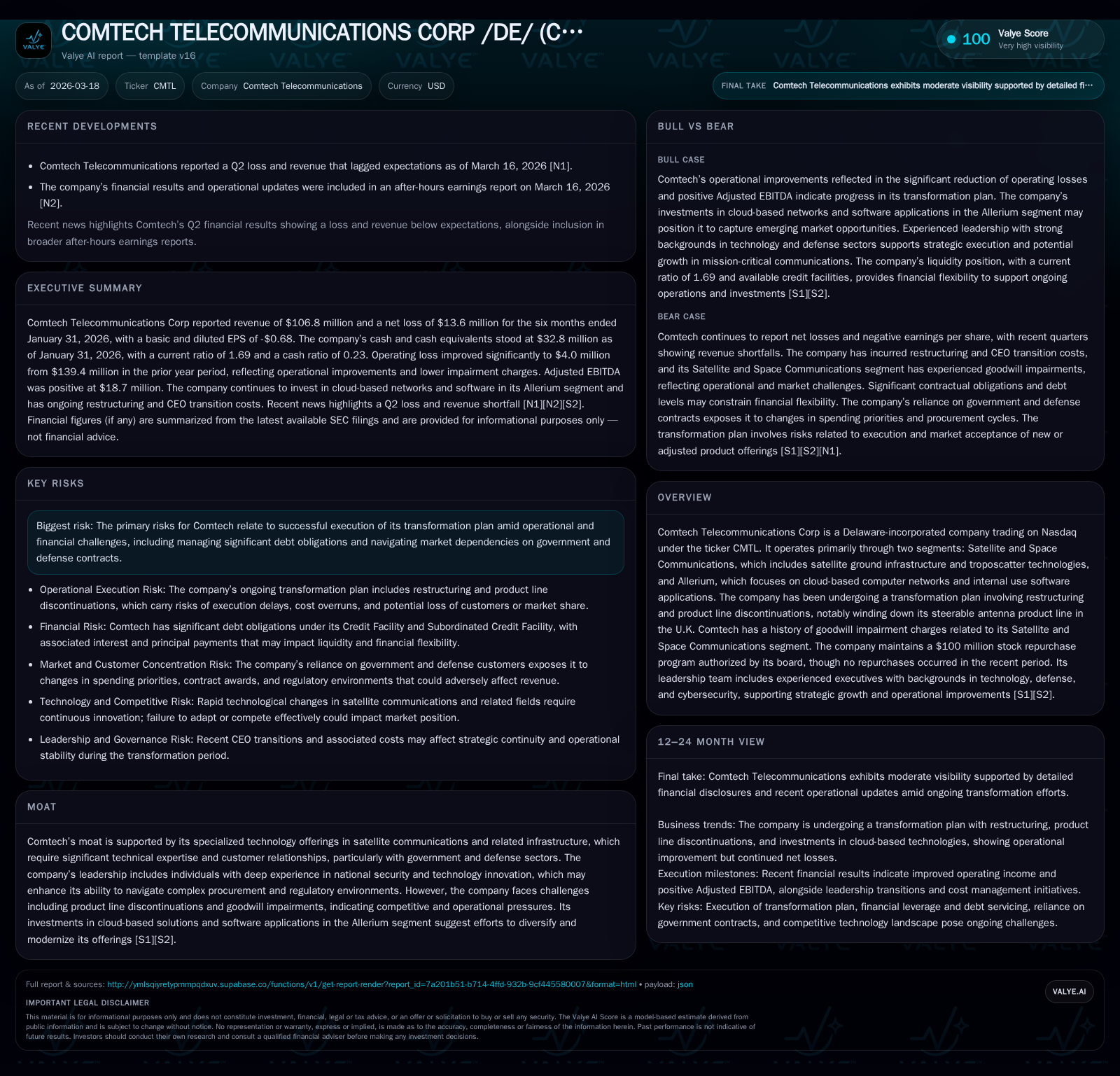

Comtech Telecommunications Navigates Deep Losses Amid Strategic Transformation and Capital Challenges

The company is addressing operational headwinds and legacy segment declines through restructuring and a pivot towards cloud-based solutions while managing significant debt and liquidity pressures.

Comtech Telecommunications Corp has experienced a multi-year decline in revenue and widening operating losses, driven by challenges in its Satellite and Space Communications segment including discontinued product lines and goodwill impairments. The company is executing a transformation plan focusing on operational streamlining and growth in its Allerium cloud services segment. Despite reductions in SG&A expenses and steady R&D investment, negative cash flow persists alongside substantial debt obligations. Liquidity is supported by $32.8 million in cash and revolving credit availability, but debt service commitments exceed $340 million. The board maintains a $100 million share repurchase authorization, though no repurchases occurred amid restructuring efforts and capital preservation.

Historical Performance Overview

Comtech Telecommunications Corp's financial performance over fiscal years 2022 through 2025 highlights persistent challenges within its core Satellite and Space Communications segment [F1]. Revenue declined from $549.9 million in FY2023 to $499.5 million in FY2025, a 7.6% decrease driven primarily by contraction of legacy product lines including the discontinuation of steerable antennas [S2][S22]. Operating losses expanded dramatically to -$139.1 million in FY2025 from -$14.7 million in FY2023 largely attributable to goodwill impairment charges of approximately $79.6 million recognized within the Satellite segment, restructuring expenses related to operational streamlining including severance costs, and non-cash amortization of intangible assets [F1][S21][S23]. Net losses similarly widened to -$155.3 million.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 500 | -155 | -8 | -139 | -7.6% | -55.3% |

| 2024 | 540 | -100 | -54 | -80 | -1.7% | -271.7% |

| 2023 | 550 | -27 | -4 | -15 | +13.1% | +18.6% |

| 2022 | 486 | -33 | 2 | -34 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -17 | -148.7 |

| 2024 | 0 | -68 | -32.6 |

| 2023 | 9 | -23 | -6.1 |

| 2022 | 11 | -18 | -7.1 |

Source: SEC companyfacts cache [F1].

Note: Dividends reflect actual payments; no recent buybacks have been executed.

Operating cash flows have fluctuated negatively due to working capital pressures and restructuring-related outflows but showed improvement from highly negative levels in FY2024 [F1][S10][S14]. Capital expenditures have decreased steadily as the company reduces investments tied to legacy infrastructure while selectively investing in cloud-based capabilities within the Allerium segment [S8][S13].

Transformation Plan and Segment Overview

Comtech's business is primarily organized into two segments: Satellite and Space Communications—which encompasses satellite ground infrastructure including troposcatter technologies—and Allerium, which delivers cloud-based computer networks and internal use software applications [S1][S2]. The Satellite segment faces headwinds from product obsolescence resulting in inventory write-downs exceeding $11 million related to discontinued products and goodwill impairments [S2][S26]. A key restructuring initiative includes winding down the steerable antenna product line in the UK initiated during fiscal 2024 [N1][S2].

In contrast, the Allerium segment represents growth initiatives focused on scalable software-driven solutions with consistent research and development spending around $5-6 million per half year period aimed at enhancing cloud services offerings [S21][S15]. Research efforts also persist within Satellite for next-generation broadband satellite technologies albeit at reduced levels post-antenna discontinuation [S15][S21].

The company’s customer base is specialized with tailored requirements often tied to government defense contracts, creating technological barriers but also necessitating agile adaptation amid evolving sector dynamics.

Recent Financial Results & Operational Highlights

For the six months ending January 31, 2026, Comtech reported consolidated net sales approximating $217 million based on quarterly disclosures [N1][S2]. GAAP operating loss narrowed relative to prior periods when excluding approximately $4 million of one-time restructuring charges compared to prior year periods significantly impacted by goodwill write-offs [S21][S23]. Selling expenses declined by about $27 million year-over-year before restructuring adjustments but represented a higher percentage of sales due to reduced revenues [S2]. Stock-based compensation expenses exhibited variability linked to leadership transitions.

Research and development expenses remained near flat year-over-year at roughly $8.2 million for the six-month period ending January 31, 2026—around 3.8% of sales—targeting critical technological advancements [S2][S21]. Capital expenditures totaled approximately $7-8 million during this interval directed primarily toward expanding Allerium's cloud infrastructure and facility improvements [S8][S11].

Liquidity and Capital Structure

As of January 31, 2026, Comtech held approximately $32.8 million in cash equivalents alongside roughly $19 million available under its revolving credit facility [F1][S7]. However, total contractual debt obligations—including principal, interest payments, plus make-whole amounts on subordinated loans—exceed $340 million with maturities extending through October 2030 [S7]. Effective interest costs are elevated due to accretion features on subordinated debt despite senior borrowings carrying cash interest rates near ~14% [S21][S23].

The board authorized a $100 million stock repurchase program in September 2020 but no shares were repurchased during recent periods as capital preservation remains paramount amid ongoing strategic execution [S12]. Dividend payments ceased after FY2023 consistent with liquidity management under credit covenants [F1][S14].

Growth Outlook and Risks

Comtech’s path forward relies on successfully transitioning away from hardware-centric satellite ground equipment toward software-driven cloud communication services within the Allerium segment while securing new contracts leveraging next-generation satellite broadband technologies supported by ongoing R&D investments [N1]. Emerging broadband satellite constellations could present growth opportunities if technology adapts effectively.

However, significant risks persist including heavy leverage burdens; timing uncertainty around contract awards amid geopolitical budget constraints; potential further asset impairments or inventory obsolescence; integration challenges within newer cloud offerings; and competitive pressure impacting margins [S1][N1]. Execution risk associated with the transformation plan is heightened by macroeconomic volatility influencing government procurement priorities.

Investors should closely monitor quarterly updates for signs of sustained profitability improvements excluding one-time items; operational cash flow generation sufficient for deleveraging; disciplined capital expenditures aligned with digital expansion strategies; prudent SG&A management without stifling innovation; and developments regarding government contract pipelines particularly for advanced satellite communication systems.

Conclusion

Comtech Telecommunications Corp confronts ongoing operational difficulties marked by declining revenues and deepening losses related primarily to legacy Satellite segment impairments while demonstrating early stabilization through restructuring coupled with strategic shifts toward diversified cloud communications via the Allerium segment.

Although improved operating efficiencies have tempered losses excluding non-recurring charges, negative free cash flows combined with substantial debt maturities impose liquidity constraints requiring vigilant execution of transformation initiatives supported by board-sanctioned capital preservation measures including suspension of share repurchases and dividends.

The company’s niche specialization within satellite communications alongside leadership rooted in defense markets may provide modest competitive advantages if it can execute its strategic pivot successfully without incurring additional significant asset impairments or weakened contract demand.

This analysis is provided solely for informational purposes without making any recommendation regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments