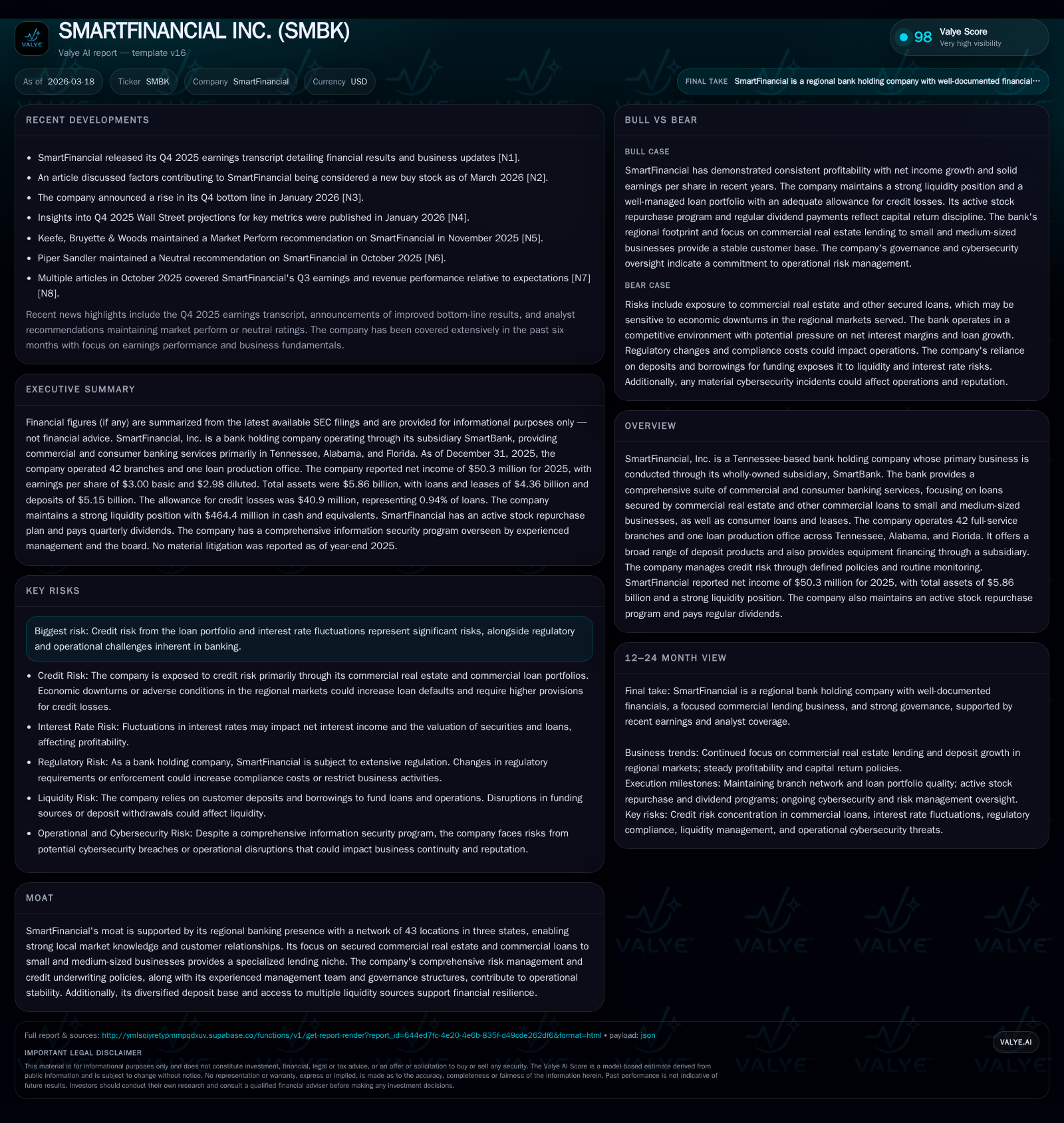

SmartFinancial Inc. Charts Regional Banking Growth with Focused Loan Portfolio

SmartFinancial’s regional scale combined with its specialized commercial lending and disciplined capital management underpin its steady profitability and risk posture.

SmartFinancial, primarily operating through its subsidiary SmartBank, maintains a strong regional presence across Tennessee, Alabama, and Florida with 43 locations. Its loan portfolio is concentrated in secured commercial real estate and small-to-medium enterprise commercial lending, which drives both growth and credit risk governance. The company reported a notable 26.4% net income increase in 2024 reflecting effective capital deployment and operational efficiency, supported by prudent liquidity management and regulatory capital buffers. Despite favorable financial metrics and an active buyback program, cautious attention to credit provisioning and interest rate exposure remains warranted as key factors shaping future performance.

Regional Footprint and Niche Lending: Foundations of Growth

SmartFinancial, Inc., through its wholly owned subsidiary SmartBank, operates a network comprising 42 full-service branch offices plus one dedicated loan production office spread across Tennessee, Alabama, and Florida — totaling 43 locations at the end of 2025 [S1]. This footprint enables the bank to capitalize on deep local market knowledge crucial for effective client engagement and competitive niche positioning.

The loan portfolio is distinctly specialized with a heavy concentration in secured commercial real estate loans alongside commercial loans geared toward small- and medium-sized enterprises (SMEs) [N1],[S1]. This focus aligns with demonstrated demand in regional markets for tailored financing solutions that address complex collateral structures and SME growth financing needs.

This lending specialization supports SmartFinancial's moat by fostering close customer relationships in these geographies while leveraging expertise in underwriting nuanced commercial credits—a strategic advantage amid increasingly competitive regional banking markets.

Historic Financial Performance: Income, Cash Flow, and Efficiency Trends

Examining recent financial results reveals sustained growth momentum coupled with disciplined capital investment:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 62 | 2 | ||

| 2024 | 36 | 53 | 6 | +26.4% |

| 2023 | 29 | 40 | 6 | -33.5% |

| 2022 | 43 | 57 | 12 | +23.7% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 5 | 3 | 59 |

| 2024 | 5 | 3 | 46 |

| 2023 | 5 | 1 | 33 |

| 2022 | 5 | 1 | 44 |

Source: SEC companyfacts cache [F1].

Note: Buybacks for FY2025 are not reported entirely but prior year showed $2.97 million spent [F1].

Net income surged by roughly four-fifths from FY2023 to FY2024 before the latest full year ended (FY2025) data is released; however consistent CFO expansion of more than a fifth between FY2023 to FY2025 indicates sound operating cash generation capability supportive of liquidity needs [F1]. Meanwhile, capital expenditures became significantly leaner in FY2025 after reductions over previous years — a sign of efficiency improvements or completion of key investment cycles.

With total equity rising steadily alongside income gains over this period, calculated ROE hovers near a moderate ~6.5% as of end-2024—a reasonable return balancing risk profile typical for mid-sized regional banks actively managing credit exposures [F1].

Loan Portfolio Composition and Credit Risk Oversight

SmartFinancial’s loan book is carefully managed under comprehensive credit risk policies that emphasize strong underwriting standards befitting their commercial focus areas.

At December 31, 2025, the allowance for credit losses was maintained at $40.9 million representing approximately 0.94% of total loans—consistent with prior periods—reflecting measured provisioning aligned with expected credit loss models under CECL accounting standards adopted since early-2023 [S9],[S21],[S26]. The company increased provision expense to $6.7 million in the most recent year versus $5.1 million previously illustrating heightened vigilance amid evolving economic conditions.

Credit policy governance involves multiple checks including segmentation-based underwriting criteria elevating approval authority for larger or complex credits plus routine monitoring supported by third-party reviews for significant accounts [S1],[S22]. These processes help mitigate concentrations inherent in secured real estate lending and SME exposures prone to localized economic shifts.

Risk committees such as the Risk Management Committee oversee overall credit risk frameworks while quarterly reporting to the board ensures strategic fit within risk appetite guidelines; the company also integrates detailed forecasting techniques incorporating national unemployment projections to inform loss estimations dynamically [S22],[S26],[S27].

Capital Structure, Liquidity Position, and Regulatory Compliance

Capital discipline remains central to SmartFinancial’s financial resilience.

Liquidity reserves reached $464 million in cash and equivalents at year-end December 31, 2025—a healthy buffer against operational needs—with no utilization drawn from access lines including a $402 million Federal Reserve discount window facility nor a fully available $35 million revolving line of credit maturing in mid-2027 [S4],[S5],[S7],[S16]. Such ready availability of low-cost sources highlights proactive liquidity risk management.

The company’s capital ratios surpass regulatory minimums comfortably — achieving “well-capitalized” status recognized by federal regulators as of December 31, 2025 [S18],[S28]. Among notable moves was issuance of $100 million subordinated debt during Q3-2025 which enhanced Tier-1 capital leverage while partially offset by retirement of older notes later that year—illustrating an active but prudent approach to optimizing funding structure without excessive leverage buildup or market dependence [S7],[S20].

Shareholder Returns: Dividends and Share Repurchase Evolution

SmartFinancial balances reinvestment needs with shareholder distributions thoughtfully.

Annual dividends paid consistently approximate $5.45 million across recent years reflecting a stable yield policy appropriate for their franchise size and earnings stability [F1],[S6]. Concurrently, the company operates an open-ended stock repurchase plan authorized up to $10 million with roughly $8.5 million expended as of late-2025 supporting share price stability and capital allocation flexibility.

Repurchases have been executed opportunistically without obligating management to specific buying schedules allowing responsive deployment based on market conditions—a hallmark of disciplined capital stewardship valuable amidst regional bank sector fluctuations [F1],[S6],[S11].

Projected Growth Drivers and Potential Headwinds

Looking forward, key growth drivers hinge on organic expansion across southeastern regional markets empowered by entrenched client deposits complemented by steady loan originations centered on SMEs benefiting from economic recovery cycles post-pandemic disruptions [N1],[N2]. The loan production office serves as a tactical vehicle enabling targeted deal flow capture without extensive physical branch investment.

Nonetheless, potential growth caps arise from macroeconomic uncertainties including sustained interest rate volatility impacting net interest margins along with heightened regulatory scrutiny which could elevate compliance costs or constrain aggressive asset growth strategies [N1],[S22]. Additionally, vigilant credit oversight remains imperative given concentrated exposure to commercial real estate segments sensitive to local economic swings.

Milestones to Monitor in 2026 and Beyond

Absent explicit forward guidance disclosed publicly at this time, monitoring forthcoming quarterly earnings releases will be essential to gauge trajectory on provisioning trends particularly if macroeconomic headwinds accentuate risk factors. Deposit growth metrics remain another bellwether—as maintaining or expanding stable low-cost deposit bases underpin balance sheet robustness. Additionally, observing continued progress against remaining share repurchase authorization offers insight into capital return priorities relative to growth or liquidity demands. Regulatory communications regarding capital adequacy updates or changes will further inform outlook adjustments necessary amid evolving banking sector policies.

This analysis relies exclusively on publicly available SEC filings up through March 16, 2026 ([F1],[S#]) alongside recent corporate earnings announcements ([N#]). All estimates apply strictly factual data without speculation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments