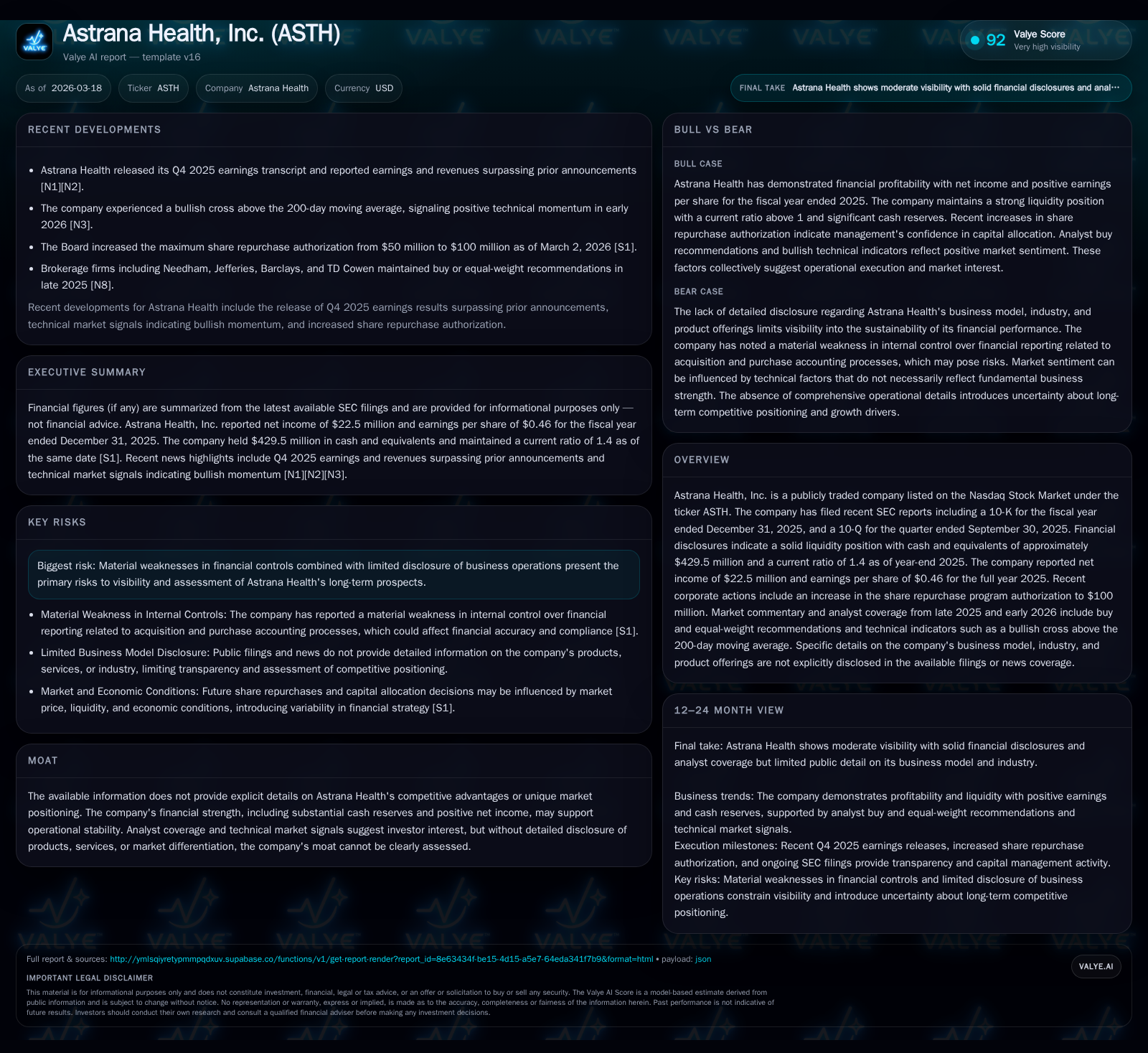

Astrana Health Leverages Strong Liquidity and Buyback Expansion Despite Control Weaknesses

Astrana Health reported solid revenue growth and expanded its share repurchase program while addressing internal control challenges.

Astrana Health, Inc. posted a remarkable rebound in revenue to over $519 million in 2025, driven largely by acquisition-related growth, despite operating income retreating modestly. The company maintains a strong liquidity position with $429.5 million in cash and an increased buyback authorization now set at $100 million. Material weaknesses in financial controls related to acquisition accounting pose ongoing risk. Investors should monitor upcoming filings for resolution progress and clarity on the business model as disclosures remain limited.

Historical Growth and Financial Performance

Astrana Health has undergone significant expansion since the mid-2010s, reflected in its revenue scaling from approximately $33 million in fiscal 2015 to a staggering near $520 million by the end of 2025 [F1]. This more than fifteenfold escalation is exceptional within healthcare services or technology sectors, hinting at aggressive M&A activity or rapid organic growth during the period.

However, the surge was accompanied by less consistent profitability dynamics. Operating income climbed steadily from low double digits into the tens of millions throughout early years but peaked around $89.3 million in fiscal 2024 before sliding approximately 12% to $78.5 million in fiscal 2025 [F1]. Net income exhibited greater volatility; positive results above $60 million were recorded in prior years but dropped nearly half to $22.5 million last year, likely reflecting integration costs or one-off items tied to growth initiatives [F1].

Operating cash flow efficiency improved notably with a near doubling in CFO from about $52 million in 2024 to nearly $115 million in 2025 [F1], suggesting underlying operational cash-generative improvements. Capital expenditures rose moderately by over 25% last year, potentially indicating investment into technology infrastructure or scaling of service capabilities [F1]. Free cash flow stands healthy at more than $104 million, providing headroom for capital returns or reinvestment.

The company's liquidity profile remains robust, featuring cash and equivalents of roughly $429.5 million alongside current assets totaling about $863 million against current liabilities near $615 million, rendering a current ratio at a comfortable 1.4 [F1]. This financial flexibility underpins Astrana Health's capacity to fund acquisitions or withstand market volatility.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 22 | 115 | 79 | 10 | -47.9% |

| 2024 | 43 | 52 | 89 | 8 | -28.9% |

| 2023 | 61 | 68 | 85 | 29 | +1728.7% |

| 2022 | -4 | 82 | 13 | 23 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 26 | 104 | 2.9 |

| 2024 | 1 | 44 | 6.1 |

| 2023 | 10 | 40 | 9.9 |

| 2022 | 9 | 59 | -0.7 |

Source: SEC companyfacts cache [F1].

Revenue for years prior to 2024 not fully available for YoY percent calculation.

Business Model and Industry Positioning

Despite robust financial metrics reported recently [S1][S8], Astrana Health provides sparse public detail regarding its exact business lines or industry segments beyond general health-related services [S8]. The company’s filings emphasize growth through acquisitions but omit comprehensive portfolios of product offerings or client bases that usually define competitive moats.

This lack of clarity restricts external ability to evaluate sustainable differentiation or pricing power relative to peers in healthcare technology or service delivery sectors — areas where consolidation often commands scale benefits but also demands integration expertise.

Risks and Internal Controls

A critical factor shadowing Astrana Health’s outlook involves disclosed material weaknesses in internal controls over financial reporting—particularly around acquisition and purchase accounting processes [S9][S20]. Such findings highlight challenges integrating complex deals which could impact the reliability of reported financials if unremedied.

The company plans to address these deficiencies during its filing extension period for the annual report [S9]. Investors and stakeholders must watch this remediation process carefully as persistent control lapses could trigger regulatory scrutiny or impair confidence.

Capital Allocation and Returns

Astrana’s approach reflects prioritization of capital returns alongside operational investments. The extension of the share repurchase program authorization from $50 million to $100 million signals management confidence in the stock’s intrinsic valuation and commitment to shareholder value creation [S9][N2]. Approximately $35.9 million remained available for buybacks at end-2025 post repurchasing over half a million shares during Q4 alone.

Dividend payments have been recorded historically but details post-2019 are unavailable; focus appears on buybacks given recent disclosures [F1]. Robust free cash flow generation exceeding $104 million after capex facilitates this dual capacity for opportunistic reacquisitions plus reinvestment into growth initiatives.

Return on equity calculated approximately at a modest near-3% level [F1] suggests earnings still reflect reinvestment phases rather than mature profitability optimization.

Future Outlook and What To Watch

Explicit forward guidance is absent across current official communications [N1][S1], shifting emphasis onto qualitative indicators:

- Resolution status of material weaknesses in internal controls will be central.

- Updates on acquisition pipeline execution and integration successes could further unlock economies of scale or margin improvements.

- Market responses post expansion of buyback authorization may reflect investor sentiment regarding valuation amid operational uncertainties.

- Transparency enhancements relating to core operations and competitive strategy would materially aid fundamental assessment.

Investors must await forthcoming SEC filings including the delayed Form 10-K for calendar year-end December 31st, 2025 expected soon following extended deadline granted [S9][S20]. Enhanced disclosure therein will hopefully offer clearer directional cues on sustained growth trajectory versus episodic gains via transaction activity.

Conclusion

Astrana Health stands out as a rapidly scaling entity bolstered by ample liquidity reserves and demonstrable free cash flow strength enabling significant capital returns through share repurchases. Yet simultaneous risks surrounding weak financial controls and limited operational transparency complicate a complete evaluation of strategic durability or moat quality.

Monitoring remediation efforts on internal controls alongside future filings will be critical milestones for market participants interested in this evolving healthcare services/technology platform going forward.

The information presented herein relies exclusively on publicly filed documents from Astrana Health and related news releases as cited; no projections beyond disclosed data have been made. This report does not constitute investment advice nor a recommendation regarding any security.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments