Rise Gold Corp. Advances Amid Legal Battles and Capital Pressures

Rise Gold Corp. faces mounting legal and financial challenges while pursuing development of its Idaho-Maryland Mine property.

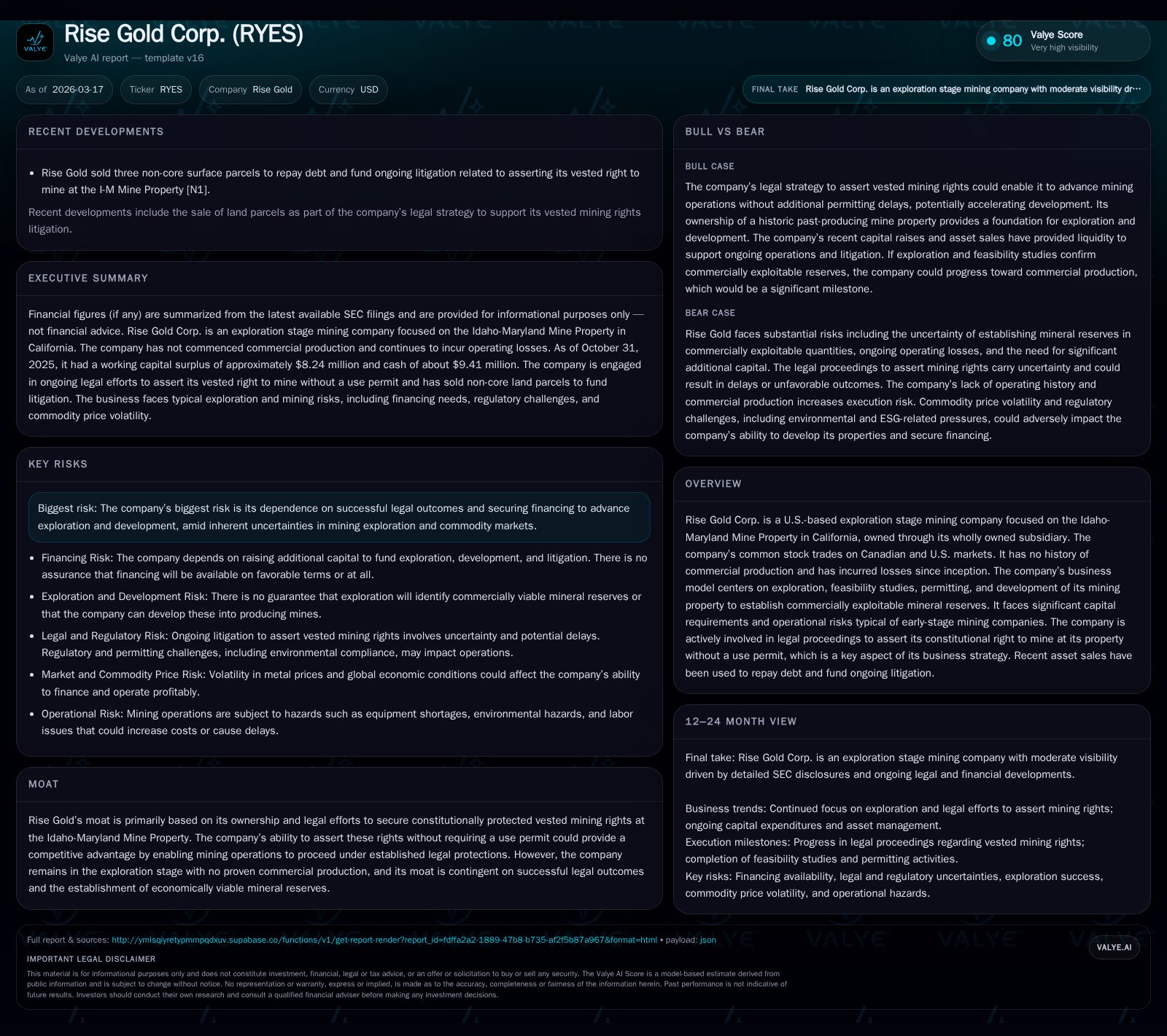

Rise Gold remains in exploration, incurring losses as it advances litigation to assert constitutional mining rights crucial for its Idaho-Maryland Mine property. The company’s historical financials show persistent negative earnings but marginally improved operating cash flows. Strategic partnerships and recent private placements have bolstered liquidity, enabling debt repayments and funding ongoing operations. However, significant operational risks persist related to legal outcomes, permitting uncertainties, and capital market volatility.

Tracing Rise Gold’s Financial Performance: Persistent Losses Through Exploration

Rise Gold Corp. continues to operate as an exploration-stage mining enterprise with no history of commercial production and a track record of losses since inception [F1]. Financial disclosures up to FY2025 reveal net losses amounting to approximately -$3.26 million, marking a slight improvement of roughly 8.6% compared to FY2024 results of -$3.57 million [F1]. This modest reduction signals some containment in expenditure growth but loss persistence.

Operating cash flow remains negative yet demonstrates notable progress. For FY2025, operating cash flow improved by about 47%, reaching approximately -$1.17 million from prior years exceeding -$2 million [F1]. Despite these improvements, the cash burn underscores the significant costs associated with extensive drilling, feasibility studies, and ongoing legal considerations typical for early-stage mining projects.

Equity fluctuated over recent fiscal years but ended FY2025 near $3.26 million down from prior peaks around $3.6 million [F1]. Calculations based on net income over equity imply an approximate ROE of -99.9%, consistent with exploration stage firms deploying capital ahead of revenue generation [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -3 | -1 | +8.6% |

| 2024 | -4 | -2 | +2.6% |

| 2023 | -4 | -2 | -5.7% |

| 2022 | -3 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -99.9 |

| 2024 | -150.0 |

| 2023 | -102.5 |

| 2022 | -96.3 |

Source: SEC companyfacts cache [F1].

Table shows loss persistence across four years ending July; operating income data not applicable post-2015 fiscal snapshots [F1].

The Moat of Mining Rights: Legal Battles Defining Competitive Positioning

Rise Gold’s primary competitive advantage hinges on its legal claim to constitutionally protected vested mining rights at the historic Idaho-Maryland Mine Property located near Grass Valley in California [S25][N1]. The company asserts that these vested rights exempt it from obtaining county use permits historically required for mining operations—a contention materialized through petitions submitted since September 2023 and the subsequent legal writ of mandamus in May 2024 challenging local regulatory decisions [S25][N1].

Court proceedings have seen mixed developments: notably in August 2025 a judicial ruling acknowledged Rise Gold's beneficial interest in the property sufficient to sustain its vested right claims [S25]. However, ongoing litigation remains unresolved with anticipated briefing schedules extending into late 2025 and beyond [S25]. This unresolved status distinctly frames legal risk as a make-or-break determinant for project advancement.

Should Rise succeed in establishing its constitutional rights under the Fifth and Fourteenth Amendments without requiring additional use permits ([S19]), it would significantly accelerate potential mine redevelopment timelines while circumventing lengthy regulatory bottlenecks that challenge other miners in California favoring protracted environmental review processes.

Conversely failure in courts could lead to debilitating permit barriers or halt progression entirely—a binary outcome making this legal positioning central to Rise Gold’s moat but inherently precarious.

Strategic Partnerships Boost Project Viability: The Morgan Hughes Agreement

In March 2026 Rise Gold formalized a strategic development partnership with Morgan Hughes Energy designed to advance the Idaho-Maryland Mine within the framework of U.S. domestic critical minerals initiatives [S3]. Morgan Hughes brings expertise in energy and minerals operations focused on aligning projects with federal industrial policy priorities targeting supply chain security for critical metals.

This alliance marks a transition from pure exploration toward structured development planning and capital formation efforts necessary for advancing feasibility studies and positioning the mine for future operational stages amidst evolving geopolitical priorities on mineral sourcing.

By integrating Morgan Hughes’ domain experience with Rise Gold’s asset base and jurisdictional advantages via its legal claims ([S3]), the partnership may facilitate more efficient access to government programs or incentivized funding mechanisms targeted at strategic mineral projects.

Capital Structure Evolution: Debt Repayment, Private Placements, and Liquidity Status

Capital formation has been a consistent priority as Rise Gold navigates high upfront expenditures amid no operational cash inflows. In calendar year 2025 alone the company completed two significant non-brokered private placements totaling approximately $10 million net proceeds through issuing shares coupled with warrants priced between $0.082 and $0.25 per unit [S4][S15]. Directors and officers participated substantially in these financings signaling internal confidence despite prevailing risks.

Concurrent debt management saw repayment of sizeable obligations including the entire $500K Myrmikan loan by mid-2025 as well as full settlement of Eridanus loan balances previously accruing high-interest charges compounded monthly ranging up to rates as steep as 25% per annum in longer periods [S4][S11][S15]. These actions reduced interest burden liabilities while clarifying balance sheet postures.

Liquidity metrics reflect improved current assets nearing $8.2 million against current liabilities below $750 thousand as January 31st on trailing period reported filings translating into a robust current ratio exceeding 11x—an unexpectedly healthy cushion for an explorer at this stage [F1][S4]. Such liquidity facilitates ongoing financing of exploration activities alongside continued litigation costs without immediate solvency pressure.

Notably there are no dividend distributions or share repurchase programs recorded aligning with industry standards for companies at pre-production phases focusing capital deployment internally rather than external returns [S15][S21][S23].

Operational Constraints: Risks from Market Volatility and Permit Challenges

Rise Gold explicitly acknowledges substantial operational risks stemming from volatile global economic conditions which exacerbate financing difficulties ([S2],[S22]). Fluctuations in metal price cycles coupled with tighter global credit markets heighten fundraising uncertainty jeopardizing the planned progressive expenditure profile needed for exploring mineralization extent or commencing development work.

Regionally specific risks center around intricate regulatory environments where local governmental opposition has manifested through denial of use permits despite company assertions of vested property rights ([N1],[S19]). The multi-front litigation increases administrative burdens alongside escalating legal costs. Further complicating is evolving ESG scrutiny which can indirectly augment compliance costs or provoke investor reservations about controversial mining projects even if not directly regulated under new policies ([S19]).

Cybersecurity concerns and physical risks such as natural disasters or infrastructure failures are recognized but weighted lower relative to overarching permit/legal uncertainties ([S19]). Collectively these factors portray a sophisticated risk matrix that stakeholders must monitor closely given their capacity to delay or derail the I-M Mine progression timeline.

Outlook and Milestones: What Future Developments to Monitor

Key upcoming events revolve around continued court proceedings relating to recognition of constitutive vested mining rights with initial briefs submitted by September-November timeframe per court stipulations signed fall 2025 [S25]. Outcomes here will likely determine whether Rise transitions significantly closer toward operational readiness or faces renewed regulatory constraints.

Concurrently progress within the Morgan Hughes collaboration may yield announcements detailing feasibility study advancements or strategic funding arrangements aligning with U.S critical mineral supply chain priorities ([N1],[S3]). These developments could materialize as public disclosures or SEC filings throughout remainder fiscal year 2026.

Monitoring additional private placement activity will be crucial as existing working capital extends only finite runway given sustained negative cash flows [F1],[N1],[S22]. Any shifts in metal price sentiment or macroeconomic stability factors impacting access to equity or debt markets also warrant continuous review given their outsized influence on junior miners’ survival prospects.

Capital Allocation Patterns: Assessing Returns, Cash Flows, and Shareholder Impact

Reflecting its early-stage status without revenue realization Rise Gold exhibits persistently negative returns on equity calculated near -99.9% consistent with ongoing net losses against comparatively modest shareholders’ equity balances at about $3.26 million [F1]. Free cash flow remains negative driven primarily by large operating expenses related predominantly to geological exploration plus heavy legal fees defending vested rights claims versus de minimis capital investment beyond routine sustaining measures ([F1]).

Allocations toward share-based compensation underscore efforts to incentivize executive retention amid challenging venture timelines aligned with stock option grants valued upwards of several hundred thousand dollars annually ([S15],[S21],[S23]). No dividends or buybacks have been initiated highlighting strict reinvestment discipline necessary at this juncture prioritizing asset advancement over direct shareholder returns.

Overall capital consumption patterns align tightly with managing complex litigation needs combined with exploration activities focused on delineation success thresholds before shifting into full-scale development phases which remain speculative pending favorable legal rulings.

Disclaimer: This analysis is based solely on publicly available information as of March 17, 2026. It is not investment advice nor an endorsement of any securities mentioned herein. Readers should conduct independent research before making any financial decisions.

Comments