ORRSTOWN FINANCIAL SERVICES’s Sharp Net Income Surge Reflects Operational Expansion

After a volatile prior two years, ORRSTOWN FINANCIAL SERVICES INC reported a dramatic rebound in net income and cash flow for 2025, fueled by operational growth and rising equity.

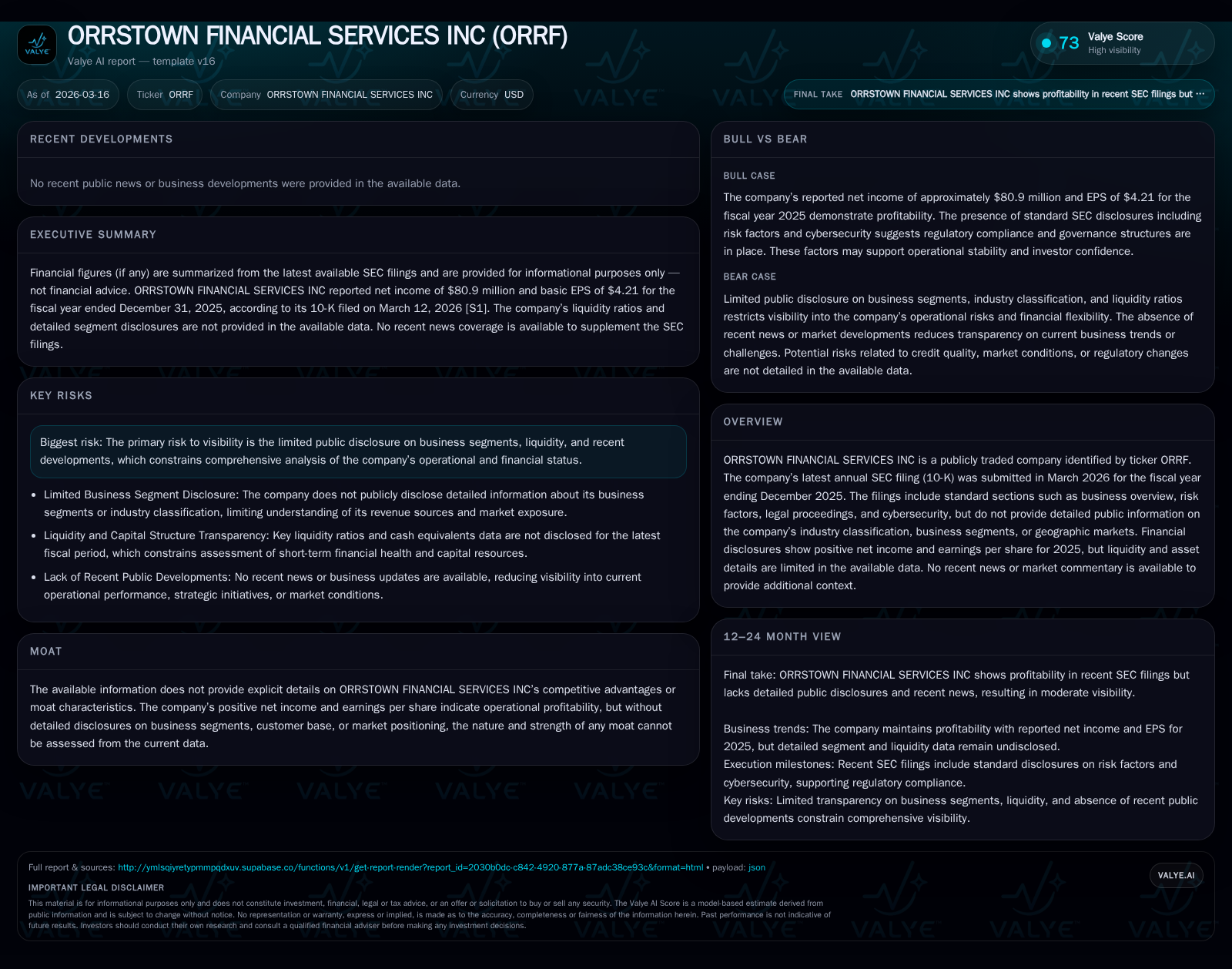

Orrstown Financial Services Inc (ticker ORRF) experienced a significant increase in profitability during the fiscal year 2025, with net income climbing to $80.9 million from $22.1 million in 2024. This triple-digit growth was accompanied by a doubling of operating cash flow and substantial equity expansion. While public disclosures lack industry and segment details, the company’s capital allocation shows rising dividends and minimal buyback activity in 2025. Key financial metrics like ROE improved to approximately 13.7%, indicating more efficient use of equity capital. The limited granularity on business composition and liquidity creates challenges for comprehensive analysis but underscores operational momentum going into 2026.

Overview

ORRSTOWN FINANCIAL SERVICES INC (ticker: ORRF) presented robust financial results for the fiscal year ending December 31, 2025, as documented in their latest March 2026 SEC annual filing (10-K) [S1][F1]. Despite the absence of specific industry classification data and segment breakdowns in official disclosures, the company demonstrated a pronounced rebound following more modest prior years.

Historical Performance

The most striking aspect of Orrstown's recent financials is the leap in reported profitability. Net income jumped from $22.1 million in FY2024 to $80.9 million in FY2025 — an increase of approximately 267% [F1]. This leap effectively reverses a somewhat uneven trajectory over the past four years wherein net income fluctuated between roughly $22 million and $35 million before accelerating sharply last year.

Operating cash flow (CFO), a key liquidity indicator representing cash generated from core operations, grew similarly—from about $35.0 million in FY2024 to $74.7 million FY2025 (+113.8%), nearly doubling within one year [F1]. This suggests that profitability gains translated well into realized cash inflows.

The company also invested more heavily back into its asset base as capital expenditures surged to $4.2 million in FY2025 from just $1.6 million the prior year (+167.7%) [F1]. This likely signals efforts to expand infrastructure or technology platforms driving future growth.

Equity capital expanded significantly with shareholders’ equity rising from approximately $517 million at end-2024 to $592 million at end-2025, evidencing retained earnings accumulation and/or capital injections over time [F1]. This swelling equity base pairs with increasing profitability to enhance overall firm value.

Meanwhile, dividends paid to shareholders also increased meaningfully—$20.6 million in FY2025 versus $13.2 million in FY2024—highlighting management’s focus on returning stable cash flows amid growth [F1]. Share repurchases were negligible during FY2025 relative to prior years when buybacks were more material, pointing potentially toward prioritizing dividends or other uses of capital.

Summary Table: Orrstown Financial Services Inc Annual Financials

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 81 | 75 | 4 | +266.7% |

| 2024 | 22 | 35 | 2 | -38.2% |

| 2023 | 36 | 44 | 2 | +61.8% |

| 2022 | 22 | 36 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 21 | 0 | 70 |

| 2024 | 13 | 0 | 33 |

| 2023 | 8 | 3 | 41 |

| 2022 | 8 | 14 | 35 |

Source: SEC companyfacts cache [F1].

Net income shows sharp acceleration in latest year; operating cash flows track earnings gains; capex rising alongside equity expansion; dividends growing steadily while buybacks dropped.

Drivers Behind Past Growth

Due to limited qualitative disclosures on business segments or customer profiles [S1], it is not possible to identify specific revenue lines or geographic markets behind the improvement definitively.

However, the considerable rise in net income paired with near doubling of operating cash flow implies either successful credit risk management allowing higher interest margins or notable growth in lending volumes/fee income typically expected for community banks or regional financial services firms.

An uptick in capital expenditures may point toward modernization investments such as expanding digital offerings or branch refurbishment aimed at capturing new clients or enhancing operational efficiency—a common strategic focus among midsize financial institutions navigating technological shifts.

The sizable boost in equity capital indicates solid retained earnings growth primarily from strengthening profits but may also reflect minor capital raises contributing additional firepower for lending or balance sheet expansion.

Dividend increases reinforce confidence from management and board regarding sustainable free cash flow generation amidst this growth phase.

Future Growth Prospects

Although explicit guidance was not disclosed within filings or press releases [S3][N0], areas likely relevant for Orrstown’s future trajectory include:

- Continuation of prudent lending expansion benefiting from improved macroeconomic conditions supporting borrower repayments.

- Further investment into digital banking platforms facilitating customer acquisition while controlling operating costs.

- Potential cautious share repurchase resumption balancing dividend policy as excess capital accumulates beyond regulatory minimums.

- Close monitoring of credit quality metrics given some portfolio parts may include real estate segments exposed to tighter underwriting standards post-pandemic.

Absent articulated strategic plans or milestone targets publicly available beyond standard risk disclosures [S4], watching quarterly earnings updates and loan portfolio credit performance will be critical indicators for assessing underlying momentum.

Capital Returns and Efficiency Metrics

Return on equity (ROE), approximated by dividing net income by average equity, stood near an estimated healthy level of roughly 13.7% for FY2025 based on available data points—a meaningful rise compared with earlier periods marked by sub-10% levels implied historically [F1]. Such improvement signals better leverage and earnings utilization amid asset base growth.

Free cash flow (operating cash flow minus capex) was strong at nearly $70.5 million in FY2025, underpinning ongoing dividend distributions totaling over $20 million while leaving room for balance sheet strengthening or opportunistic investments [F1].

Minimal stock buybacks indicate current management preference toward steady dividend payouts rather than aggressive share repurchase programs—potentially reflecting measured capital deployment consistent with regulatory prudence common across regional banking peers.

Risks and Disclosure Gaps

The principal challenge for investors analyzing Orrstown lies in the sparse transparency related to business segments, market demographics, loan portfolio composition by risk category, and liquidity nuances beyond broad aggregated numbers noted repeatedly throughout quarterly reports focused largely on capital structure captions rather than operational granularity [S5–S29].

Moreover, no recent news coverage offsets this opacity limiting timely assessment of possible strategic shifts or macroeconomic headwinds potentially impacting forward results.

Legal proceedings described are routine without significant litigation or regulatory interventions changing evaluation materially as per filings [S4].

Conclusion and Watch Points

Orrstown Financial Services has demonstrated impressive bottom-line recovery through strong net income gains coupled with expanding capital base and disciplined cash flow management entering early calendar year of reporting.

Going forward, clarity on operating segments, loan book quality trends especially within commercial real estate exposure common among community banks, plus management commentary around technology investments will be pivotal signals highlighting sustainability of recent success.

Dividend policies alongside potential resumption of share repurchases warrant continued scrutiny tied directly to evolving earnings quality and regulatory environment impacts affecting mid-tier financial institutions broadly.

Monitoring subsequent quarterly filings will be essential given absence of explicit company projections or detailed public guidance.

Disclaimer: This report is based solely on publicly available information including SEC filings and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments