Energy Vault’s diversified energy storage technologies underpin strong bookings but intense competition and capital intensity weigh on near-term earnings.

Energy Vault Holdings, Inc. operates a unique portfolio of gravity, battery, and hydrogen energy storage solutions supported by proprietary software and is shifting towards owning and operating assets to capture recurring revenues. In 2025, the company placed its first owned projects into commercial operation and reported revenue growth, yet sustained large operating losses amid heavy capital expenditures. Backlog and pipeline indicate robust demand across U.S., Australian, and European markets, but profitability remains elusive due to technology development costs, supply chain challenges, and competitive pressures from established battery vendors. The company’s low current ratio highlights ongoing liquidity risks during this capital-intensive expansion phase.

Company Overview

Energy Vault Holdings, Inc. is an emerging energy storage solutions provider focusing on utilities, independent power producers, and large energy users. Its portfolio spans proprietary gravity-based (G-VAULT), battery-based (B-VAULT), and green hydrogen (H-VAULT) storage technologies supported by integrated software platforms including VaultOS EMS. Traditionally centered on build-and-transfer models through EPC or equipment delivery contracts, since 2024 the company has progressively shifted to an integrated "Own & Operate" business model aimed at generating recurring revenues from owned assets via its Asset Vault platform backed by dedicated project-level capital [S1][S5][S7].

Historical Performance

Energy Vault's growth trajectory has been characterized by rising revenue accompanied by persistent operating losses reflective of ongoing product development expenses, supply chain investments, and capacity buildout costs. The fiscal year ended December 31, 2025 reported revenue of approximately $204 million [F1], up on prior years where revenue was lower (historical revenues not explicitly detailed). Operating income loss narrowed substantially to -$74 million from a loss exceeding -$130 million in FY2024—a roughly 43% improvement year-over-year—indicating operational leverage beginning to materialize as deployments scale. Net loss also shrank from about -$136 million in FY2024 to -$104 million in FY2025 [F1].

Operating cash flow exhibited similar improvement trends but stayed negative (-$5.6 million in FY2025 vs negative $56 million prior year). Capital expenditures declined ~30% year-over-year to nearly $41 million reflecting a measured investment pace after prior aggressive capex. Nonetheless free cash flow was still negative by more than $46 million indicating that operating inflows remain insufficient to cover investing activities fully [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -104 | -6 | -74 | 41 | +23.7% |

| 2024 | -136 | -56 | -130 | 59 | -37.9% |

| 2023 | -98 | -93 | -107 | 30 | -25.7% |

| 2022 | -78 | -23 | -63 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -47 | |

| 2024 | -115 | |

| 2023 | -123 | -44.0 |

| 2022 | -26 | -27.2 |

Source: SEC companyfacts cache [F1].

Liquidity indicators reveal pressure points: current assets stood at $121 million vs current liabilities of $165 million for a current ratio ~0.73 signaling potential short-term funding challenges despite solid cash reserves of ~$58 million [F1][S8].

Business Model and Product Portfolio

Energy Vault provides a technology-diverse suite of energy storage solutions:

- B-VAULT: Electrochemical battery energy storage systems focused on short-duration applications (1–4 hours), offered both AC/DC coupled; includes the second-generation FlexGrid variant targeting small commercial/industrial users (~2–25 MW).

- G-VAULT: Gravity-based mechanical storage using composite blocks or water for longer-duration applications emphasizing durability and infrastructure longevity.

- H-VAULT: Green hydrogen storage integrating fuel cells supporting hybrid microgrid architectures.

All product lines are integrated via the sophisticated VaultOS platform suite covering energy management (EMS), bidding optimization (Vault-Bidder), and operational oversight (Vault-Manager). The software focus enables enhanced asset dispatch across heterogeneous storage types optimizing grid participation revenues [S5][S21].

The company continues engaging in traditional third-party EPC contracts while expanding its own asset ownership operated through the Asset Vault platform launched in 2025 with notable capital commitments including a $300 million preferred equity tranche from Orion Infrastructure Capital targeting ~1.5 GW deployment capacity across key geographies including U.S., Australia, and Europe [S1][S4][S7].

Noteworthy deployments include the Cross Trails Battery Energy Storage System in Texas—commissioned mid-2025—which operates under a landmark physically settled revenue floor contract with Gridmatic marking a first for ERCOT region BESS offerings; also the Calistoga Resiliency Center hybrid microgrid blends H2 fuel cells and lithium-ion batteries enhancing grid reliability for isolated communities or heavy industrial zones [S1][S21].

Market Positioning and Competitive Landscape

Energy Vault’s core competitive advantage lies in its multi-technology approach addressing diverse duration needs beyond standard lithium-ion-only battery players—combining gravity storage’s long-duration capabilities with flexible battery systems plus emerging green hydrogen options provides differentiation alongside vertically integrated lifecycle services from development through operations backed by proprietary control software [S16][S21].

However, Energy Vault faces significant competition against well-capitalized incumbents such as Tesla, Fluence Energy, LG Chem, Samsung SDI, CATL for BESS solutions; further layered competition arises from emerging long-duration storage innovators like ESS Inc., Eos Energy Enterprises as well as alternative tech categories such as thermal or carbon capture storage which could evolve rapidly challenging current market boundaries [S16][S17]. Software competition is also fierce with competitors developing their own EMS to capture value from increasing grid market complexities.

Furthermore, reliance on third-party cell manufacturers combined with tariff changes—including U.S.’s January 2026 tariff hike on lithium-ion batteries—introduces cost pressures that must be managed carefully through diversified supplier arrangements such as recent agreements capturing sodium-ion tech capacity from Peak Energy [S6][S22]. These supplier dynamics directly impact delivery timelines affecting backlog conversion rates.

Growth Prospects and Demand Pipeline

As of December 31, 2025 Energy Vault reported backlog of approximately $1.3 billion representing contracted but unrecognized revenue as well as contingent options expected to be exercised pending project execution milestones; net bookings for the year were roughly $1.1 billion indicating strong order intake momentum even while developed pipeline—the aggregate potential revenue identified via awarded/shortlisted projects or advanced talks—stood at around $2.4 billion serving as an expanded opportunity set for future conversion [S4][S11].

The robust pipeline is driven by accelerating electrification demand exacerbated by rapid adoption of renewables requiring flexible grid balancing solutions along with rising data center loads especially connected to AI computing workloads which Energy Vault intends to address through modular powered shell data centers leveraging their energy assets for onsite resiliency [S19][S27].

The intrinsic modularity across gravity-based infrastructure deployments and advanced BESS product lines positions Energy Vault well to tailor solutions across diverse customer segments including utilities needing ancillary services, IPPs seeking capacity firming options, commercial/industrial clients pursuing resiliency upgrades, and new hyperscale compute facilities demanding low-latency power security.

Financial Outlook and Milestones to Monitor

While explicit guidance is not provided post-filing beyond backlog figures and known milestones such as Cross Trails COD completion date in May 2025 or expansions into Australia/Europe service centers in Switzerland established in late 2025, critical indicators include:

- Conversion rate of backlog bookings into recognized revenue over subsequent quarters;

- Operating margin trajectory amidst scaling asset ownership versus third-party EPC revenue mix;

- Ability to sustain EBITDA improvements while managing capex intensity related to Own & Operate buildouts;

- Evolution of recurring revenues derived from long-term service agreements combined with software licensing upsells;

- Responses to regulatory changes impacting tariff costs or incentive programs such as IRA credits influencing project economics.

Returns Profile and Capital Allocation Strategy

ROE remains negative at an approximate -46% level due primarily to sustained net losses relative to equity base highlighting absence of profitability stemming largely from early-stage commercialization investment phase [F1]. Operating cash flows have improved markedly but continue negative implying ongoing external financing dependency.

Capital allocation focuses heavily on growth investment including capex related to owned asset commissioning while maintaining liquidity buffers supported by preferred equity injections such as Orion Infrastructure Capital commitment described above [F1][S8]. Dividends or buybacks are not material considerations given reinvestment needs.

Managing working capital requirements prudently remains critical considering current ratio below unity signaling tight short-term financial flexibility requiring close monitoring especially if macroeconomic headwinds affect financing availability or customer creditworthiness [F1][S14]. Given the capital-intensive nature of deploying energy infrastructure aligned with utility-scale renewable integration timelines, Energy Vault’s strategic pivot toward Own & Operate positions it for potentially higher-margin recurring cash flows but places near-term stress on liquidity metrics until scale economies develop.

Risks Assessment Summary

Prominent risks revolve around:

- Continuous engineering refinement demands creating schedule adherence uncertainty affecting rollout cadence;

- Customer acquisition risks including dependence on limited major customers impacting revenue predictability;

- Supply chain exposure exacerbated by geopolitical trade tensions imposing tariffs particularly on lithium-ion cells impacting cost competitiveness;

- Legal/regulatory compliance challenges globally including anti-corruption laws increasing operational risk;

- Competition risk from entrenched players capable of rapid innovation threatening technology relevance;

- Economic sensitivity affecting project financing environment critical for both direct asset ownership and customer purchases;

- Unanticipated delays during permitting or interconnection may defer revenue recognition compressing near-term cash flows. These factors collectively pose considerable execution risk during this transformational phase toward owning operational assets while continuing system deliveries under traditional models [S9][S10][S12][S13].

Conclusion

Energy Vault Holdings stands at an inflection point transitioning beyond technology provider into operator-investor within burgeoning utility-scale energy storage markets responding to rising decarbonization imperatives worldwide. Its multi-pronged technological base combined with proprietary integrated software suite represents clear differentiation versus single-tech competitors enhancing addressable markets across varying duration needs. Yet financials reflect the growing pains typical of early-stage diversified infrastructure developers requiring ongoing capital infusion alongside demonstration of economically sustainable operating margins to win scale investor confidence. Success hinges on disciplined execution converting robust backlog into profitable operations supported by enhanced cash flow generation while navigating supply chain constraints plus intensifying competitive pressures within highly dynamic global energy markets. Investors should track key pipeline conversion metrics alongside liquidity movements while monitoring customer diversification progress plus regulatory developments shaping incentive frameworks vital for accelerating adoption rates.

This report is intended solely for informational purposes based on publicly available filings and news sources cited herein without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments