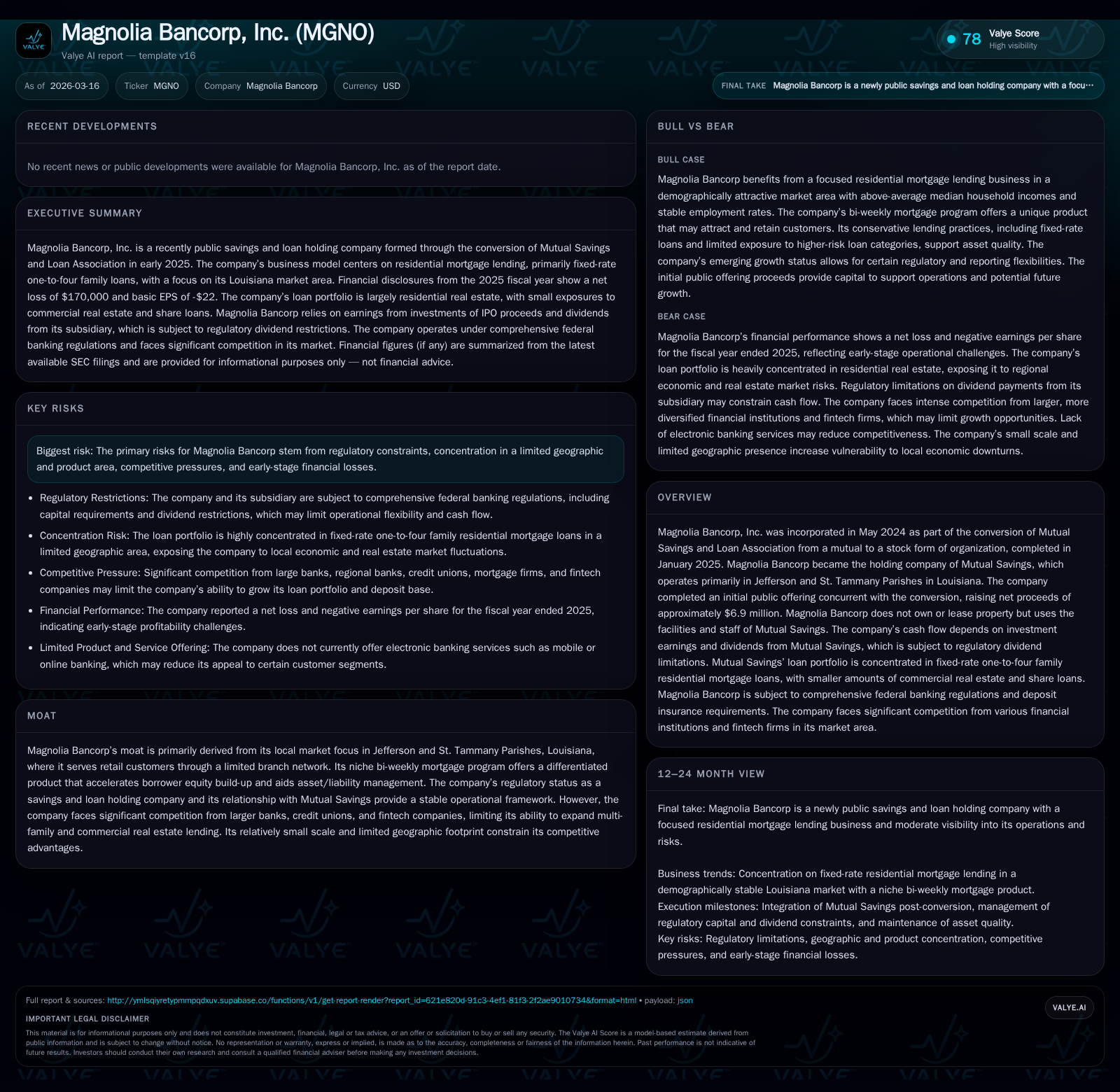

Magnolia Bancorp's Early Challenges Reflect Regulatory Constraints and Limited Geographic Focus

The bank holding company’s nascent public operations reveal growth limitations tied to its conversion structure, local market, and regulatory environment.

Magnolia Bancorp, Inc. was established in mid-2024 as part of Mutual Savings’ conversion from a mutual association to a stock holding company. Operating primarily in Jefferson and St. Tammany Parishes near New Orleans, Magnolia Bancorp’s revenue and cash flows hinge on dividends from its subsidiary Mutual Savings, which faces regulatory constraints on capital distributions. The company's loan portfolio remains narrowly concentrated in fixed-rate single-family residential mortgages with modest diversification. Financially, Magnolia Bancorp has reported consecutive net losses since inception with operating cash flow deficits, while building equity through retained proceeds from its January 2025 IPO. Future growth is contingent on the regional housing market, regulatory dividend allowances, and potential expansion of lending activities within its limited scale and scope.

Company Overview and Historical Performance

Magnolia Bancorp was incorporated in May 2024 following the decision by Mutual Savings and Loan Association to convert from a mutual savings institution to a stock holding company structure. This conversion completed in January 2025 simultaneously with an initial public offering that raised about $6.9 million in net proceeds after expenses [S1]. Post-conversion, Magnolia Bancorp became fully reliant on Mutual Savings as its sole operating subsidiary.

The company does not own or lease any physical property; instead, it utilizes Mutual Savings’ offices and staff resources without separate infrastructure commitments [S1]. As such, operational efficiency depends heavily on the subsidiary's performance.

Financially, Magnolia’s net income has been negative since inception: losses of $170K for FY2025 compared to $100K the previous year reflect early-stage costs typical of conversion-related expenses and nascent public company overheads [F1]. Operating cash flows are also negative ($439K in FY2025) slightly improving from -$470K in FY2024 with capital expenditures rising modestly due to initial investment outlays [F1]. Equity expanded nearly 44% YoY from $13.9M to almost $20M reflecting retained IPO capital rather than earnings applied retention [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -170000 | -439000 | 47000 | -70.0% |

| 2024 | -100000 | -470000 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -486000 | -0.9 |

| 2024 | -470000 | -0.7 |

Source: SEC companyfacts cache [F1].

Financials illustrate ongoing unprofitability with modest improvement in cash flow post-conversion.

Business Model and Market Focus

Operating primarily within Jefferson and St. Tammany Parishes—bedroom communities adjacent to New Orleans—Mutual Savings targets retail customers through two physical branches offering traditional deposit accounts such as checking, savings, certificates of deposit but no electronic banking yet [S1], [S22]. This reflects a conservative approach maintaining legacy delivery channels.

Their lending focus is predominantly fixed-rate one-to-four family residential mortgages which constitute about 97.8% of the loan portfolio by dollar volume ($30 million out of roughly $30.7 million total loans at end-2025) [S21]. The remaining book includes minor commercial real estate (about 1.5%) and secured shareholder deposit loans (~0.7%) [S21]. Construction loans were fully converted into permanent loans by year-end.

A distinguishing feature is their niche bi-weekly mortgage product aimed at accelerating borrower equity accumulation—a useful asset/liability management tool aligned with borrower preferences favoring quicker principal reduction versus traditional monthly schedules [S21]. Approximately three quarters of their loan portfolio consists of these bi-weekly fixed-rate loans.

Despite these specialized offerings, Magnolia Bancorp faces headwinds expanding into multi-family or broader commercial lending markets given scale constraints and competition from larger banks or fintech lenders who possess greater underwriting depth and tech-enabled platforms [S19].

Regulatory Environment and Capital Structure

As a federally supervised savings association holding company regulated primarily by the Office of the Comptroller of Currency (OCC), Magnolia Bancorp operates under stringent capital adequacy standards requiring common equity Tier 1 ratios above minimum thresholds such as 4.5% among other risk-based measures [S6],[S12]. At December 31, 2025, Mutual Savings met "well-capitalized" criteria indicating sufficient capitalization buffers available for operations within regulatory limits.

Dividend payments from Mutual Savings to Magnolia Bancorp are tightly controlled by regulation imposing dividend cap restrictions tied to earnings and capital retention requirements designed to protect depositor interests [S18],[S12]. This constrains cash flow availability at the holding company level which relies on these dividends alongside investment earnings from retained IPO proceeds for liquidity.

The allowance for credit losses is maintained conservatively relative to historical experience although management notes possible variability should economic conditions shift adversely for borrowers or collateral values unexpectedly decline [S8],[S26]. At year-end 2025 provision coverage reasonably matches minimal delinquency levels across a highly collateralized loan book concentrated in owner-occupied real estate loans.

Growth Prospects and Constraints

Future growth potential hinges on several key factors:

- Continued stabilization post-conversion enabling operational efficiencies.

- Incremental expansion within their niche residential mortgage lending supported by established presence in targeted parishes.

- Possible gradual diversification into selective construction lending if origination opportunities justify increased risk exposure.

- Regulatory allowance increases permitting higher dividend flows or reinvestment flexibility.

However, significant challenges temper optimism:

- The narrow geographic footprint limits scale economies compared with regional or national peers.

- Dependence on fixed-rate mortgages exposes earnings sensitivity to interest rate environments affecting asset/liability matching.

- Competitive pressure especially from digital-first lenders could erode market share absent technological upgrades.

- Potential tightening in regulatory capital or dividend policies could restrict financial flexibility further.

Management currently signals no immediate plans for aggressive geographic expansion or launching new banking subsidiaries; instead preferring an incremental organic path consistent with historical roots [S1],[S22],[S24].

Capital Allocation: Dividends & Buybacks

Following their recent IPO conversion event in early 2025, Magnolia Bancorp initiated its first stock repurchase program approved late in calendar year 2025 authorizing up to approximately 33,350 shares (~4% outstanding shares) intended primarily for employee retention plan fulfillment commencing January 15, 2026 [S24]. This modest repurchase activity aligns with early-stage publicly traded banks balancing shareholder return initiatives against regulatory caution.

No dividends have been declared or paid thus far; dividend distribution capability remains contingent upon sufficient earnings at Mutual Savings consistent with regulator evaluations emphasizing capital conservation buffers (2.5% over minimum risk-based requirements) and safety metrics adherence [S18],[S25]. Market watchers should monitor any updates related to dividend policy shifts or buyback program amendments as indicators of confidence or capital surplus deployment strategies.

Summary & Outlook Considerations

Magnolia Bancorp illustrates common transitional challenges typical for newly converted thrift holding companies emerging from mutual ownership structures into publicly listed entities. Its reliance on a localized business model centered on traditional fixed-rate residential mortgages reflects both strength in community ties and vulnerability vis-à-vis scale economies and evolving customer preferences for digital delivery platforms.

Financially fragile at inception with ongoing net losses offset by solid capitalization underscores a need for disciplined growth aligned with capital adequacy mandates and regulatory dividend constraints impacting free cash flow generation at the parent level.

Despite inherent risks—including geographic concentration coupled with competitive pressures from larger banks and fintech players—the firm’s niche bi-weekly mortgage offering provides some differentiation supporting borrower loyalty and internal asset/liability matching strategies.

Investors should watch upcoming quarterly filings for:

- Loan originations pace versus repayments trends indicating demand sustainability,

- Changes in allowance for credit loss reflective of portfolio credit quality shifts,

- Updates on dividend capacity or buyback utilization signaling improved core profitability,

- Any strategic moves toward technology investments or service expansions addressing digital banking gaps,

- Regulatory exam feedback impacting capital requirements or operational scope.

Disclaimer

This report is prepared solely for informational purposes based on publicly available documents including SEC filings as of March 16, 2026 ([F1], [S#]). It does not provide investment advice or recommendations nor does it reflect any confidential insights into Magnolia Bancorp’s internal plans beyond disclosed materials.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments