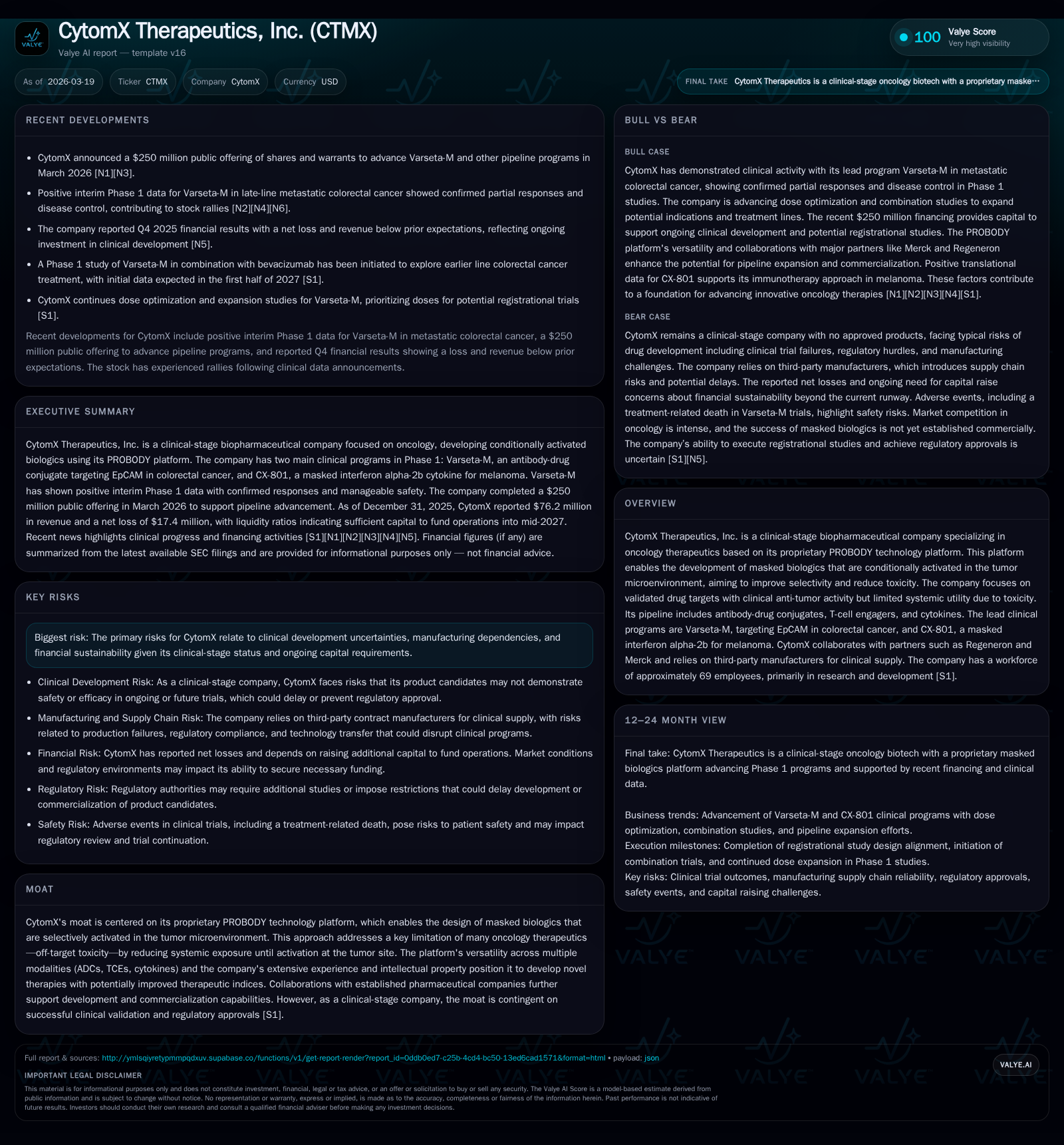

CytomX Therapeutics’ PROBODY Platform Advances with Varseta-M Amid Revenue Decline and Rising Losses

Clinical-stage CytomX focuses on oncology therapeutics leveraging its masked biologics platform while navigating challenging financial trends and capital needs.

CytomX Therapeutics operates at the clinical forefront of oncology drug development with its proprietary PROBODY technology designed to reduce off-target toxicity through conditionally activated biologics. Despite promising Phase 1 data for lead candidate Varseta-M targeting colorectal cancer, the company’s revenue declined nearly 45% in 2025 alongside widening operating losses, reflecting ongoing high R&D investment and limited commercialization. Sustained cash burn necessitated a $250 million equity raise in early 2026 to finance pipeline advancement. CytomX must balance clinical progression of its pipeline against operational costs and regulatory hurdles before potentially transitioning toward commercialization.

Company Overview and Technology

CytomX Therapeutics is a clinical-stage biopharmaceutical company specializing in oncology therapeutics anchored by its proprietary PROBODY® technology platform [S1]. This platform consists of conditionally activated, masked biologics intended to limit systemic exposure until activation by tumor-localized proteases within the tumor microenvironment. This reduces off-target toxicities common to many existing oncology treatments that indiscriminately bind targets expressed on healthy tissues as well as tumors. The platform’s versatility extends across therapeutic modalities including antibody-drug conjugates (ADCs), T-cell engagers (TCEs), and cytokines.

The company's mission targets validated tumor-associated antigens previously limited by safety concerns—attempting systemic targeting unlocked by masking [S1]. CytomX aims to convert targets with known anti-tumor activity but poor therapeutic indices into viable drug candidates.

Historical Financial Performance

CytomX remains pre-commercial, generating revenue primarily from collaboration agreements rather than product sales [S1]. Key financial metrics over recent years are summarized below:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 76 | -17 | -76 | -22 | -44.8% | -154.5% |

| 2024 | 138 | 32 | -86 | 25 | +36.4% | +5700.9% |

| 2023 | 101 | -1 | -56 | -6 | +90.4% | +99.4% |

| 2022 | 53 | -99 | -111 | -101 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -76 | -17.5 |

| 2024 | -87 | -6988.8 |

| 2023 | -57 | 1.2 |

| 2022 | -113 | 115.8 |

Source: SEC companyfacts cache [F1].

Revenue fell sharply by nearly half from $138 million in 2024 to $76 million in 2025 [F1], reflecting the expiration or reduction of milestone payments related to collaborations amid no product sales [S1]. Operating income swung from a positive $25 million in 2024 to a loss of $22 million in 2025 due to increased clinical trial expenditures for lead programs Varseta-M and CX-801 alongside administrative costs [S3]. Net income followed suit.

Operating cash flow remained negative at approximately -$75.6 million in 2025, consistent with significant investments in R&D supporting pipeline advancement [F1]. Capital expenditures were modest relative to operating outlays.

Equity improved significantly to $99 million at year-end 2025 after prior deficits, likely reflecting recent financing activities [F1].

Pipeline and Clinical Progress

Two lead candidates anchor CytomX’s pipeline:

- Varsetatug Masetecan (Varseta-M): A PROBODY ADC targeting EpCAM, overexpressed in colorectal cancer (CRC). Varseta-M is armed with a topoisomerase-1 inhibitor payload similar to irinotecan chemotherapy components used in CRC treatment [S1]. It aims for selective cytotoxic delivery within the tumor microenvironment.

- CX-801: A masked form of interferon alpha-2b designed for conditional activation within tumors, evaluated primarily for melanoma treatment where immune modulation is critical [S1][N1].

Recent positive Phase I data for Varseta-M demonstrated encouraging safety and early efficacy signals, supporting the platform’s potential despite historical challenges with unmasked EpCAM ADCs due to systemic toxicity [N1][N8][S3]. No products have received regulatory approval yet.

Forecasts and Milestones

While explicit guidance is limited, key upcoming milestones include:

- Completion of enrollment and initial safety readouts for Varseta-M colorectal cancer cohorts.

- Advancement of CX-801 melanoma trials assessing safety and biological activity.

- Potential nomination of additional clinical candidates within the PROBODY pipeline based on preclinical progress.

These milestones will be critical inflection points determining progression toward pivotal studies or partnerships [N9][S3]. Regulatory approvals remain several years away contingent on successful clinical outcomes.

Returns and Capital Allocation

Financial returns remain negative due to absence of product sales combined with high R&D investment:

- Approximate return on equity was around -17.5% at end-2025 based on net loss relative to shareholders’ equity [F1].

- Operating cash flows are consistently negative owing primarily to R&D spending rather than operational inefficiencies.

- Capital expenditures are limited, consistent with the company’s focus on research activities.

- No dividends or share repurchases have been declared or executed given ongoing losses [F1].

To address cash needs, CytomX completed a public offering in March 2026 raising gross proceeds of approximately $250 million via shares plus warrants intended primarily to fund late-stage development of Varseta-M and other pipeline programs amid dwindling cash reserves of about $12.7 million at end-2025 [N7][F1]. This financing underscores reliance on capital markets typical for companies with multiple early-stage assets.

Risks Summary

Key risks include:

- Clinical trial failures or delays impacting regulatory timelines and commercial prospects [S1].

- Dependence on third-party manufacturers and CROs introduces operational risk [S1].

- Intense competition particularly in colorectal cancer and immuno-oncology sectors.

- Regulatory scrutiny over pricing, reimbursement policies could constrain market access post-approval [S5,S6,S7].

- Ongoing need for capital raises poses dilution risk and potential funding gaps [S24,S25,N7].

- Intellectual property challenges may arise though none currently material.

Conclusion

CytomX Therapeutics remains an innovator advancing conditionally activated biologics addressing unmet needs in oncology through the PROBODY platform amid financial pressures inherent to clinical-stage biopharma without current product revenues.

Progressive clinical data from Varseta-M provide validation signals supporting future development while recent equity financing strengthens near-term liquidity.

Investors should monitor upcoming trial results along with management’s execution on capital deployment as key indicators of potential transition toward commercialization.

This report synthesizes publicly available data including SEC filings up to March 19, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments