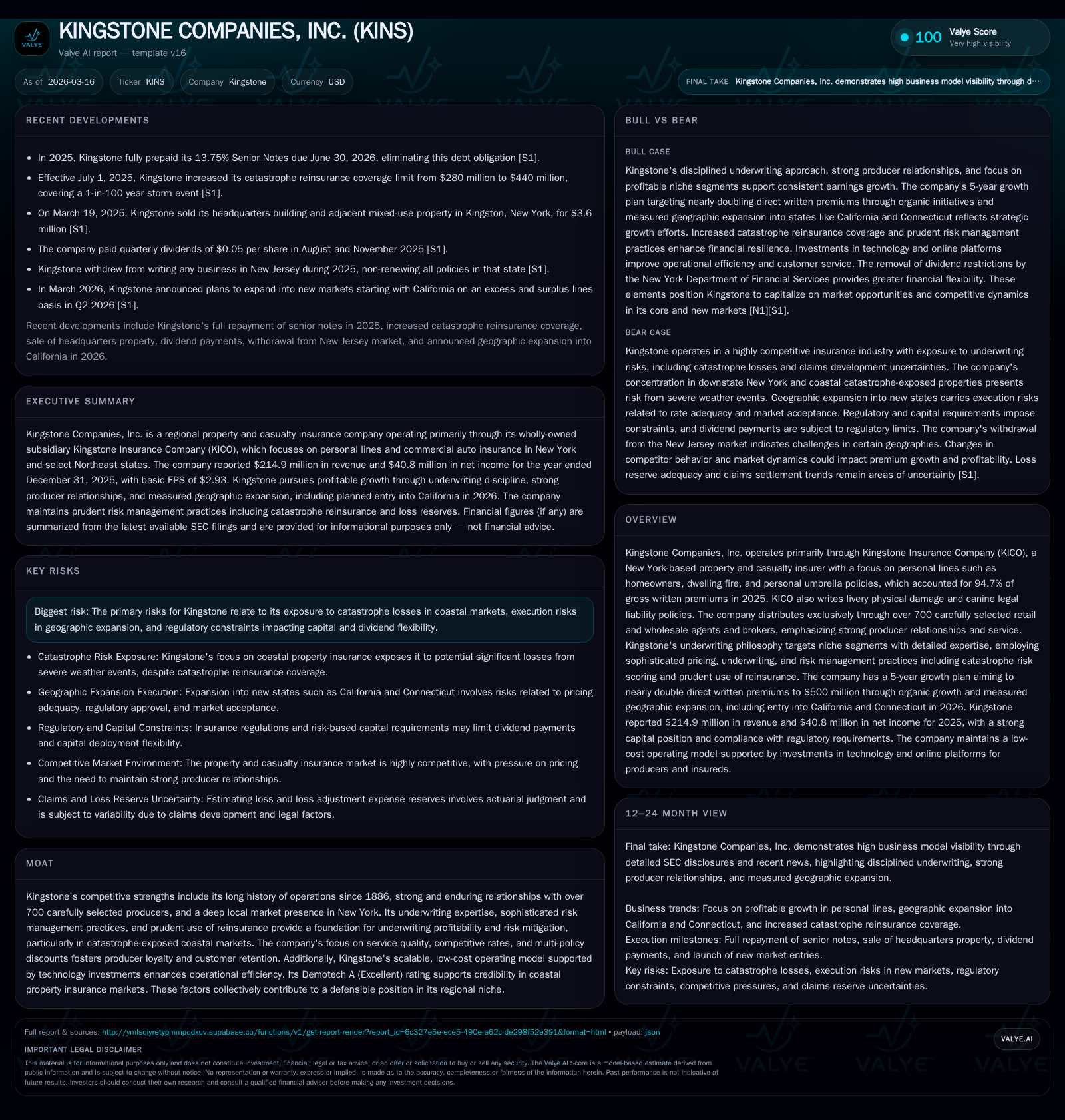

Kingstone Companies' Strategic Surge: From Regional Insurer to Growth Contender

Kingstone Companies leverages its deep New York market roots and producer partnerships to drive underwriting profitability and ambitious growth.

Kingstone Companies, operating through Kingstone Insurance Company (KICO), has transformed from multi-year underwriting losses into a double-digit profit generator by focusing on personal lines in catastrophe-exposed New York markets. Its 2025 financials show a significant rebound with 38.5% revenue growth and 122% net income increase, driven by premium growth supported by strong producer relationships and prudent risk management including expanded catastrophe reinsurance coverage. The company’s five-year plan targets nearly doubling direct written premiums to $500 million through measured geographic expansion and niche underwriting. While regulatory constraints and catastrophe exposure remain key risks, recent dividend flexibility improvements and capital efficiency (approximate 33% ROE) underpin a solid foundation for sustainable growth.

Historic Performance: From Underwriting Losses to Double-Digit Profit Growth

Kingstone Companies’ financial trajectory over the last four years clearly illustrates a successful turnaround. After reporting net losses of approximately -$22.5 million in FY2022 and -$6.2 million in FY2023, the company achieved net income of $18.4 million in FY2024 before more than doubling that figure to $40.8 million in FY2025 [F1]. Revenue grew markedly by 38.5% year-over-year to approximately $215 million in 2025, up from just over $130 million in 2022.

This recovery is reflected in cash flow metrics as well: operating cash flow improved from negative territory (-$0.9 million in FY2022) to a positive $57.9 million in FY2024 and further increased to nearly $76 million in FY2025 [F1]. Capital expenditures remained modest while the business enhanced its cash generation capabilities—indicative of improved underwriting profitability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 215 | 41 | 76 | 3 | +38.5% | +122.1% |

| 2024 | 155 | 18 | 58 | 2 | +7.6% | +397.6% |

| 2023 | 144 | -6 | -11 | 2 | +10.8% | +72.6% |

| 2022 | 130 | -23 | -1 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 73 | 33.2 | |

| 2024 | 56 | 27.5 | |

| 2023 | 0 | -13 | -17.9 |

| 2022 | 1277066 | -5 | -62.3 |

Source: SEC companyfacts cache [F1].

This table demonstrates accelerating revenue growth alongside dramatic profit restoration.

Core Market Focus: Personal Lines and Catastrophe Risk Management

Kingstone’s primary product focus is on personal lines—including homeowners, dwelling fire, cooperative/condominium, renters, and personal umbrella policies—which accounted for approximately 94.7% of gross written premiums as of December 31, 2025 [S6][S9]. These policies are predominantly concentrated (98%) within New York State’s coastal region—a market exposed to natural catastrophes such as hurricanes and severe storms.

The company employs detailed underwriting expertise supported by sophisticated catastrophe risk modeling tools that assess property exposures dynamically [S26]. This approach facilitates prudent risk selection balancing profitable growth against adverse selection risks.

In July 2025, Kingstone increased its catastrophe reinsurance coverage limit from $280 million to $440 million for single-event losses—aligned with a one-in-100 year storm event per industry models—to mitigate capital strain from severe weather while supporting rate stability [S1][S18]. Additionally, hurricane deductibles tailored by risk parameters help moderate loss severity during windstorm events [S26].

Producer Partnership Model: Sustaining Premium Growth Through Strong Distribution

Distribution is exclusively through over 700 carefully selected retail and wholesale agents ("producers") evaluated on multiple criteria including sales potential, loss history, market knowledge, and alignment with Kingstone's niche strategy [S6][S11]. Each producer is assigned a dedicated underwriter providing direct access for personalized risk assessment decisions [S11].

This model fosters loyalty; producers consistently rate Kingstone above average for underwriting quality, claims responsiveness, and service standards.

Features such as multi-policy discounts encourage bundling (e.g., homeowners with personal umbrella insurance), enhancing retention rates alongside periodic performance reviews ensuring portfolio quality management [S11]. Technology investments provide quoting tools, policy form access, periodic updates via "Producer Grams," and claims tracking portals enhancing service efficiency.

This producer-centric approach protects premium inflows against commoditized pricing pressures while enabling targeted penetration within select geographies.

Growth Blueprint: Targeting Nearly $500 Million Written Premiums Over Five Years

Kingstone announced a five-year strategic plan aiming to nearly double direct written premiums from roughly $278 million (FY2025) toward $500 million via organic initiatives complemented by selective acquisitions [N1][S9].

Key pillars include deepening penetration into New York’s Downstate markets—leveraging competitors’ exits from personal lines—and an agreement (AmGuard Renewal Rights) involving approximately $70 million annual premium [S1][S12].

Geographic expansion is planned cautiously with entry into California's excess & surplus lines market starting Q2 2026 followed by Connecticut later that year plus two additional states projected for rollout during 2027 [N1][S23][S29]. These markets were selected based on catastrophe profiles compatible with Kingstone’s underwriting expertise.

Execution risks include regulatory approval dependencies for market entry or exit plans as well as managing distributor scaling while maintaining underwriting discipline outside core territories [N1][S10].

Capital Allocation & Returns: Prudent Management Supports Strong ROE

Capital allocation improved materially with full prepayment of costly senior notes due mid-2026 via principal payments totaling nearly $6 million early in calendar year '25 reducing interest expense burdens significantly ([S8],[S15]).

Dividend payments resumed cautiously after dividend restrictions were lifted by regulators late in 2025; quarterly dividends of $0.05 per share were declared mid-year continuing into late-year payments with limits based on statutory surplus thresholds ([S8],[S16]).

Return on equity approximated ~33% for calendar ’25 calculated from statutory net income ($40.8M) over equity ($122.7M), reflecting efficient capital deployment despite ongoing regulatory constraints ([F1],[S8]).

Free cash flow exceeded $73 million after capex (~$2.8M), supporting operational reinvestment without external financing reliance ([F1],[S14]). This enhances flexibility for growth investments or acquisitions.

Challenges & Regulatory Environment: Exposure & Compliance Costs Persist

Key risks remain:

- Geographic concentration (~98% premiums from New York) heightens vulnerability to severe storm seasons despite elevated reinsurance protection ([S6],[S20],[S24]).

- Legislative changes removing prior anti-arson application requirements may increase underwriting information gaps ([S4],[S25]).

- New cybersecurity regulations effective early ’26 require enhanced CISO authority and incident reporting increasing compliance costs ([S17],[S19]).

- Recent regulatory examinations affirm capitalization but underscore ongoing scrutiny potentially limiting dividend capacity ([S4],[S8]).

- Market withdrawal restrictions necessitate approval potentially prolonging unprofitable business retention ([S10],[S13]).

Vigilant management balancing growth ambitions against risk controls remains critical.

Future Monitoring Points: Execution & Risk Controls Key to Strategy Realization

Areas warranting attention include:

- Sustaining premium growth aligned with combined ratio targets ensuring underwriting profitability amid evolving catastrophe trends ([N1],[S1]).

- Claims management effectiveness alongside reserve adequacy validated by independent actuaries ([S24],[F1]).

- Compliance with New York DFS cybersecurity standards plus potential federal insurance oversight developments ([S17],[N1]).

- Progress executing geographic expansion validating rate adequacy especially within California E&S segment’s distinct regulatory framework ([N1],[S29]).

- Maintaining strong risk-based capital ratios (~5.3x TAC/ACL) preserving buffers amid catastrophic event exposures ([S8]).

These metrics will shape realization of Kingstone's strategic ambitions while safeguarding underwriting culture and capital strength.

Disclaimer: Analysis based solely on publicly available data as of March 16th, 2026 from SEC filings and recent news transcripts without constituting investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments