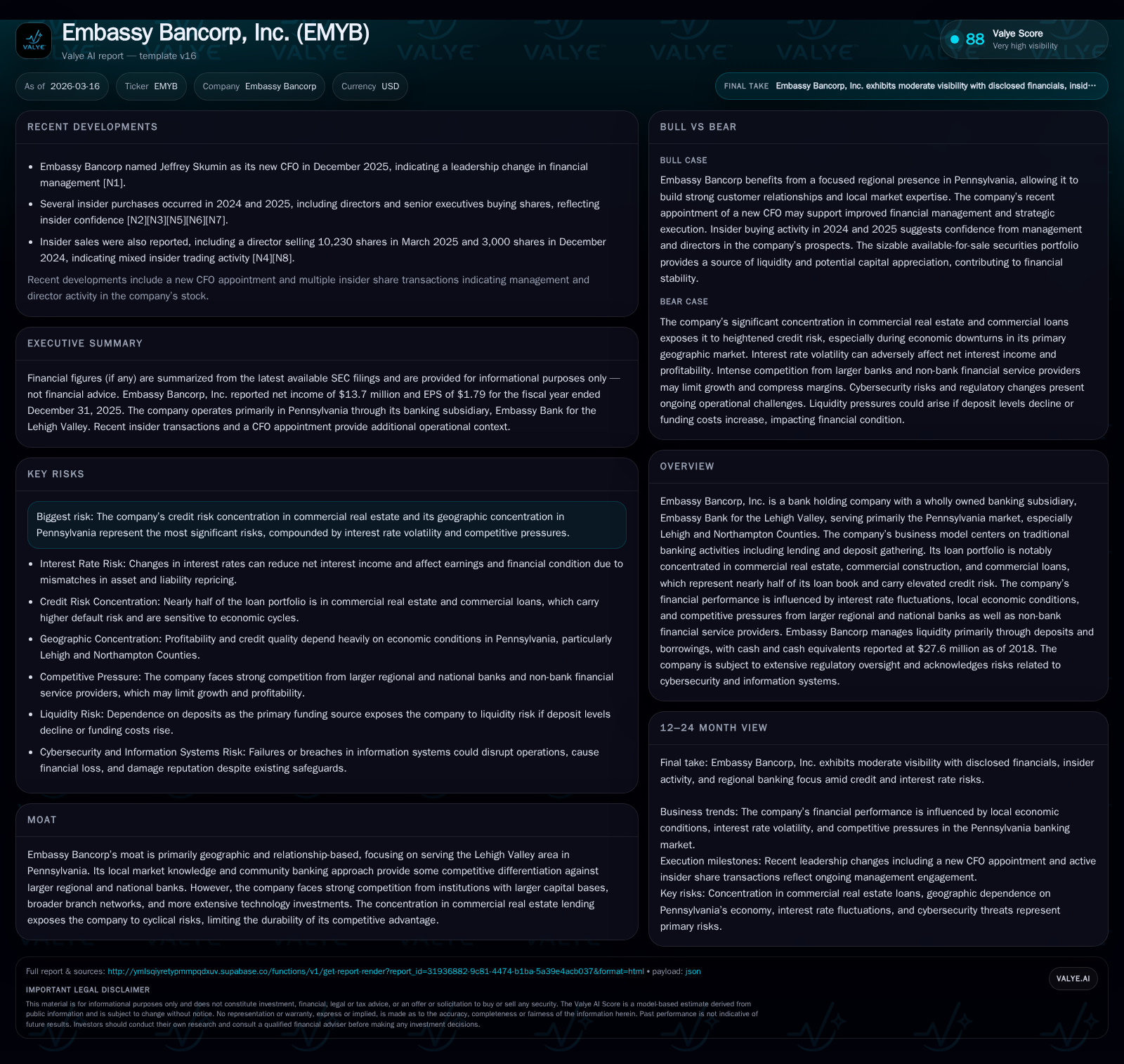

Embassy Bancorp's 31% Net Income Rise Tempered by Commercial Real Estate Concentration and Local Market Risks

The Pennsylvania-focused bank holding company shows robust income growth but faces strategic and credit concentration challenges.

Embassy Bancorp, Inc. operates primarily in the Lehigh Valley, Pennsylvania, focusing on traditional lending and deposit activities. Its 2025 financials reflect a solid 31% net income increase to $13.7 million, supported by growing equity and operating cash flows. However, significant concentration in commercial real estate loans and geographic exposure to a single local economy impose elevated credit and competitive risk. Capital ratios remain well above regulatory standards, with modest capital returns through dividends and buybacks. Going forward, interest rate volatility, regional economic conditions, and competitive dynamics from larger banks will be key variables influencing growth and profitability.

Company Overview

Embassy Bancorp, Inc., headquartered in Pennsylvania, operates through its wholly owned subsidiary Embassy Bank for the Lehigh Valley. The company concentrates its banking services geographically in the Lehigh Valley region—primarily Lehigh and Northampton Counties—leveraging local expertise and community banking relationships. Its core activities include deposit gathering and lending, with an emphasis on commercial real estate, commercial construction, and broader commercial lending segments that constitute close to half of its loan book [S18][S19].

Historical Performance Drivers

The past four years reveal fluctuations influenced by macroeconomic conditions and local market trends. Net income fell from approximately $17.7 million in 2022 to $10.4 million in 2024 before rebounding sharply to $13.7 million in 2025—a gain of over 31% year-over-year [F1]. This recovery reflects improved net interest income management amid shifting interest rates alongside effective cost controls.

Equity rose steadily from $88.3 million in 2022 to $127.6 million in 2025, driven by retained earnings accumulation [F1]. The resultant approximate return on equity for FY2025 stands near 10.7%, signaling solid profitability for this bank holding company size.

Operating cash flows have varied: after declining below $10 million in FY2024 alongside earnings compression, they rebounded to exceed $12 million in FY2025 enabling roughly $12.2 million free cash flow following about $0.6 million annually on capital expenditures [F1].

Dividend payments consistently returned cash to shareholders (around $3-3.7 million annually), while share repurchases have been minimal (<$100k total except a trace $11k buyback in FY2025), indicating dividends as the primary capital return method [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 14 | 13 | 632000 | +31.2% |

| 2024 | 10 | 10 | 739000 | -17.5% |

| 2023 | 13 | 19 | 806000 | -28.5% |

| 2022 | 18 | 20 | 719000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 4 | 11000 | 12 |

| 2024 | 3 | 72000 | 9 |

| 2023 | 3 | 132000 | 19 |

| 2022 | 3 | 100000 | 19 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures primarily relate to branch upgrades or IT systems enhancing operational efficiency.

Loan Portfolio Composition and Credit Concentration

As of mid-2025 reporting dates, loans outstanding totaled approximately $1.27 billion distributed as follows: commercial real estate loans represented about 43% ($551 million), commercial construction loans around 1-2% ($17-22 million), commercial loans near low single digits (3%), residential real estate above half (53%), and consumer loans negligible (0.04%) by composition [S18][S19].

This concentration toward commercial real estate elevates exposure to sector-specific risks linked to property market cycles and refinancing challenges if local economic conditions deteriorate or interest rates rise sharply.

While some nonperforming or impaired loan balances exist mainly within the commercial real estate segment, no alarming credit loss provisions have been highlighted [S18].

Interest Rate Risk Management

Embassy Bancorp’s earnings substantially depend on net interest margin spreads between asset yields and funding costs.

The company notes that liabilities such as deposits can reprice faster than assets during rising rate environments potentially compressing margins temporarily; conversely falling rates may reduce asset yields faster than liability costs lowering income generation capability [S1].

Management applies asset-liability duration control techniques aimed at balancing repricing schedules but acknowledges inherent limitations under rapid or unexpected rate volatility scenarios that could materially impact net interest income [S1].

Competitive Environment and Geographic Moat

The company’s moat derives from geographic concentration within Pennsylvania's Lehigh Valley area leveraging deep local relationships.

However, this focused footprint exposes it to intense competition from larger regional and national banks with greater capital resources enabling larger loan sizes and superior technology investments attracting digitally savvy customers [S15].

Non-bank competitors such as credit unions also contest deposit pricing and specialty products further pressuring traditional community bank niches [S15].

Liquidity Profile and Capital Adequacy

Deposits constitute Embassy’s principal liquidity source supplemented by Federal Home Loan Bank (FHLB) borrowing capacity exceeding $700 million secured against qualifying assets [S4][S11].

As of late-2025 periods examined, no long-term FHLB advances were outstanding; short-term usage was minimal or nil [S4].

Additional liquidity lines include unsecured federal funds lines of credit around $10 million plus revolving credits near $7-10 million under ancillary agreements providing further funding options [S4].

Regulatory capital ratios consistently exceed "well capitalized" thresholds protecting against regulatory actions or forced capital raises [S11]. The company cautions that future equity raises depend largely on external market conditions affecting timing and terms if needed [S11].

Growth Outlook Considerations

Growth prospects center on deepening local deposit bases and expanding loan originations where customer relationships foster new business opportunities.

However, growth is constrained by geographic concentration exposing results to regional economic downturns—including employment shocks or real estate declines prevalent in Pennsylvania markets served—as noted by management risk disclosures [S15].

Competitive pressures from better-capitalized rivals with advanced digital platforms may limit pricing power on deposits and loans restricting margin expansion [S15].

Interest rate uncertainty could also disrupt stable net interest margins causing earnings volatility challenging for a midsize institution lacking substantial hedging scale or diversification [S1].

Monitoring indicators such as non-performing loan trends within commercial real estate segments, deposit growth relative to competitors, margin preservation despite rate swings, and regulatory changes impacting capital requirements will be critical benchmarks going forward.

Capital Allocation Summary

- ROE at approximately 10.7% for FY2025 indicates steady profit generation relative to equity base for a community-focused player but moderate compared to larger peers [F1].

- Operating cash flows after capex suggest robust free cash flow supporting consistent dividend payments around $3–3.7 million annually reflecting commitment to shareholder returns while preserving liquidity buffers [F1].

- Minimal share buybacks imply preference towards steady dividends possibly due to limited excess capital or prioritization of balance sheet strength given portfolio credit risks [F1].

Risks Highlighted by Management

- Credit concentration risk due to heavy exposure toward commercial real estate loans increases vulnerability should property values decline or borrowers face refinancing difficulties during adverse cycles [S21].

- Interest rate risk remains significant given potential margin compression if liability costs outpace asset repricing adjustments especially under volatile market conditions [S1].

- Competitive pressures from larger banks with deeper pockets investing heavily in fintech capabilities challenge traditional community bank market share expansion efforts [S15].

- Geographic concentration limits diversification benefits making performance sensitive to Pennsylvania's economic health without offsetting revenue streams elsewhere.

- Regulatory changes could increase compliance costs or constrain product offerings limiting future growth avenues.

- Cybersecurity threats require ongoing vigilance though no material breaches reported; management recognizes escalating electronic risk environment necessitating continuous investment.

Conclusion

Embassy Bancorp demonstrates solid recent financial improvement marked by meaningful net income growth accompanied by strong capital levels above regulatory minima ensuring operational viability amid cautious management of credit concentrations notably within commercial real estate lending.

Its regional focus offers relationship-driven banking advantages but imposes scalability constraints alongside exposure risks amplified by competitive intensity from larger institutions deploying superior technology platforms.

Future progress hinges on navigating inflationary headwinds controlling asset quality risks especially within CRE portfolios while maintaining disciplined liquidity management leveraging abundant FHLB borrowing capacity. Monitoring operational milestones like loan delinquency trends, deposit inflows versus competitors’, sustained margin preservation despite rate volatility will be crucial for assessing Embassy’s trajectory.

Disclaimer: This report is intended solely for informational purposes based on publicly available data as of March 16, 2026; it does not constitute investment advice nor an offer or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments