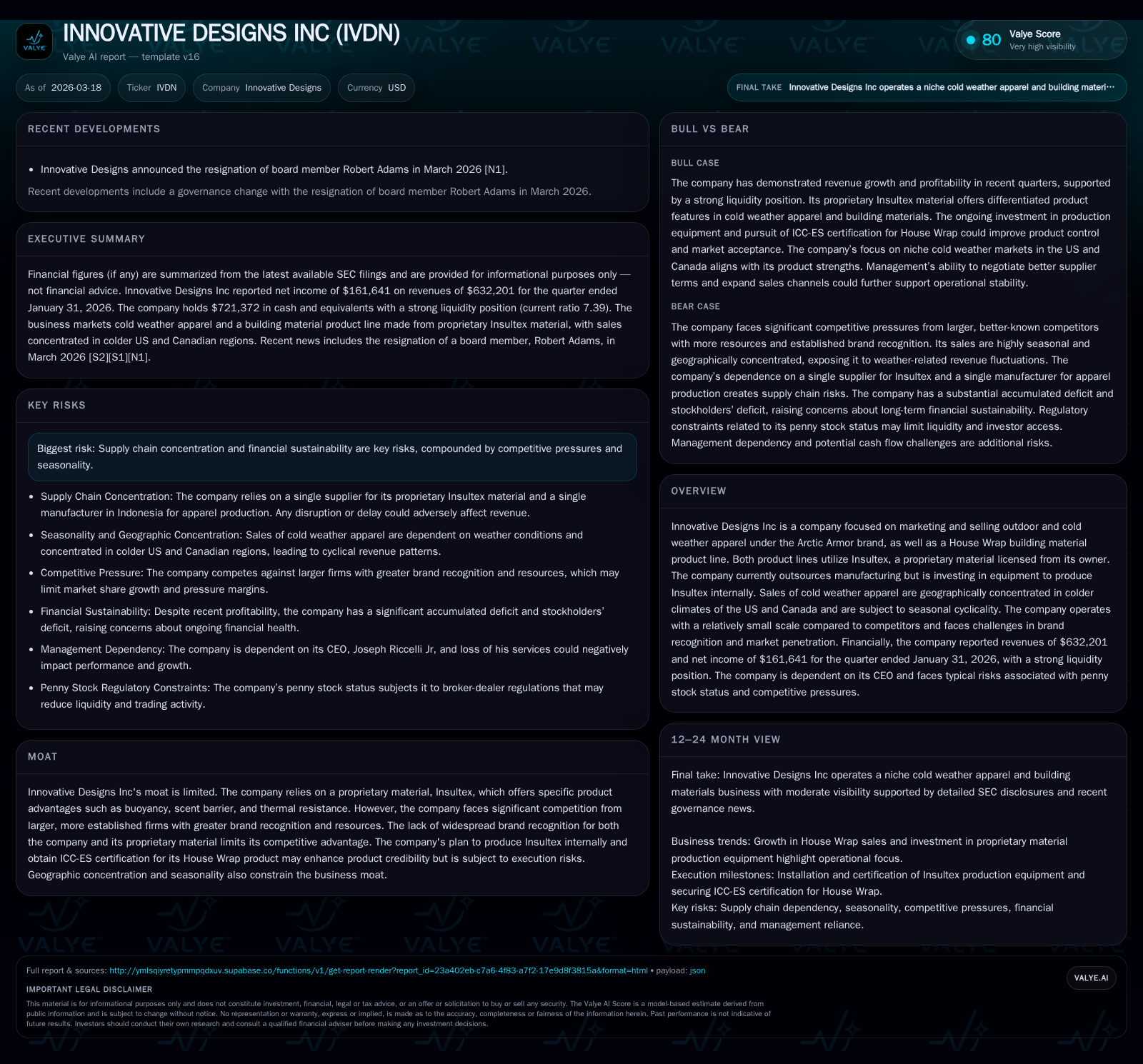

Innovative Designs Inc Doubles Revenue with Insultex Innovation and Internal Manufacturing Shift

A detailed analysis of Innovative Designs Inc’s financial turnaround driven by proprietary material advantage and operational transformation.

Innovative Designs Inc has reversed historical losses to achieve significant profitability, doubling revenues over three years largely due to growth in its House Wrap product line powered by proprietary Insultex material. The company is transitioning from outsourced manufacturing to internal Insultex production to enhance margin control and supply reliability, although execution risks persist. Seasonality and geographic concentration weigh on revenue consistency amid stiff competition from established large players. Strong liquidity and prudent capital allocation underpin the recent financial robustness, with future growth hinged on certification milestones and manufacturing scale-up.

From Operating Losses to Profitability: A Financial Turnaround Analysis

Innovative Designs Inc has exhibited a remarkable financial transition over the period FY2022 through FY2025. Revenue surged from $258,734 in FY2022 to nearly $2.77 million in FY2025 — an increase of approximately 100% year-over-year for the most recent fiscal year [F1]. This dramatic sales acceleration was accompanied by an inversion of operating results; the company moved from operating losses exceeding half a million dollars in FY2022 (-$554K) and FY2023 (-$284K) to a robust operating income of roughly $501K in FY2025, marking a 276% improvement year-over-year [F1]. Net income trends paralleled this swing, rising from net losses (-$225K in FY2022) to positive earnings of nearly $495K in FY2025 — a sixfold increase compared with the previous year’s modest $73K profit [F1]. Operating cash flows tell a consistent story: negative CFOs persisted through FY2024 but turned strongly positive at about $460K in FY2025 [F1], enabling the company to fund operations without reliance on debt.

This swift turnaround benefits both from scale effects as revenue doubled and tighter costs management. The company's liquidity position further strengthens this narrative with a current ratio exceeding 7x at January 31, 2026 ([F1] Current Assets: ~$1.67M vs Current Liabilities: ~$226K). Such ample short-term liquidity cushions the firm against temporary working capital cycles inherent in their seasonal product lines.

Historical Financial Performance Summary (FY2022-FY2025)

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | 494703 | 459847 | 500606 | +100.0% | +576.6% |

| 2024 | 1 | 73114 | -201668 | 133195 | +297.6% | +124.3% |

| 2023 | 0 | -301378 | -209489 | -284090 | +34.4% | -33.7% |

| 2022 | 0 | -225489 | -99685 | -554417 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 449181 | 24.0 |

| 2024 | -211226 | 5.1 |

| 2023 | -230082 | -27.2 |

| 2022 | -22.5 |

Source: SEC companyfacts cache [F1].

*Note: large percentage swings reflect low prior base ([F1]).

Insultex Material: Proprietary Advantage Amidst Branding Challenges

Innovative Designs’ core moat resides primarily in its licensed proprietary material Insultex utilized across both its outdoor apparel (Arctic Armor line) and House Wrap building products [S1]. Insultex provides distinct functional advantages including buoyancy — critical for safety aspects particularly in cold weather gear — plus scent barrier properties verified through rigorous permeation testing methods conducted by Texas Research Institute Austin. Specifically, gas stimulant exposure over eight hours showed minimal permeation indicative of strong odor containment—a key attribute for hunting apparel applications where scent control is paramount [S1]. Thermal resistance further positions Insultex as a legitimate alternative to conventional insulation options.

Yet despite these functional merits well-recognized within technical circles (e.g., standards-based permeation sampling every few minutes during tests), the company confronts significant hurdles around brand recognition both at consumer and trade levels. Market perceptions tend toward established insulation materials like down feathers with decades-deep consumer trust; thus Insultex faces uphill battles building broad market awareness and demand pull beyond niche users that prioritize its unique features [S1]. This challenge underscores a classic innovation adoption curve issue prevalent across specialty materials sectors where technical superiority does not always translate immediately into sales traction absent extensive marketing budgets.

Operational Shifts: Transitioning from Outsourcing to Internal Manufacturing

Historically reliant on outsourcing for apparels production incorporating Insultex material—principally via Indonesian manufacturers—Innovative Designs is actively investing to bring Insultex manufacturing capabilities internally by acquiring dedicated equipment (~$700K contract signed since mid-2015), intending self-production under company control [S9],[S25]. This strategic pivot aligns with typical manufacturing industry imperatives seeking margin improvement via backward integration alongside supply chain resilience enhancements.

Over the last several quarters ending January 31, 2026, capex grew modestly by about +11.6% YOY (~$10.7K vs $9.6K prior year), reflecting incremental outlays toward equipment installation and startup costs accompanying this shift [F1],[S13],[S15]. However significant additional investments are captured as deposits on equipment totaling approximately $653K outstanding as of mid-2025 filings highlighting capital intensity ahead [S25],[S9]. Installation timelines remain uncertain with dependencies spanning facility procurement to international specialist technicians' arrival—a recognized execution risk that could delay intended operational benefits.

Moreover, planned ICC Evaluation Services (ICC-ES) certification process for the House Wrap line requires this embedded quality control equipment be fully operational and independently verified before we see certification outcomes—a prerequisite for scaling large commercial sales given market expectations for validated R-value claims among building materials buyers [S9],[S25]. These regulatory compliance requirements represent both gatekeeping mechanisms enhancing product credibility but also time-consuming non-trivial hurdles introducing uncertainty around go-to-market timings.

Seasonal and Geographic Factors Shaping Revenue Cyclicality

Sales of Arctic Armor cold weather apparel naturally concentrate geographically within northern US states and Canada regions subject to severe winter climates. The company explicitly acknowledges that these regions constitute primary markets currently accounting for roughly 10% of total revenues mainly attributable to cold temperature conditions dictating wear demand cycles each fiscal year end (FY ended Oct ‘23 referenced as example) [S1],[S17]. Consequently quarterly results must be contextualized within cyclical demand spikes during winter months with troughs otherwise impacting revenue visibility.

House Wrap products are likewise exposed to seasonality linked not only to colder months but local construction activity rhythms influenced by regional weather cycles impacting contractor ordering behavior leading to quarter-to-quarter variance patterns [S17]. Such climatic dependency reinforces working capital management complexities forcing inventory buffers calibrated against forecast timing uncertainties common across building material industries.

Competitive Landscape: Legacy Market Giants versus Innovative Designs’ Scale

IVDN operates against formidable incumbents in both product categories complicating market penetration efforts. House Wrap competition is dominated by multinational corporations like Dupont and Kimberly Clark boasting entrenched brand equity widespread distribution channels plus R&D firepower far surpassing small cap competitors like Innovative Designs [S1]. Meanwhile Arctic Armor competes against specialized players such as Ice Clam Corporation et al., which though niche-focused maintain stronger brand visibility among outdoors enthusiasts.

The firm attempts differentiation on product-specific features — lightweight waterproof windproof fabrics combined with sub-zero protection layered by proprietary Insultex offering buoyancy/scent barrier pros — rather than pure price undercutting tactics. However lacking scale restricts marketing reach limiting consumer awareness buildup contributing to persistent challenges scaling beyond existing base customers constrained regionally primarily due to familiarity effects prevailing within outdoor apparel market segments characterized by brand loyalty.[S1]

Capital Allocation Focus: Liquidity, Debt Management, and Returns

Innovative Designs demonstrates prudent capital stewardship evident from its robust liquidity position measured as current assets totaling approximately $1.67 million against current liabilities near $226 thousand yielding an impressive current ratio just over 7x at the close of January ’26 quarter-end—providing comfort towards short-term obligations funding operations smoothly amidst cyclicality challenges [F1],[S3],[S14],[S27].

Long-term debt is minimal with notes payable balances around $10K all current as of reporting dates negating material interest burdens or refinancing risks; shareholder loans similarly kept constrained underscoring conservative leverage posture maintained historically across periods analyzed [F1],[S14].

Financial return metrics underscore operational efficiency gains post-turnaround; approximate ROE calculated at ~24%, derived from net income versus equity base ($495K net income / $2.06 million equity) signifying effective utilization of shareholders’ capital during profitability escalations [F1].

Cash flows reinforce fundamental stability with free cash flow approximated at $449K (CFO minus Capex), evidencing capacity generation supporting organic expansion absent reliance on dilutive external financing so far. Notably there are no declared dividends or share repurchase programs consistent with reinvestment priority phase typical for smaller innovators asserting scale growth before shareholder distributions become viable considerations [F1],[S10].

Future Growth Catalysts and Execution Risks in Product Development

Looking ahead growth trajectories hinge on near-term milestones as disclosed including achieving ICC-ES certification for House Wrap products expected to unlock broader commercial purchase orders vital for scaling revenue streams substantially beyond existing levels secured predominantly through smaller contracts or direct sales channels [N1],[S9],[S25].

Concurrent internal manufacturing ramp-up entails complex project management demands balancing capital expenditure commitments (~$700K machine acquisition plus ancillary costs) alongside regulatory approvals tied closely to machinery installation timing availability of qualified technical personnel imported internationally presents notable execution risks threatening potential schedule slippages or cost overruns should any component falter unexpectedly.

Additionally geographic expansion efforts beyond traditional colder climate strongholds would require commensurate marketing investments overcoming entrenched competitor brand dominance compounded by consumer inertia favoring established insulation materials emphasizing a critical need for intensified branding initiatives potentially stretching limited marketing budgets underscoring strategic resource allocation tradeoffs ahead.

Investor Outlook: Key Metrics and Milestones to Monitor

Investors tracking Innovative Designs should closely monitor quarterly revenue retention outside peak cold-weather months which serve as bellwethers regarding diversification success countering seasonality headwinds noted historically across apparel segment performance patterns [N1],[F1],[S2]. Equally critical will be progress updates on realizing full operational capacity internally within Insultex production machinery monitoring adherence against planned installation timelines plus completion of ICC-ES certification process which will materially impact credibility and reorder cadence especially for House Wrap customers seeking code-compliant solutions.

Maintaining strong liquidity ratios while avoiding any meaningful upticks in short-term payables or credit dependence will also signal capable working capital management preserving solvency during cyclical downturns characterizing sector dynamics enhanced awareness relating supplier concentration risks flagged within filings reinforce caution downstream should supply disruption events occur complicating raw material timely availability impacting finished product deliveries adversely acting as warning flags requiring proactive mitigation strategies going forward.[N1],[S2],[F1]

This analysis integrates publicly filed SEC financial statements dated up through March 18, 2026 ([F1], [S#]) alongside relevant public news disclosures ([N#]) reflecting facts known as of report date without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments