HealthEquity Expands Market Share and Profitability Leveraging Integrated Tech Platform Despite Debt Constraints

HealthEquity solidified leadership in health savings accounts through technology-driven services, growing accounts and profit while managing regulatory and financial risks.

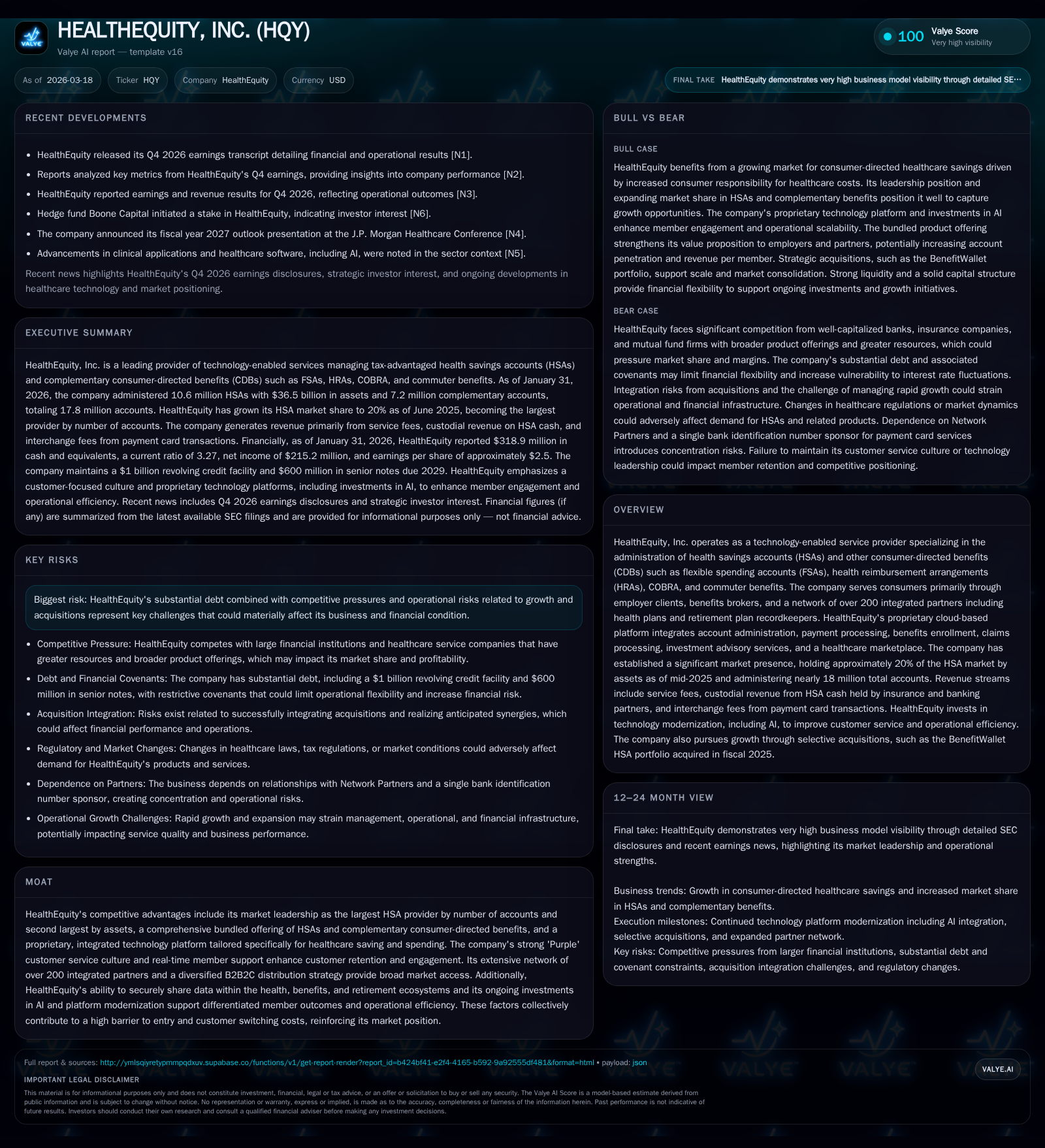

HealthEquity, Inc. operates a proprietary cloud-based platform administering health savings accounts (HSAs) and complementary consumer-directed benefits (CDBs), commanding about 20% of the HSA asset market as of mid-2025. The company’s growth has been propelled by its integrated technology, broad network partnerships exceeding 200 entities, and a distinctive customer service culture known as 'Purple'. Over recent years, HealthEquity matured from modest revenue to producing substantial operating income and cash flow, driven mainly by increased custodial assets and strategic acquisitions. However, elevated debt levels, regulatory complexities, and competitive pressures pose ongoing challenges to sustaining this trajectory.

Introduction

HealthEquity, Inc. () is a leading provider of technology-enabled services focused on administering Health Savings Accounts (HSAs) and related consumer-directed benefits (CDBs) such as Flexible Spending Accounts (FSAs), Health Reimbursement Arrangements (HRAs), COBRA administration, and commuter benefits [S5][S6][S8]. The company delivers these services via a proprietary cloud-based platform that integrates account administration, payment processing, claims handling, personalized investment advice through an SEC-registered advisory subsidiary, and an online healthcare marketplace designed to enhance member engagement. As of January 31, 2026, HealthEquity managed approximately 17.8 million total accounts with HSA assets totaling $36.5 billion [S8][F1].

Historical Performance

HealthEquity has demonstrated notable financial growth over recent years. Revenue was approximately $60.4 million in FY2026 [F1], reflecting steady expansion aligned with broader adoption of HSAs and complementary benefits. Operating income increased substantially from modest levels under $10 million in earlier years to $322.5 million in FY2026 [F1], driven by operational leverage inherent in recurring fee-based revenue streams tied to growing custodial assets.

Net income improved markedly to $215.2 million in FY2026 from prior losses and moderate profits [F1], underscoring enhanced profitability through scale and efficiency gains.

Operating cash flow rose consistently to around $457.1 million in FY2026 while capital expenditures remained modest at about $2.0 million annually [F1], enabling robust free cash flow generation capable of supporting debt servicing and reinvestment.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 215 | 457 | 322 | 2 | +122.5% |

| 2025 | 97 | 340 | 162 | 2 | +266.8% |

| 2024 | 26 | 243 | 118 | 2 | +200.8% |

| 2023 | -26 | 151 | 9 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 299 | 455 | 10.2 |

| 2025 | 121 | 338 | 4.6 |

| 2024 | 241 | 1.3 | |

| 2023 | 147 | -1.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data for fiscal years other than FY2018 and FY2026 are not directly disclosed; operating income and net income are available for recent years only [F1].

Share repurchases accelerated notably with nearly $299 million executed in FY2026 reflecting management's commitment to capital return amid no dividend payments currently [F1].

Business Model and Competitive Positioning

HealthEquity's core offering centers on HSAs—tax-advantaged savings accounts requiring enrollment in high-deductible health plans (HDHPs). These accounts provide "triple tax savings": tax-deductible contributions excluding employer contributions from gross income; tax-free earnings growth; and tax-free withdrawals for qualified medical expenses [S16]. Complementary CDB products such as FSAs and HRAs are bundled to offer employers a comprehensive benefits solution enhancing value proposition [S5][S14].

The company employs a business-to-business-to-consumer (B2B2C) distribution model leveraging employer Clients supported by benefits brokers/advisors alongside integration with over 200 Network Partners including health plans and retirement recordkeepers [S5][S8]. This broad channel strategy is key for scaling membership given reliance on employer benefit offerings.

Technology serves as a critical differentiator with proprietary cloud-based platforms delivering account management integrated with claims processing, payment card transactions, personalized investment advisory services via its SEC-registered subsidiary, access to a healthcare marketplace, plus increasing use of AI-powered tools such as Expedited Claims processing and HSAnswers decision support [S11][S12][S25]. This technology supports the company’s distinct 'Purple' customer service culture emphasizing real-time multi-channel support fostering high retention.

Market share has grown from about 4% of U.S.-held HSA assets in December 2010 to roughly one-fifth as of June 2025 according to Devenir research reports cited internally [S14]. The company also leads nationally by number of HSA accounts administered [S14]. Strategic acquisitions like the fiscal year ’25 purchase of BenefitWallet’s HSA portfolio added over half a million HSAs with nearly $2.7 billion assets for $425 million consideration funded partly via borrowings under revolving credit facilities [S14][S16].

Growth Prospects

Key growth drivers include:

- Market Expansion: Increasing consumer responsibility via HDHPs among privately insured working-age adults drives HSA eligibility growth [S8].

- Cross-Selling: Adoption of complementary CDB products increases wallet share per member while deepening integration within employer benefit ecosystems.

- Platform Innovation: Investments in AI-enabled claims automation (Expedited Claims), decision-support tools (HSAnswers), chip-stacked payment cards enabling multi-account access simultaneously, plus API integrations with partner systems bolster competitive moat against legacy or third-party platforms [S12][S25].

- Acquisitions: Selective purchases of smaller portfolios or non-core divestitures provide inorganic growth opportunities though integration risks exist [S11][S13][S27].

Challenges include potential regulatory changes diminishing tax advantages impacting volumes and revenues [S18][N9]; custodial risk related to insurance partners holding uninsured HSA cash under Enhanced Rates programs; intensifying competition especially from large financial services firms like Fidelity expanding into HSAs; plus operational complexity amid evolving privacy regulations increasing costs [S18][S20][N7][N11].

Financial Structure and Capital Allocation

The company’s capital structure features significant leverage comprising a senior secured revolving credit facility up to $1 billion maturing August 2029 with approximately $361.9 million drawn as of January 31, 2026 plus unsecured senior notes totaling $600 million due the same year at fixed interest rates [S7][S10][F1].

Liquidity remains robust with cash on hand near $318.9 million alongside covenant compliance requiring maintenance of specified leverage ratios under credit agreements ensuring operational flexibility within limits [S4][S7][S10]. Interest expense has risen reflecting higher debt levels but remains manageable given operating income growth.

Free cash flow approximated at roughly $455 million (operating cash flow less capex) supports balance sheet deleveraging potential or opportunistic share repurchases evidenced by nearly $300 million repurchased most recently while dividends remain suspended possibly due to covenant considerations or reinvestment focus [F1].

Competitive Landscape

HealthEquity faces competition from diverse players including retail investment firms like Fidelity Investments offering integrated retirement-HSA services; large healthcare entities such as UnitedHealth Group’s Optum; traditional banks; insurers; payroll providers; national CDB administrators; regional third-party administrators; plus indirect competition through ecosystem partners deploying white-label solutions [S17][S19].

The company's competitive strengths lie in its breadth—full spectrum consumer-directed benefits combined with proprietary technology enabling superior member engagement—and scale—being largest by account count—and its service philosophy fostering loyalty despite switching costs inherent in HSAs though competition intensifies with rivals investing heavily in AI and digital capabilities paralleling HealthEquity’s own innovation efforts.

Regulatory And Operational Risks

Complex federal/state regulations govern HSAs including Internal Revenue Code provisions granting tax-exempt status requiring strict compliance plus supervision from SEC authorities overseeing its investment advisory subsidiary functions [S20]. Evolving data privacy laws such as HIPAA amendments impose ongoing compliance costs.

Political uncertainty creates risk that future reforms reduce attractiveness or eligibility for tax-advantaged accounts directly impacting market size potential [S18][N9]. Custodial arrangements wherein substantial member funds are held via insurance company partners expose HealthEquity indirectly to risks from partner defaults or interest rate volatility affecting contractual yields which management monitors closely to mitigate reputational or financial harm [S18].

Integration execution risk is material given frequent acquisitions necessitating harmonization of IT systems, regulatory compliance standards, personnel retention along with culture alignment critical for realizing synergies without disrupting client service continuity [S13][N3].

What To Watch Going Forward

While explicit forward guidance is limited recently publicly available information suggests monitoring:

- Market share developments amid intensifying competition by asset size and account volumes.

- Adoption metrics for AI-powered tools enhancing member experience or operational efficiency.

- Regulatory updates affecting tax advantages tied to HSAs or complementary products.

- Capital deployment balancing between debt reduction versus strategic acquisitions or share repurchases.

- Ecosystem integration progress measured through API usage expansion or partner satisfaction indices.

- Retention rates reflecting effectiveness of 'Purple' customer service ethos alongside digital experience enhancements.

Conclusion

HealthEquity exemplifies a compelling growth narrative within the U.S healthcare financial services space characterized by an integrated platform tailored for consumer-directed healthcare markets incentivized by favorable tax treatment around HSAs and related vehicles. The company has leveraged organic expansion supported by technology innovation alongside strategic acquisitions driving scale gains culminating in substantially improved profitability metrics. Nonetheless significant execution risks tied primarily to regulatory uncertainty around health benefits taxation regimes coupled with elevated indebtedness amid fierce competition warrant vigilant monitoring going forward.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments