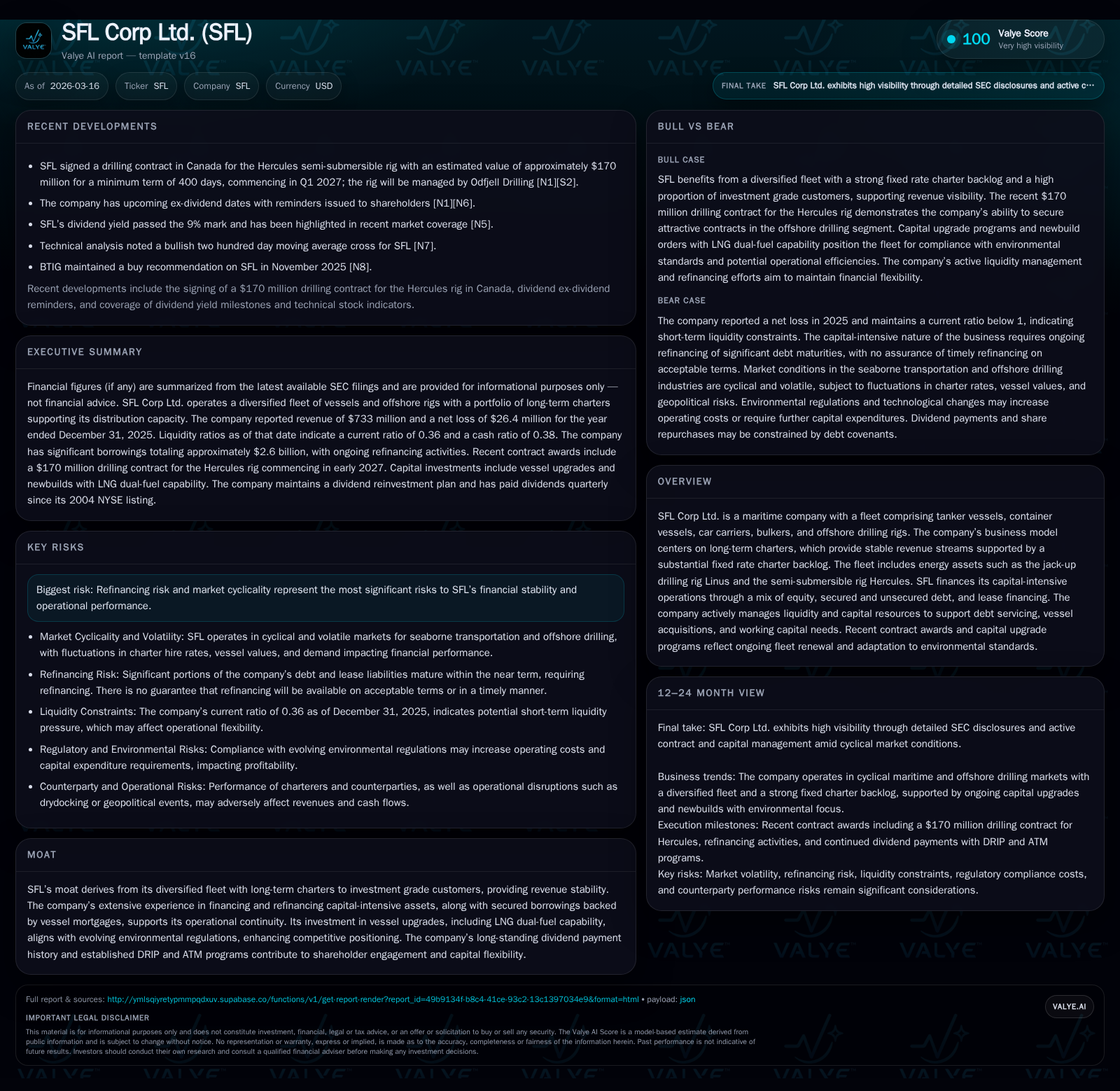

SFL Corp Ltd. Reflects Maritime Market Volatility with Strategic Contract Wins and Capital Maneuvers

SFL maintains dividend continuity despite a notable earnings decline, driven by a diversified charter portfolio and proactive fleet upgrades.

SFL Corp Ltd.'s revenue and operating income declined significantly in 2025 compared to prior years, reflecting ongoing maritime market volatility. The company counters cyclical revenue pressure with long-term contracts like the $170 million Hercules rig deal and executes environmental fleet upgrades for regulatory compliance. While refinancing risks persist due to large debt maturities, SFL’s strong liquidity management and capital allocation policies, including consistent quarterly dividends backed by operating cash flow, underpin its operational resilience. Upcoming rig mobilizations and shipbuilding commitments suggest potential for revenue recovery in coming years.

Historic Growth and Income Fluctuations: Analyzing FY2023–2025 Performance

SFL Corp Ltd.’s financial trajectory from fiscal years 2023 through 2025 highlights the pronounced cyclicality inherent in maritime asset finance driven by fluctuating charter rates and vessel utilization trends. Revenue peaked at approximately $904 million in FY2024 before contracting sharply by 18.9% to roughly $733 million in FY2025 [F1]. Correspondingly, operating income experienced a precipitous decrease exceeding 55%, plummeting from $307 million to about $137 million over the same interval [F1]. This steep decline largely stems from softer spot market conditions, despite the company’s focus on long-term fixed-rate charters that temper exposure.

Net income also registered a dramatic reversal — shifting from profits of over $130 million in FY2024 to a loss nearing $26 million last year [F1]. The deterioration reflects both reduced top-line performance and elevated financing costs associated with its substantial indebtedness. Operating cash flow followed suit, slipping nearly 28% year-over-year to approximately $267 million in FY2025 from prior highs above $369 million [F1]. This contraction places heightened emphasis on maintaining robust liquidity to underwrite capital expenditures and service debt obligations.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 733 | -26 | 267 | 137 | -18.9% | -120.2% |

| 2024 | 904 | 131 | 370 | 307 | +20.2% | +55.7% |

| 2023 | 752 | 84 | 343 | 240 | +12.2% | -58.6% |

| 2022 | 670 | 203 | 355 | 275 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 125 | 10 | -2.8 |

| 2024 | 138 | 10 | 11.6 |

| 2023 | 123 | 10 | 8.1 |

| 2022 | 112 | 18.6 |

Source: SEC companyfacts cache [F1].

This table summarizes key annual financial metrics indicating cyclical volumetric and profitability shifts typical for charter-based maritime operators [F1].

Contract Portfolio Strength: The $170 Million Hercules Rig Deal and Charter Backlog

The announcement of the $170 million drilling contract with an investment-grade multinational client for the semi-submersible rig Hercules marks a critical anchor within SFL's diversified portfolio, supporting stable cash flows against volatile spot markets [N2][S2]. Scheduled to commence early Q1 2027 off East Coast Canada — a known harsh environment where the rig has historic operational familiarity — this contract strengthens the segment's medium-term outlook.

This award complements SFL’s broader strategy of securing long-term time charters across tanker vessels, container ships, car carriers, bulkers, and offshore rigs — where a substantial backlog of fixed-rate contracts exists [S2]. Notably, Odfjell Drilling will manage Hercules during this deployment enhancing operational oversight leveraging sector-specific expertise.

Such high-quality counterparty agreements reduce revenue volatility from spot-market swings, underscoring the firm’s moat which blends fleet diversification with charter tenure stability.

Environmental Upgrades and Fleet Renewal: Meeting Regulatory Demands

Capital allocation towards comprehensive environmental modifications embodies a critical competitive lever amid tightening IMO emissions standards and forthcoming global regulations targeting sulfur oxide outputs [S1]. In particular, multiple vessels spanning container ships, tankers, and car carriers have undergone LNG dual-fuel conversions — enabling use of low-sulfur fuels or natural gas alternatives essential for compliance.

Offshore assets such as Hercules and Linus also receive targeted retrofits improving operational efficiency while adhering to environmental mandates [S1]. These upgrades entail sizable capital outlays ($70.5 million invested in these efforts during FY2025), reflective of industry-wide pressures faced by operator-financiers managing aging fleets amid regulatory transitions.

In maritime finance vernacular, these enhancements preserve vessel utility against declining charter-free values attributable to non-compliance risk premiums while positioning the assets favorably for future contracts requiring greener technology adaptation.

Liquidity Profile and Refinancing Strategy in a Capital-Intensive Industry

SFL’s liquidity posture as of December 31, 2025 reveals cash reserves totaling about $150.8 million complemented by revolving credit facilities secured against most assets [F1][S1][S4][S6][S7]. Nearly all vessels and rigs serve as collateral securing borrowings — conveyed through first priority mortgages on asset-owning subsidiaries — exemplifying classical asset-backed lending principles prevalent among maritime financiers.

Recent refinancing activity includes full repayment of a $150 million senior secured term loan on the jack-up drilling rig Linus followed immediately by drawing down a new three-year revolving credit line secured against the same asset (Feb-March 2026)[S1]. This transaction illustrates strategic liability management aiming at maturity smoothing amid sizeable refinancing needs.

Overall borrowings stood near $2.6 billion at year-end with about half concentrated within short-term maturities slated within twelve months [F1][S5][S16]. While management exhibits confidence rooted in an extensive history of timely refinancings bolstered by charter cash flow coverage ratios above covenant thresholds, prevailing macroeconomic credit conditions inject refinancing risk uncertainty [S1][N1].

Interest rate swaps reducing floating rate exposure over roughly $800 million of debt blend prudent treasury policy that balances cost containment alongside mitigating interest rate volatility [S14][S16].

Capital Allocation: Dividends, Buybacks, and Investor Return Policies

Despite net losses incurred in FY2025, SFL sustained its long-standing tradition of quarterly dividends — distributing approximately $125 million during the year via payments including quarterly dividends of $0.20 per share — underscoring commitment to shareholder yield continuity foundational since its NYSE listing inception in 2004 [F1][N3][S13].

Dividend sustainability draws upon solid operating cash flow generation ($267 million) combined with balance sheet robustness ($961 million equity base)[F1]. The company complements dividend policies through established DRIP mechanisms enabling shareholders optional reinvestment enhancing shareholder base depth [S13].

Modest repurchase activity (~$10 million executed during FY2025) reflects calibrated capital redeployment priorities emphasizing liquidity stewardship amidst earnings variability [F1][S13].

The ATM program provides further flexibility allowing issuance up to $100 million new shares if market conditions warrant incremental equity supplementation without dilutive surprises.

Financial Risks: Market Cyclicality, Refinancing Uncertainties, and Credit Costs

By nature, SFL is exposed to pronounced cyclicality inherent within shipping sectors where spot freight rates oscillate sharply contrary to often fixed charter revenues [N1][S1]. This dichotomy manifests materially through revenue declines alongside compressing profitability as demonstrated recently.

Refinancing risk is acutely monitored given significant bond maturities ($150 million sustainability-linked unsecured bond due mid-2026 alone), alongside numerous term loans approaching maturity between now and early next decade [S4][S5][S16]. The borrowing terms differ markedly between secured lines backed by vessel mortgages versus unsecured bonds priced at higher nominal yields reflecting credit risk premiums.

Management’s track record mitigates some concerns; however macroeconomic tightening combined with shipping sector uncertainty could pressure financing costs or delay renewals impacting debt serviceability constraints leading possibly to covenant breaches triggering acceleration risks.[S7][S8]

Cost differential between secured versus unsecured debt illustrates nuanced capital structure balancing intended to optimize liquidity while protecting asset retention rights under adverse scenarios[S7][S8].

Key Milestones Ahead: Upcoming Contract Launches and Fleet Deployment

Looking forward, notable catalysts include mobilization of the Hercules rig scheduled for early calendar 2027 providing tangible upside potential from substantial drilling revenues related to harsh environment operations off Canadian coasts[N2]. The rig's previous experience in similar waters reduces commissioning lead times enhancing commercial attractiveness for extended future engagements.

Parallelly five shipbuilding contracts valued at over $800 million predominantly target delivery of dual-fuel capable large containerships by end-2028 reaffirming SFL’s commitment toward fleet modernization aligned with evolving emission compliance requirements[S18].

These initiatives collectively offer pivotal inflection points likely to bolster revenue uplift prospects post-2026 as environmental mandates increasingly dictate charterer vessel selection criteria.

Investor Signals: Dividend Sustainability Amid Earnings Pressure

Investor communications reinforce confidence through maintained dividend distributions although reported net losses might superficially raise concerns[N3][F1]. However, positive operating cash flow coverage provides substantive underpinning evidencing capacity to service dividends independently of accounting profits.

The attached DRIP program further encourages shareholder reinvestment fostering steady ownership structures common among maritime finance investors favoring reliable yield over growth narratives[S13].

Maintaining dividend levels amidst earnings headwinds typifies yield-oriented business models where stable contract backlogs mitigate underlying volatility ensuring resilient distribution policies overall.

Disclaimer: This analysis relies exclusively on disclosed financial statements and official company releases as of March 16, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments