Hudson Technologies Confronts Revenue Headwinds and Contract Uncertainty with Proprietary Refrigerant Services

Hudson faces sharply declining revenues and profit pressures amid commodity price volatility and an unsettled Defense Logistics Agency contract renewal.

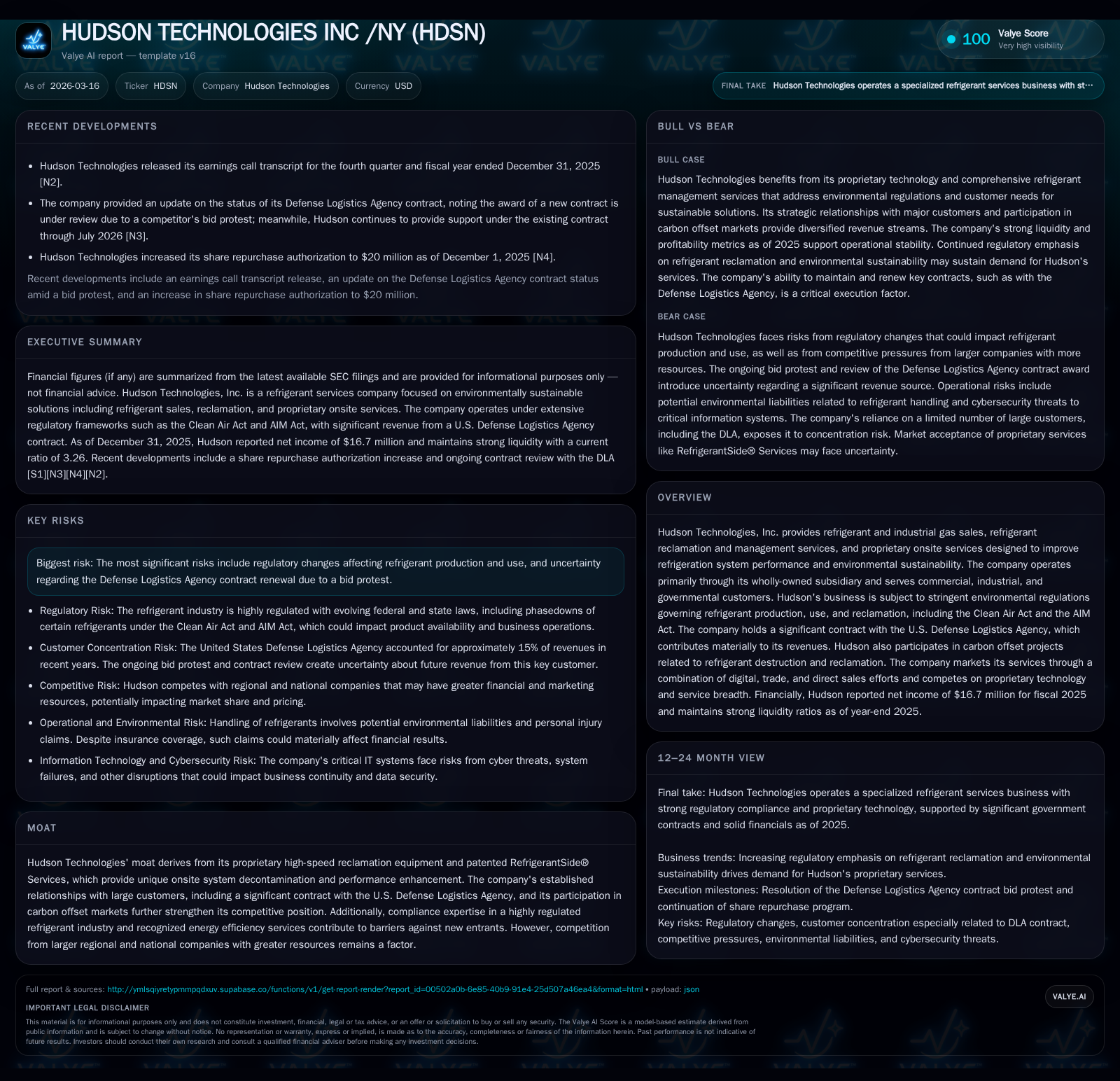

Hudson Technologies, specializing in refrigerant sales and reclamation services anchored by proprietary RefrigerantSide® technology, has experienced significant financial erosion from FY2022 to FY2025 driven by fluctuating refrigerant commodity prices and seasonal demand shifts. A major uncertainty hangs over its material U.S. Defense Logistics Agency contract, currently under bid protest, clouding future revenue visibility. While the company leverages patented onsite decontamination services and carbon offset projects as competitive differentiators, these have yet to offset the revenue declines or alleviate capital constraints caused by negative free cash flow and tight asset-based lending covenants.

Recent Financial Performance: Growth Erosion Amid Market Volatility

Hudson Technologies has witnessed pronounced financial contraction over the last four fiscal years. Revenue peaked at approximately $325 million in FY2022 before descending sharply by 18% to $237 million in FY2024 [F1]. Operating income contracted even more dramatically from $132 million in FY2022 to roughly $29 million in FY2024 before plunging to just $18.6 million in FY2025 [F1]. Net income followed suit with a steep decline from over $103 million in FY2022 to about $16.7 million in FY2025 [F1]. Critically, operating cash flow dropped from a robust positive $63 million in FY2022 to negative $3.2 million in FY2025, pushing free cash flow into negative territory (approximately -$8.2 million after capex) [F1].

This deterioration is largely attributable to volatility in refrigerant commodity markets and seasonality impacting both volume and pricing, as inventories must be valued at the lower of cost or net realizable value, subjecting Hudson to write-down risks when prices weaken [S1],[S10]. The company's exposure to substantial inventory levels exacerbates these risks.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17 | -3 | 19 | -31.7% | ||

| 2024 | 237 | 24 | 92 | 29 | -18.0% | -53.3% |

| 2023 | 289 | 52 | 59 | 78 | -11.1% | -49.7% |

| 2022 | 325 | 104 | 63 | 132 | +68.7% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 20 | -8 | 6.8 |

| 2024 | 8 | 87 | 9.9 |

| 2023 | 55 | 22.8 | |

| 2022 | 59 | 59.4 |

Source: SEC companyfacts cache [F1].

All figures rounded; CAGR reflects compound measures based on available fiscal year data [F1].

The Strategic Role of RefrigerantSide® Services and Proprietary Technology

Hudson's core competitive moat lies in its RefrigerantSide® Services—proprietary onsite system decontamination processes employing patented high-speed reclamation equipment such as the Zugibeast® system [S1],[S14]. These services remove moisture, oils, and contaminants directly at customer locations, restoring refrigeration systems closer to original design capacity while improving energy efficiency—a critical performance metric under stringent regulatory scrutiny.

Unlike simple refrigerant resale, these proprietary offerings enhance system longevity and reduce additional refrigerant manufacturing needs through reclamation—an issue of prime importance given the phaseouts mandated by environmental statutes [S14],[S17]. Additionally, Hudson operates two of only four AHRI-certified laboratories nationwide, underscoring its leading capability in ensuring reclaimed refrigerants meet purity standards [S16].

By integrating predictive diagnostics such as Chiller Chemistry® and SmartEnergy OPS®, Hudson provides clients real-time actionable insights that further differentiate its service offerings beyond commoditized refrigerant sales [S18]. This technical sophistication supports client retention especially among large industrial and governmental customers.

Defense Logistics Agency Contract: Uncertainty Clouds Future Revenue

The U.S. Defense Logistics Agency (DLA) constitutes a crucial revenue pillar for Hudson, consistently representing over 10-15% of total revenues—$38.2 million recognized in FY2025 alone—with corresponding accounts receivable concentrations [S4],[S9]. Since July 2016 Hudson has been the prime contractor for a multi-year DLA contract supplying refrigerants and related logistics.

In October 2025, Hudson was awarded a new five-year contract (with an optional five-year extension); however, this award was immediately contested via bid protest at the U.S. Court of Federal Claims by a competitor [S8],[S11]. Consequently, the DLA rescinded the award pending re-evaluation but allowed Hudson to continue current operations under the expiring contract through July 2026.

This scenario introduces acute uncertainty about ongoing government revenue streams beyond mid-2026, underscoring customer concentration risk typical within federal contracting contexts where lengthy procurement cycles and protests are common [S7],[S8]. Cash flow predictability remains impaired until bid protest resolution expected later in mid-2026 per recent earnings call commentary [N1].

Market and Regulatory Dynamics Shaping Refrigerant Sales

Hudson’s business is deeply influenced by extensive environmental regulations chiefly governed by the Clean Air Act amendments and the AIM Act which aggressively phase out virgin production of ozone-depleting substances like CFCs and HCFCs by end-2030 while progressively limiting HFCs [S1],[S25],[S26]. These policies mandate refrigeration equipment operators minimize emissions via recovery and reclamation practices enforced through EPA certification programs [S17].

Inventory valuation challenges arise due to commodity price fluctuations exacerbated by market supply constraints tied to regulatory quotas—forcing lower-of-cost-or-market write-downs that erode margins notably during downturns [S10],[S20]. Additionally, compliance costs required for licensed handling, transport (regulated as hazardous materials), quality testing (AHRI standards), and storage elevate operating expenses.

Despite headwinds from regulated virgin product scarcity accelerating HFC phasedown schedules (85% reduction by developed countries through mid-century), reclamation services like those of Hudson gain strategic significance as essential supply chain components exempt from production allowances [S26],[S19].

Capital Structure, Liquidity Stress, and Funding Outlook

Hudson manages liquidity primarily via an asset-based lending facility secured with Wells Fargo Bank capped at $40 million that limits borrowing tied to asset levels and contains restrictive covenants impacting financial flexibility [S6],[S18],[S27],[S28].

The decline into negative operating cash flow (-$3.16 million in FY2025) coupled with steady capital expenditures (~$5 million annually) results in negative free cash flow nearing -$8.2 million last fiscal year [F1]. This deterioration raises concerns about Hudson’s ability to sustain operations without augmenting financing sources beyond its existing ABL.

Management flagged potential requirements for additional debt or equity capital if inventory acquisition costs rise or RefrigerantSide® business development demands increase but has no current arrangements approved for such funding outside current credit facilities [S1],[S6]. Covenant breach risks persist given these liquidity pressures which could force accelerated debt repayment or operational curtailment absent lender waivers.

Environmental Innovation: Monetizing Carbon Offsets as Growth Catalyst

Capitalizing on growing decarbonization mandates, Hudson participates actively in carbon offset markets through projects linked to destruction and reclamation of potent greenhouse gases including CFCs and HFCs [S4],[S19]. These initiatives generate Verified Emission Reductions (VERs) which convert into tradable carbon credits under registries like American Carbon Registry.

Monetization of these VERs creates incremental revenue streams aligned with sustainability trends appealing both environmentally conscious customers and investors seeking ESG-compliant exposure [S4],[S19]. Such carbon offset generation differentiates Hudson within the refrigeration services industry while reinforcing compliance with federal environmental policies.

What to Watch: Contract Outcomes and Inventory Price Fluctuations

Key near-term catalysts will center on timely resolution of the DLA bid protest—expected sometime after July 2026—and whether Hudson retains or potentially loses this critical contract revenue source per latest earnings disclosures [N1],[S8].

Additionally, persistent volatility in refrigerant inventory market prices necessitates close monitoring since unfavorable net realizable value adjustments could further impair margins or cash flows going forward [F1],[S10]. Fluctuations derive from unpredictable weather patterns affecting seasonal demand as well as supply-side policy shifts.

Investors should also observe any updates concerning regulatory developments especially revisions of EPA’s Technology Transition Rule anticipated later in 2026 that may alter compliance cost bases or production quotas relevant to Hudson’s product portfolio [S26].[N1]

Shareholder Value: Buybacks, Dividends, and Return on Equity Trends

Despite earnings pressure, management maintained share repurchases around $20 million during FY2025 following an increase from approximately $8 million in the prior year enabled by amendment relief on stock buyback restrictions embedded within their credit agreement [F1],[S27]. This suggests attempts at capital return engagement balancing against tight liquidity.

Meanwhile return on equity remains modest at roughly 6.8%, reflecting diminished net income paired with relatively stable equity levels hovering near $243 million as of year-end 2025 [F1]. No meaningful dividends were declared or mentioned indicating buybacks serve as primary shareholder remuneration strategy given present operating conditions.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations regarding any security or company discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments