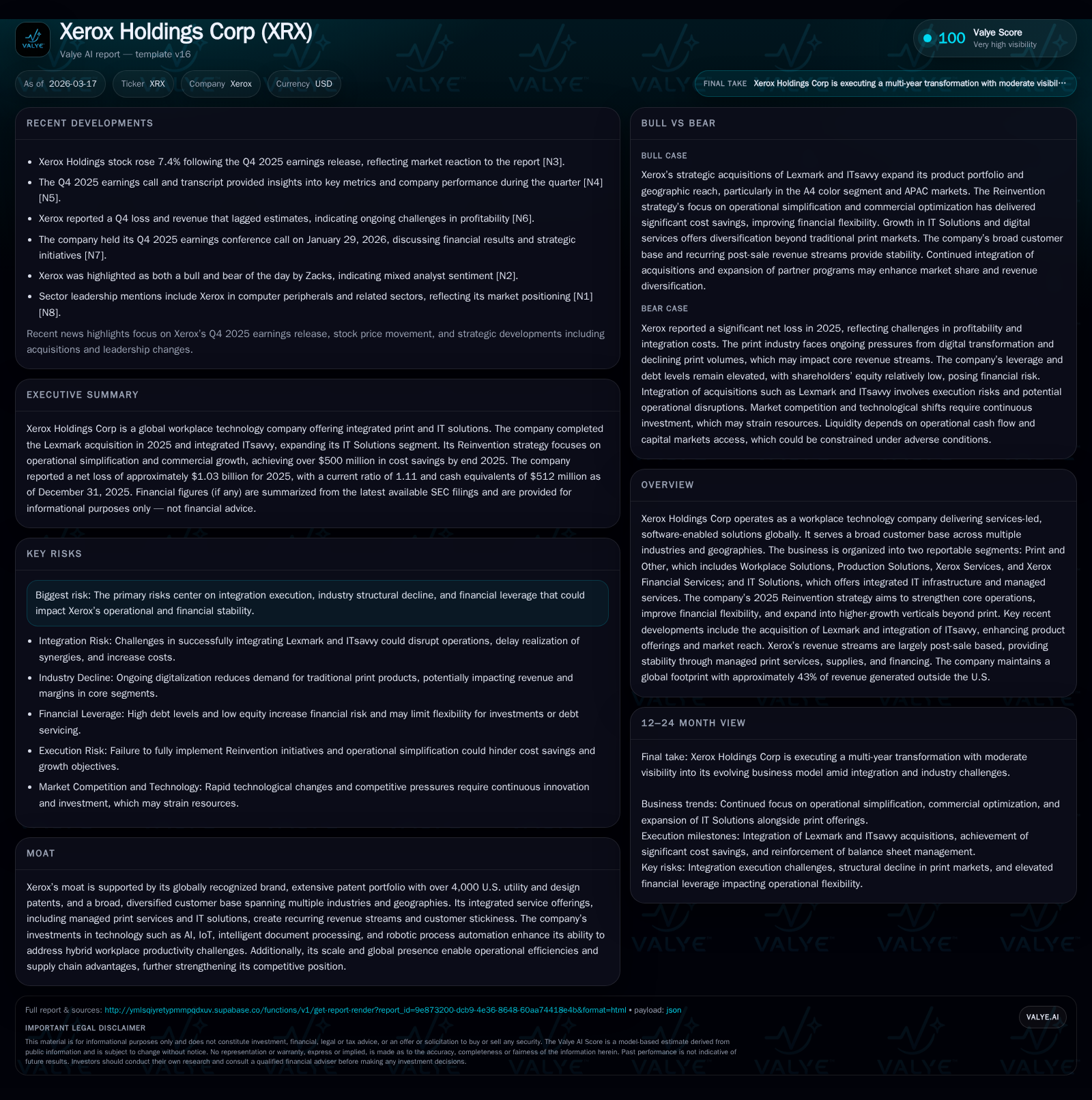

Xerox Holdings Transforms Print Legacy With Tech-Driven Reinvention

Xerox leverages acquisitions and innovation to shift from traditional print to integrated workplace technology.

Xerox Holdings Corp has embarked on a multi-year Reinvention strategy aimed at redefining its legacy print business by expanding into higher-growth IT and workplace solutions. This transformation is driven mainly by the 2025 acquisitions of Lexmark and ITsavvy, which broaden its product portfolio and geographic reach while boosting service-related revenue streams. Despite persistent challenges such as declining print demand and financial leverage pressures, Xerox maintains operational flexibility through cost savings, a strong patent base, and recurring post-sale revenues. Key milestones ahead include further integration of acquisitions and expansion in managed IT services.

Historical Revenue Trends and Profitability Challenges

Xerox’s top-line demonstrated modest growth fueled largely by acquisitions amid an industry characterized by secular print volume declines. Total revenues increased from approximately $6.22 billion in fiscal year (FY) 2024 to about $7.02 billion in FY2025 [F1], marking a roughly 13% rise partially attributable to the inclusion of Lexmark's portfolio and ITsavvy’s IT product lines.

However, profitability remains strained. Net income reported a significant loss of approximately -$1.03 billion in FY2025, an improvement on the deep loss of -$1.32 billion recorded in FY2024 but still reflecting enduring pressures on margins and cost structure [F1]. Operating cash flow decreased sharply by over half—from $511 million in FY2024 to $224 million in FY2025—driven by reduced finance receivable sales, acquisition-related expenditures, and working capital variances [F1]. Capital expenditures rose moderately to $37 million reflecting investments aligned with the company’s strategic pivot [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1029 | 224 | 37 | +22.1% |

| 2024 | -1321 | 511 | 27 | -132200.0% |

| 2023 | 1 | 686 | 29 | +100.3% |

| 2022 | -322 | 159 | 36 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 71 | 0 | 187 |

| 2024 | 141 | 8 | 484 |

| 2023 | 165 | 544 | 657 |

| 2022 | 174 | 113 | 123 |

Source: SEC companyfacts cache [F1].

Note: Revenue for FY2022 not stated explicitly; net income fluctuations illustrate volatility.

Drivers Behind the 2025 Reinvention Strategy

The strategic impetus behind Xerox’s Reinvention centers on countering its legacy print industry decline while expanding into faster-growing adjacent sectors through operational simplification and commercial optimization [S1]. The plan aims to strengthen core competencies, improve financial flexibility, and invest selectively into digital workplace solutions that integrate software, AI-enabled intelligent document processing (IDP), robotic process automation (RPA), and IoT technologies.

Demand shifts towards hybrid work environments and secure digital workflows are addressed through expanded IT infrastructure offerings designed to complement print hardware [S1]. Reinvention also targets cost reduction via greater procurement efficiency, consolidation of duplicate systems, inventory management enhancements, and digitization tools.

Strategic Acquisitions: Lexmark and ITsavvy Integration Impact

Lexmark’s acquisition completed in Q3 2025 added critical scale particularly within the A4 color print segment—a market expanding due to small-to-mid-sized office needs—and extended Xerox’s geographic presence into the Asia Pacific region [S1]. Lexmark also contributes manufacturing capacity that supports tariff mitigation strategies and supply chain flexibility.

Simultaneously, full integration of ITsavvy established Xerox's dedicated IT Solutions segment, significantly broadening its addressable market beyond hardware to include cloud migration services, cybersecurity offerings, managed IT infrastructure under service level agreements (SLAs), network management, and device lifecycle services [S1], [N1]. These high-margin services diversify revenue streams beyond traditional print hardware sales.

Nonetheless, integration risks remain material given complexities in harmonizing systems and cultures across formerly separate entities [N4]. Execution efficacy will be a key factor for sustained success.

Print Segment Dynamics Amid Industry Decline

The "Print and Other" segment—including Workplace Solutions, Production Solutions, Xerox Services, and Financial Services—remains challenged by secular headwinds such as declining page volumes exacerbated by digital alternatives [S7], [S16]. Equipment gross margins contracted significantly due to unfavorable product mix shifts toward lower margin offerings, incremental tariff-related costs on imported components largely mitigated by Lexmark’s footprint gains, but still pressuring unit economics [S16], [S18].

That said, managed print services provide recurring revenues anchored around installed base maintenance contracts that help stabilize cash flows despite equipment unit sales softness [S24]. The broadened portfolio enables cross-selling opportunities but margin compression remains a persistent theme.

Emergence of IT Solutions as Growth Catalyst

The newly formed IT Solutions segment showed substantial growth momentum primarily driven by ITsavvy’s contributions as well as increased client demand for integrated cloud architectures, cybersecurity programs, network migration services, and managed infrastructure solutions [S24], [S7], [N1]. The business emphasizes defined SLAs enhancing customer retention through service reliability guarantees.

IT products revenue more than doubled year-over-year while services grew strongly as Cisco-like solutions expanded the TAM beyond traditional print-centric budgets [S26], [S27]. This segment operates predominantly in North America and Europe with pockets of emerging activity globally.

The strategic shift aligns with broader industry technology transitions where value pools increasingly reside in software-enabled service delivery rather than standalone hardware sales.

Capital Allocation: Balancing Debt, Cash Flow, and Returns

Xerox’s capital strategy must navigate rising core debt levels resulting from acquisition financing combined with investment needs for reinvention initiatives [F1], [S4], [S5], [S6]. Total debt climbed from about $3.4 billion in FY2024 to roughly $4.25 billion at the end of FY2025; notably over half pertains to non-finance operating debt while remainder supports finance receivables assets per a targeted ~7:1 leverage model [S5], [S21].

Returns remain negative as indicated by an approximate -232% ROE calculated from net losses relative to equity around $444 million at year-end [F1]. Free cash flow after capex is positive but compressed at an estimated $187 million for FY2025, tightening operational flexibility compared to prior years when cash generation was more robust.

Dividend payments were scaled down considerably—from $141 million distributed in FY2024 down to $71 million in FY2025—with no share repurchases executed amid preservation priorities [F1].

Navigating Financial Leverage and Liquidity Constraints

Despite elevated leverage ratios coupled with issuance of high-yield secured Senior Notes carrying coupon rates between approximately 10% to above 13% maturing between 2026–2031 [S4], Xerox maintains liquidity buffers including roughly $565 million cash reserves as of Dec-31-2025 plus undrawn availability under asset-based lending arrangements exceeding $289 million net exposure after letters of credit issuance limitations [S6], [F1].

Ongoing finance receivables sales programs augment liquidity but are subject to market conditions which could tighten access if economic stress occurs.

Interest expense pressures are expected to rise correspondingly impacting future operating profitability until leverage reduction strategies advance further.

Key Performance Metrics: What Past Data Reveals

Analyzing key metrics:

- Revenue growth has been uneven but positive since the Lexmark acquisition boosted scale (+13% YoY through FY25) [F1].

- Operating cash flow declined sharply (-56% YoY) reflecting changing cash collection patterns on finance assets along with acquisition spend impact underscoring operating challenges early in reinvention phase.

- Capital spending is stepping up modestly (+37% YoY) indicating increased investments into technology transition while remaining conservative overall.

- Dividend distributions have halved signaling cautious capital returns stance given prevailing losses.

- Equity base erosion reflects cumulative losses impairing balance sheet capacity requiring careful leverage management going forward.

These data points illustrate both progress achieved via scale expansion alongside structural hurdles inherent to legacy product decline transition dynamics.

Outlook and Milestones to Monitor in Xerox’s Transformation

Looking ahead under analysis:

- Successful integration outcomes for Lexmark manufacturing efficiencies will be pivotal for cost mitigation relative to tariff headwinds.

- Growth trajectory for IT Solutions adoption including managed security services should be monitored closely for revenue diversification validation.

- Operating margin improvement will hinge on continuing cost simplification savings beyond the stated >$500 million cumulative run-rate target achieved end-2025.

- Liquidity management factors including debt refinancing or deleveraging will be critical as secured notes mature starting mid-2026 period presenting refinancing risk windows.

- Adoption of AI/IoT-enabled workflows within software-led offerings could catalyze new productivity gains aligning closely with hybrid work trends described internally.[N1]

Absent explicit published guidance beyond these milestones, investors should watch reported quarterly results for signs of accelerating synergy capture across multi-segment operations driven by digital transformation velocity.

Disclaimer: This analysis does not constitute investment advice or recommendations. It synthesizes publicly available data for informational purposes only.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments