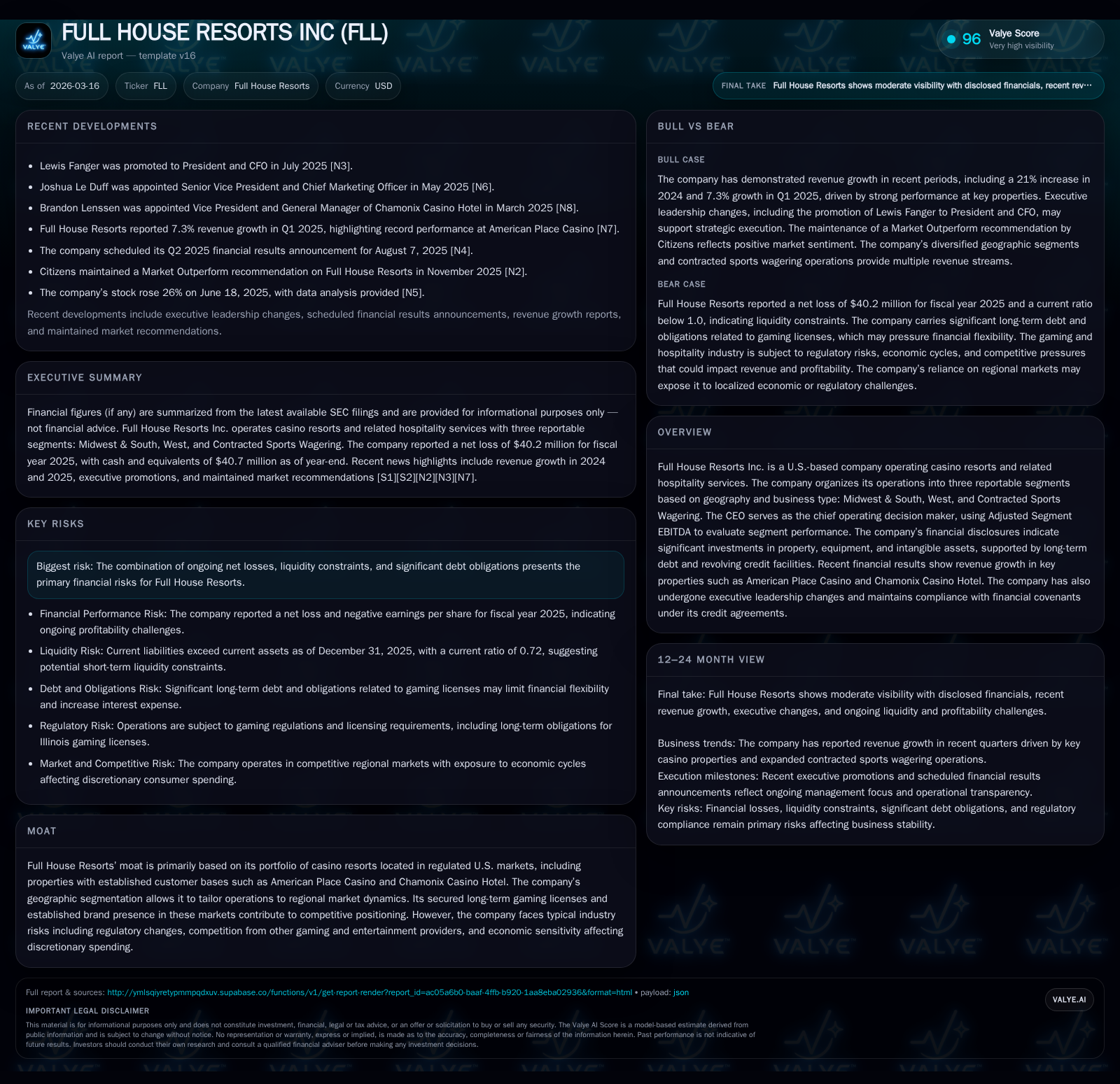

Full House Resorts’ Recovery Efforts Strained by High Debt and Cash Flow Challenges

The company’s modest revenue growth contrasts with ongoing losses and heavy leverage, testing its financial flexibility.

Full House Resorts Inc. operates a portfolio of U.S.-based casino resorts segmented geographically and has recently completed key property developments, including Chamonix Casino Hotel. While revenue showed a moderate annual increase of about 10.5% in 2025, net losses remain substantial, driven by high interest expenses and operating costs amid liquidity constraints. The company’s capital structure features $450 million in senior secured notes due in 2028 and a revolving credit facility, with liquidity supported by steady but diminishing cash flow from operations. Full House’s recovery hinges on improving operating profitability at its core properties and managing debt maturities without dilutive capital raises.

Company Overview

Full House Resorts Inc. is a U.S.-based casino resort operator with a portfolio segmented into three key areas: Midwest & South, West, and Contracted Sports Wagering [S22][S26]. The company strategically manages operations tailored to these geographic markets which differ in regulatory frameworks and customer demographics. Notable recent developments include the phased opening of the Chamonix Casino Hotel in October 2024 and the operation of the temporary American Place facility launched in early 2023 [S11][S18][S12].

Historical Performance

Financial performance through FY2025 shows gradual top-line growth with underlying profitability challenges common within regional gaming operators undergoing development cycles.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -40 | 10 | 3 | 13 | +1.2% |

| 2024 | -41 | 14 | 3 | 53 | -63.3% |

| 2023 | -25 | 22 | -1 | 149 | -68.2% |

| 2022 | -15 | 4 | 13 | 171 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | -1583.8 |

| 2024 | -39 | -100.4 |

| 2023 | -126 | -32.0 |

| 2022 | -167 | -14.8 |

Source: SEC companyfacts cache [F1].

Source: [F1]

Revenue grew to approximately $161 million in FY2025, continuing a long-term upward trend reflecting new property openings [F1]. Operating income returned to positive territory at about $3.1 million after prior volatility including losses in FY2023 [F1]. Despite this improvement, net income remained significantly negative at over $40 million primarily due to interest expenses associated with substantial long-term debt [F1].

Operating cash flow declined roughly 28% year-over-year to around $10 million as capital expenditures slowed following completion of major projects such as Chamonix Casino Hotel [F1][S11][S18][S19]. Capital spending dropped sharply from above $52 million in FY2024 to nearly $12.7 million in FY2025 [F1], marking a transition from development phase toward operational focus.

Equity has been substantially eroded by cumulative losses, falling from about $40 million at the end of FY2024 to just $2.5 million by end-FY2025 [F1], indicating significant pressure on shareholder value.

Drivers of Past Growth

Growth initiatives centered on:

- Completion and phased opening of Chamonix Casino Hotel in October 2024, financed largely through senior secured notes issuance [S11][S12].

- Launch of American Place temporary facility starting March 2023 supporting market presence during permanent facility design stages [S12][S18].

- Divestiture of Stockman’s casino real estate finalized by April 2025 to reallocate capital and streamline operations [S24].

These strategic moves were primarily funded through debt offerings supplemented by earlier equity financing rounds.

Capital Structure and Liquidity Position

The company's capital structure is characterized by significant leverage:

- Senior Secured Notes totaling $450 million due February 15, 2028 bearing an annual fixed coupon rate of 8.25% form the backbone of long-term debt financing [S11][S12][S18].

- A revolving credit facility up to $40 million maturing January 1, 2027 provides working capital flexibility; borrowings ranged between $25-$30 million during mid-2025 [S4][S7][S9].

- Debt issuance costs are being amortized but materially affect reported net debt balances [S11][S18].

The company remains compliant with covenants tied mainly to Adjusted EBITDA coverage ratios as of late-2025 [S4]. However, liquidity is constrained with a current ratio near 0.72 indicating current liabilities exceed current assets [F1]. Year-end cash balances approximated $40.7 million but were offset by current liabilities totaling about $73.5 million requiring careful cash management ahead of debt maturities [F1].

Segment Profitability Insight

Management tracks performance through Adjusted Segment EBITDA across three operating segments:

- Midwest & South: Mature markets providing relatively stable cash flows.

- West: Includes newer properties such as Chamonix generating developing contributions post-opening.

- Contracted Sports Wagering: Emerging segment expanding amid wider legalization trends nationally.

Investment outlays continue to suppress near-term profitability particularly in the West segment while Midwest & South remain more stable [S26].

Forward Growth Prospects and Constraints

Growth Catalysts:

- Continued ramp-up of new facilities including plans for permanent American Place buildout may expand revenue base (timing details not explicitly disclosed).

- Expansion opportunities via contractual sports wagering arrangements could generate incremental revenues across legalized markets.

- Operational efficiencies expected as development projects mature may improve margins if effectively managed.

Constraints:

- Significant fixed interest obligations limit net earnings growth absent margin improvements or refinancing strategies.

- Regulatory risks related to licensing, fees, and operational restrictions pose ongoing challenges typical for regional gaming operators [S10][S21].

- Competitive pressures from larger integrated resorts and online wagering platforms threaten market share gains.

- Tight liquidity limits ability to pursue acquisitions or aggressive marketing needed for rapid growth acceleration.

Capital Allocation Policy

Current financial constraints dictate limited shareholder returns:

- No dividends have been declared or resumed amid substantial net losses and focus on deleveraging balance sheet (no explicit dividend data provided).

- No share repurchase programs indicated given financial conditions (not disclosed).

- Capital expenditures have been curtailed post-heavy investment phases aligning with efforts to conserve free cash flow despite an approximate negative free cash flow position of about $2.7 million in FY2025 (calculated as operating cash flow minus capex) [F1].

Risks Highlighted

Risk disclosures emphasize: "Ongoing net losses combined with liquidity challenges amid substantial debt obligations present principal financial risks." Regulatory variability further compounds operational uncertainties for casino operators reliant on state/local gaming permissions [S10][S21].

Summary Analysis Outlook

Full House Resorts faces a critical juncture balancing stabilized revenue growth following major investments against persistent losses and high leverage eroding equity value. Success depends on operational efficiency gains coupled with prudent debt management toward the senior notes maturity horizon in early 2028.

Key monitoring areas include adjusted EBITDA trends per segment, covenant compliance under credit agreements, cash flow sufficiency relative to upcoming debt maturities, and progress toward permanent facility development especially regarding American Place transition.

If operational improvements materialize alongside controlled capital expenditure replacing historically high upfront investments, Full House may advance toward stronger returns prospects beyond the medium term.

This analysis is based exclusively on publicly available company financial statements filed with the SEC as of March 16, 2026 ([F1]-[S29]) without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments