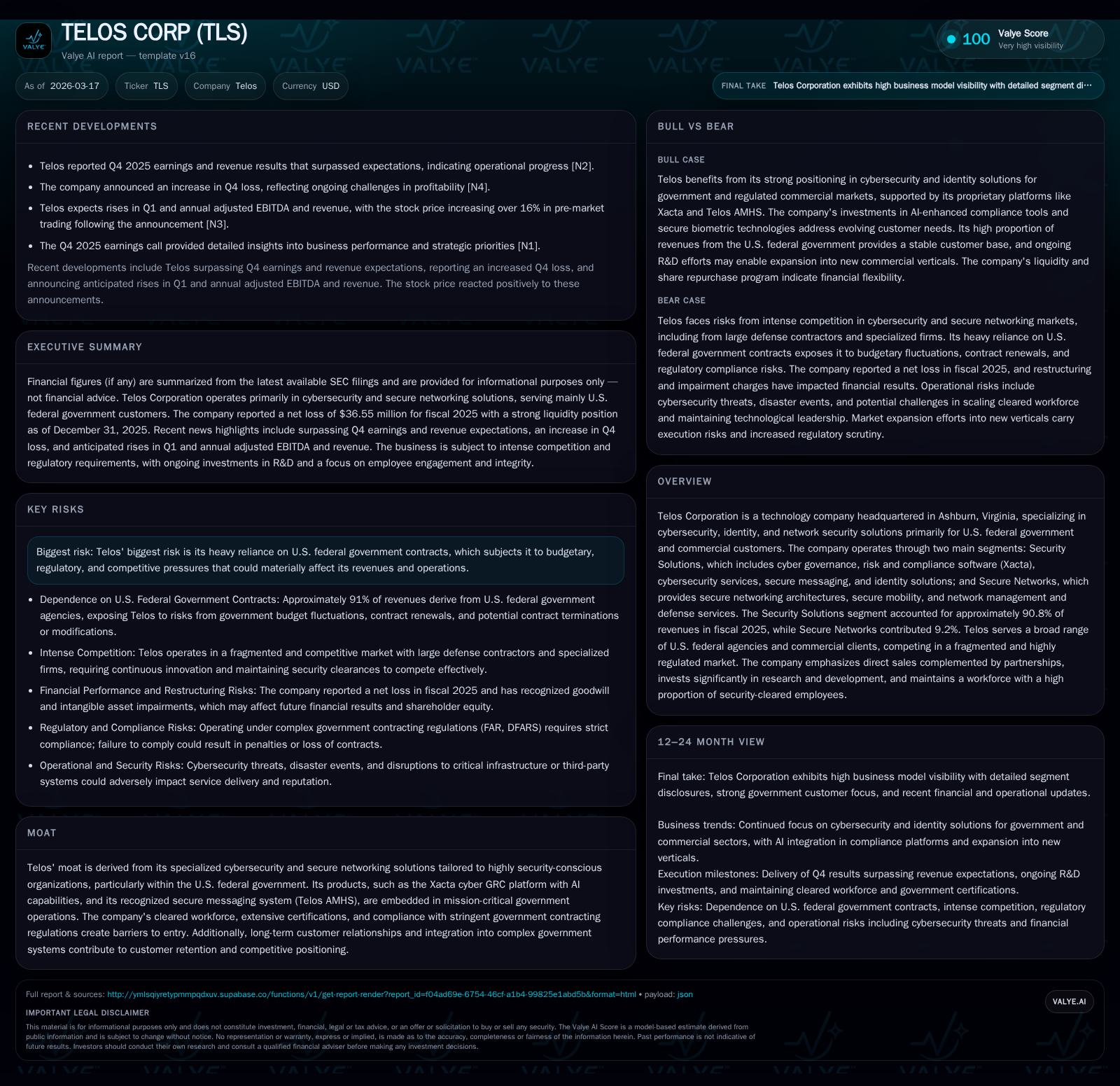

Telos Corp's Revenue Growth Counterbalanced by Rising Operating Losses and Government Contract Risks

Telos Corporation continues revenue expansion driven by cybersecurity solutions but faces mounting operating losses and dependence on U.S. federal contracts.

Telos Corporation, a provider of cybersecurity and secure networking solutions predominantly to U.S. federal agencies, has demonstrated significant revenue growth in recent years, particularly with its Security Solutions segment comprising over 90% of revenues in 2025. Despite this growth, the company has incurred increasing operating losses influenced by investment in research and development, expanded sales efforts, and sector dynamics. Its financial health is supported by strong operational cash flow and a sizable cash reserve, enabling ongoing capital deployment including share repurchases. However, reliance on U.S. federal government contracts introduces uncertainty through budgetary and regulatory pressures. Future growth depends on customer contract renewals, new contract awards, and successful expansion into commercial verticals while managing risk exposure inherent in government contracting.

Company Overview

Telos Corporation is a technology firm headquartered in Ashburn, Virginia, specializing in cybersecurity and secure networking solutions primarily serving the U.S. federal government alongside commercial clients [S1][S16]. Its product suite includes cyber governance risk and compliance software (notably the Xacta platform), identity technologies, secure messaging (Telos AMHS), network management, and defense services [S4][S20].

The company operates two main segments: Security Solutions driving over 90% of revenues as of fiscal year 2025, and Secure Networks contributing the rest [S4][S20]. Telos emphasizes direct sales complemented by partnerships (e.g., AWS) to expand market reach [S16].

Past Growth and Historical Performance

Revenue trends from companyfacts show $35.3 million for fiscal year 2017 but no recent consolidated top-line numbers are provided within the current dataset beyond segment contributions [F1][S4]. However, the Security Solutions segment’s share grew from approximately 71% in 2024 to nearly 91% in 2025 reflecting shifting business mix or segment scaling [S4][S20].

Financial performance reveals escalating operating losses: $39.9 million loss in 2025 improved from prior wider losses ($55.9 million in 2024), yet still substantial relative to revenue scale [F1]. Net income follows a similar pattern with a net loss of $36.5 million recorded in fiscal 2025 [F1].

Despite losses at the net and operating levels, Telos generated strong operating cash flow ($30.2 million in FY25) reversing negative flows seen earlier (-$25.9 million FY24) [F1]. Capital expenditures remain low ($739k in FY25), resulting in positive free cash flow ($29.4 million) powering financial flexibility [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -37 | 30 | -40 | 1 | +30.4% |

| 2024 | -53 | -26 | -56 | 2 | -52.6% |

| 2023 | -34 | 2 | -40 | 1 | -142.4% |

| 2022 | -14 | 17 | -15 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 14 | 29 | -38.1 |

| 2024 | 0 | -28 | -41.3 |

| 2023 | 0 | 1 | -21.6 |

| 2022 | 11 | 15 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures for recent years not directly available; analysis reflects segment reporting and related disclosures.

Business Model Nuances

Telos services mainly U.S federal agencies such as the Department of War (DoW), intelligence community units, DHS, DOJ among others [S4][S19]. These customers require highly secure solutions conforming to rigorous compliance standards such as NIST frameworks, FedRAMP, CMMC – all embedded within Telos’s flagship Xacta platform which recently incorporated AI capabilities (Xacta.ai) aimed at automating compliance workflows [S20].

The firm also delivers specialized cyber lifecycle services including security assessments, penetration testing, digital forensics supporting continuous assurance on mission-critical networks [S20]. Secure Networks offers managed service portfolios such as network management/defense reducing total cost of ownership while enhancing availability/security for complex DoD and civilian networks [S4].

Sales approach predominantly focuses on direct accounts supplemented by selected partnerships such as with AWS leveraging marketplaces for broader access [S16]. Market competition is intense within fragmented cybersecurity ecosystems involving large defense contractors alongside niche solution providers [S5]. Contract awards are mostly competitive bids subject to periodic renewals; thus contract attrition risk remains an ongoing concern [S5][S26].

Growth Prospects and Constraints

Growth drivers stem from elevated demand for cyber GRC automation amid rising government emphasis on risk-based security posture management recognized in federal directives and compliance mandates [N1][N3][S20]. The AI-powered Xacta.ai platform positions Telos well to capitalize on efficiency gains sought by agencies facing limited resources.

Expansion into commercial verticals — banking, healthcare, manufacturing etc.— offers avenues outside federal dependency but incurs execution risk due to lesser domain familiarity and potential regulatory complexities [S9][S16]. Sales investments targeting senior decision makers underpin strategic intent to deepen presence.

Constraints primarily relate to heavy reliance on U.S federal budgets (~91% revenue dependency) exposing Telos to cyclical appropriations uncertainties that may delay or curtail contracts leading to volatility in revenue streams [S23][S26]. The company acknowledges attrition risks as contract renewals are not guaranteed; attrition could be affected by changing spending priorities or customer dissatisfaction impacting financial results [S14][S26].

Operational risks include potential cybersecurity threats against internal or client infrastructures which could damage reputation or result in liabilities despite sophisticated protective measures [S14][S15]. Regulatory scrutiny over government contracting practices—including audits—introduces compliance costs and potential penalties if deficiencies arise [S11][S12]. Dependence upon third-party technology licensing is another vulnerability that may disrupt operations if licenses are lost or technical failures occur without viable alternatives readily available [S22][S23].

Forecasts and Milestones

Explicit guidance beyond recent earnings calls shows expectations of revenue and adjusted EBITDA growth per Q4 FY25 release signals positive momentum but no detailed multi-year outlook was provided within our evidence set [N1][N3]. Analysts should monitor upcoming contract awards/renewals given their outsized impact on near-term financial performance as well as progress on commercialization efforts outside government sectors.

Returns and Capital Allocation

The company’s return metrics reflect current challenges: a negative approximate return on equity near -38% based on latest net income relative to equity base indicates ongoing unprofitability though improved versus prior periods[F1].

Strong operational cash flow generation ($30m+) contrasted with modest capex (~$0.7m) results in robust free cash flow facilitating discretionary capital deployment including $13.6m share repurchases executed during fiscal year ending December 2025 under an existing program with roughly half capacity remaining for future buys [F1][S25]. No dividends were indicated.

This active buyback approach suggests confidence from management in underlying business value despite operating challenges but also reduces available liquidity cushions that might otherwise be deployed toward growth investments or debt reduction.

Conclusion

Telos Corporation occupies a defensible niche providing cyber governance automation solutions deeply embedded within U.S federal government ecosystems benefitting from stringent clearance requirements that act as barriers to entry. Its recent revenue growth trajectory is overshadowed by significant operating losses driven by investment intensive strategies aimed at product innovation (AI-enabled platforms), workforce certification expansion, sales penetration efforts plus managing complex contracted project executions.

Liquidity remains healthy backed by improving cash flows enabling ongoing capital returns via share repurchases albeit accompanied by meaningful execution risks driven by concentrated customer bases dependent on volatile federal budgets coupled with evolving cybersecurity threat landscapes.

Future value creation will depend heavily on contract retention/expansion success with existing federal customers combined with measured commercial expansion into regulated industries where demand heterogeneity exists.[N1][N3][S23]

This analysis synthesizes regulatory filings and recent public disclosures without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments