Vanguard Green Investment: Early-Stage Innovation Meets Liquidity Hurdles

VGES, initially a wellness services startup, pivots into green finance amid persistent liquidity constraints and no customer revenue.

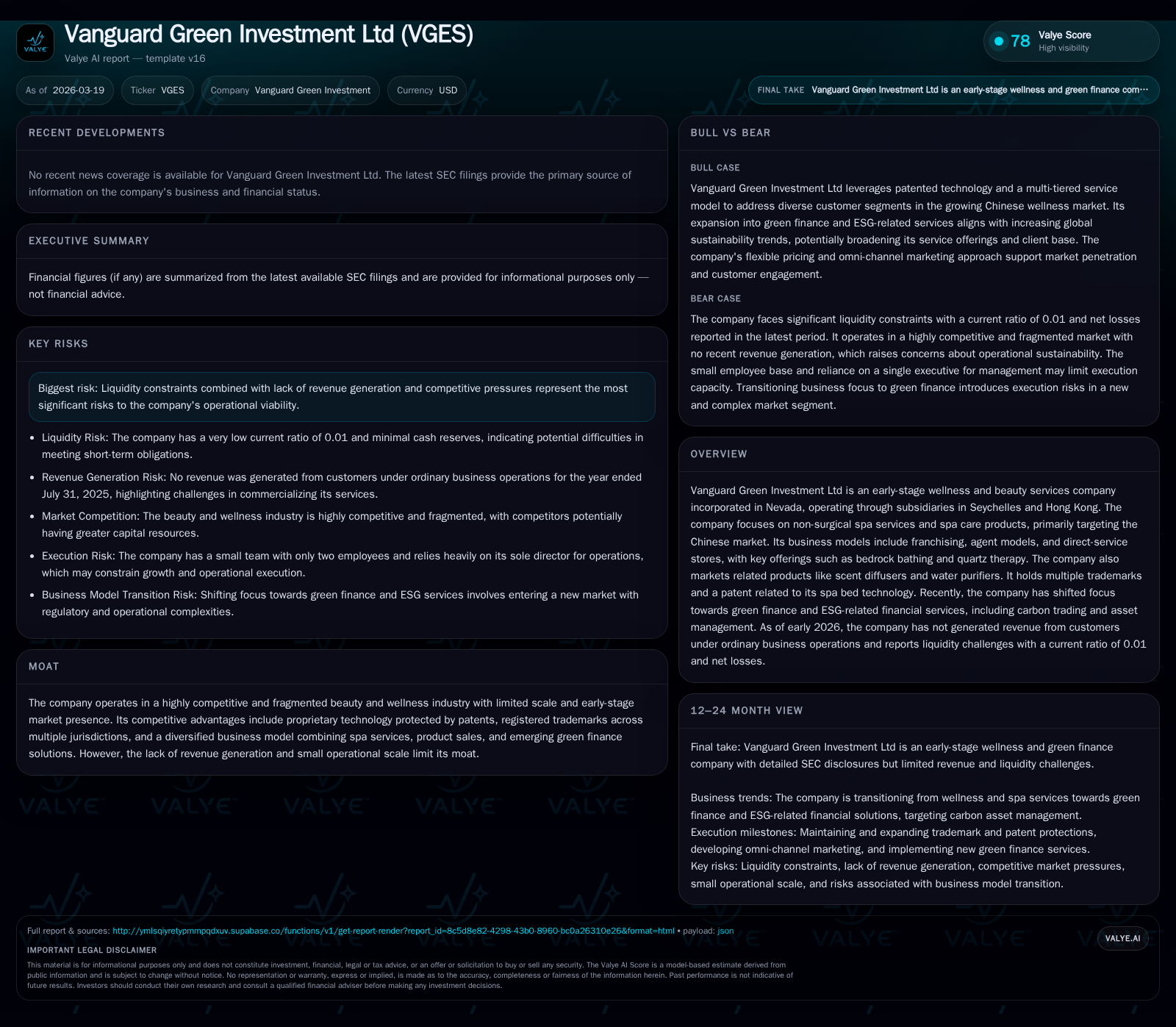

Vanguard Green Investment Ltd began as a niche wellness and beauty services provider focused on the Chinese market but has yet to generate revenue in its ordinary business operations as of early 2026. The company deploys a mix of franchising, agent, and direct-service models largely centered on non-surgical spa treatments using proprietary spa bed technology. Recently it initiated a strategic pivot toward green finance and ESG-related financial services to leverage sustainability trends. However, severe liquidity shortages and ongoing net losses highlight formidable operational challenges ahead.

From SPA Origins: Early Performance and Operational Challenges

Vanguard Green Investment Ltd was incorporated in Nevada in June 2018 under a former name and rebranded in mid-2024. Initially anchored in wellness and beauty services, the company sought to tap the Chinese market’s rising consumer interest in non-surgical spa therapies including its signature bedrock bathing and quartz therapy treatments [S1][S6]. Despite commencing service deployment—such as a Shanghai flagship opening in January 2019—the company has not generated meaningful revenue under ordinary business operations since then. The only recorded topline figure available is approximately $19K as of April 2019 [F1].

Operationally, VGES has reported consistent net losses for multiple years: -$357K FY2022 worsening to -$76K FY2025 latest annual report filing [F1]. Operating income has remained negative as well, with last recorded quarterly operating loss near -$192K (Oct 2019 endpoint). Negative operating cash flow exacerbates these issues — for example, fiscal 2023 posted a CFO deficit above -$63K, underscoring continued cash burn far exceeding any investment inflows [F1]. Financial data also indicate capex remains steady but modest relative to operational outflows around $41K annually by recent counts.

These persistent losses reflect an inability thus far to scale operations or broadly monetize the initial wellness business models amid market headwinds including COVID-related disruptions particularly severe in China’s beauty sector [S6].

Historical performance (annual)

| FY | Net ($) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -76778 | -194.9% | ||

| 2024 | -26035 | +62.2% | ||

| 2023 | -68827 | -63517 | 41811 | +80.7% |

| 2022 | -357333 | -4169 | 41811 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 10.6 | |

| 2024 | 4.0 | |

| 2023 | -105328 | 11.8 |

| 2022 | -45980 | 67.0 |

Source: SEC companyfacts cache [F1].

VGES financial highlights show sustained net losses without reported revenue post-2019. Operating cash flows remain negative with continuous capital expenditures.

Business Model Complexity and Market Positioning in China’s Wellness Sector

To navigate China’s geographically dispersed consumer base characterized by varying cultural preferences and regional demands, VGES adopted a tripartite business model [S6][S13]:

- Franchise model: Partnering with local operators possessing granular market knowledge to rapidly scale service points.

- Agent model: Large-scale chain agents deploying proprietary stone spa bed equipment acting as intermediaries.

- Direct-service stores: Company-operated outlets delivering flagship branded experiences primarily in urban hubs.

This multi-channel approach aims to balance broad market penetration with tailored local execution. The company’s signature offerings include bedrock bathing—a dry hot stone therapy originating from Japanese "Ganbanyoku" tradition—and quartz therapies intended to stimulate physical and mental wellness [S6][S15].

The presence of specialized equipment like their patented thermostatic-controlled stone spa beds supports differentiation within the fragmented wellness industry where many competitors rely solely on standard massage or cosmetic services [S7]. However, given the early-stage nature of operations with only two employees reported as of mid-2025 [S4], scalability remains impractical without substantial capital infusion.

The highly fragmented Chinese wellness industry also entails fierce competition from better-capitalized incumbents and numerous regional players, complicating VGES’s path to achieving operational critical mass or brand recognition [S6].

Pivot Toward Green Finance and ESG: New Horizons and Market Realities

Recognizing the limitations inherent within its core wellness segment compounded by liquidity distress, VGES embarked on a strategic pivot during late 2024 toward green finance and ESG-focused financial services [S7][S9]. This transition encompasses offerings such as carbon trading platforms, carbon pledge financing programs, carbon custody solutions, along with broader ESG-compliant asset management aimed at investors seeking sustainable investment vehicles.

This pivot leverages global sustainability trends and regulatory momentum promoting carbon reduction initiatives [S4]. By combining traditional wellbeing concepts with emerging green finance opportunities, VGES intends to craft innovative hybrid solutions that meld health improvement with environmental stewardship.

Nonetheless, this pivot occurs while retention of significant competitive disadvantages persists—including negligible revenues from prior operations and minimal liquidity buffers [F1]. Early-stage status within an unrelated financial domain outside core competencies potentially heightens execution risk given limited resources [S7].

Path to Revenue: Milestones to Watch Amid Zero Current Sales

With ordinary course revenues absent through July 2025 filings [F1][S6], future growth will depend heavily on clear milestone achievements against two fronts:

- Expansion of franchising contracts or agent agreements leading to widespread deployment of patented stone spa beds generating leasing or service fees.

- Launch of green finance products such as carbon trading facilities producing fee income or asset management mandates growing client assets under administration.

Neither source currently contributes observable revenue; therefore investors should monitor announcements around franchise openings beyond pilot projects or early customer acquisitions within ESG products. Adoption metrics such as number of active franchisees or value traded on the carbon platform would provide critical insights into commercial traction.

Given historical precedents with prior wellness segment stagnation despite flexible pricing tiers (membership bundles for bedrock bathing packages) [S13][S15], measurable topline ramp is uncertain absent catalytic partnerships or scale capital injections.

Capital Structure and Liquidity: Struggles Amid Expansion Plans

Perhaps most concerning are VGES’s severely constrained liquidity metrics indicating substantial short-term solvency risks. As of Q1 2026:

- Cash & equivalents stand at an alarming $55 only,

- Current assets total $5,110,

- While current liabilities amount to $758,724,

- Resulting in an extremely weak current ratio of approximately 0.01 [F1].

Equity is deeply negative at nearly -$725K by FY25 year-end reflecting accumulated deficits eroding shareholder value steadily over time [F1]. No dividends or share repurchases have been made reflecting absence of distributable profits or discretionary capital policies.

Operating cash flows remain consistently negative with free cash flow approximated near -$105K recently (CFO minus capex), indicating ongoing dependency on external financing or asset disposals for operational continuity [F1].[S7]

Capital allocation appears suboptimal given persistent cash depletion coupled with ongoing capital expenditure outlays that have not yet catalyzed profitable sales expansion—reflecting either high customer acquisition costs or insufficient product-market fit at scale.

Intellectual Property Assets Supporting Service Differentiation

A notable asset underpinning VGES's unique service proposition is its thermostatic control setting patent for stone spa beds granted by Singapore Intellectual Property Office in June 2021 valid until September 2039 [S7]. This patent relates to integrated heating element regulation aimed at enhancing energy efficiency during therapy sessions—a meaningful innovation within therapeutic hardware niches.

Additionally, the company holds multiple trademarks registered across Hong Kong, Saudi Arabia, UAE, Singapore among others covering product designations related to fragrance diffusers and water purifiers aligned with its wellness product suite [S16][S17]. These IP protections erect some barriers against commoditization providing legal defensibility for branded offerings across international markets.

Such proprietary technologies can be critical differentiators given the commoditized nature of many spa treatments competing primarily on price rather than technical sophistication.

Risks Amplified: Competitive Pressure and Funding Constraints

The convergence of fierce competition within the fragmented beauty & wellness space alongside VGES's lack of operational scale intensifies risk exposures substantially. Competitors with greater capitalization can invest more aggressively into marketing campaigns and geographic spread threatening market share gains for VGES despite niche offerings [S3][S8].

Further compounding challenges are ongoing net losses magnified by a negative equity balance signaling persistent erosion without immediate path to profitability [F1]. Legal disclosures acknowledge potential operational risks common among early developmental ventures but no material litigation pending at present [S3][S10][S12].

Liquidity insufficiency remains paramount—working capital very low restricts ability to absorb shocks or fund expansions organically. If new green finance ventures fail to gain traction swiftly enough to generate positive cash flows, financial distress could materialize imminently demanding recapitalization measures.[F1]

Financial Outlook Summary and Analytical Watchpoints

While no explicit guidance exists regarding revenue targets or break-even horizons given the company's early stage status underpinned by limited track record,[N/A] investors monitoring VGES should prioritize key performance indicators including:

- Number of franchises opened and active lease contracts signed for stone spa beds;

- Client acquisition rates within green finance products such as carbon trading volumes;

- Changes in operating cash flow burn rate indicating improved cost control or revenue inflows;

- Movement in liquidity ratios signaling alleviation or worsening financial constraints;

- Progressive milestones linked to intellectual property commercialization or product launches.

Absent material inflection points along these vectors, VGES faces sustained uncertainty balancing innovation aspirations against stark liquidity realities.

This analysis synthesizes public SEC filings through Q1 2026 along with latest available financial data without projecting forward-looking earnings owing to insufficient disclosed guidance. Given Vanguard Green Investment Ltd’s unique dual-sector positioning straddling wellness services and nascent green finance initiatives amid acute funding pressure, stakeholder vigilance over execution capability remains crucial.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments