Forgent Power Solutions Powers Forward Amid Market Challenges

Forgent leverages engineered-to-order expertise and manufacturing integration to sustain growth amid supply and cost pressures.

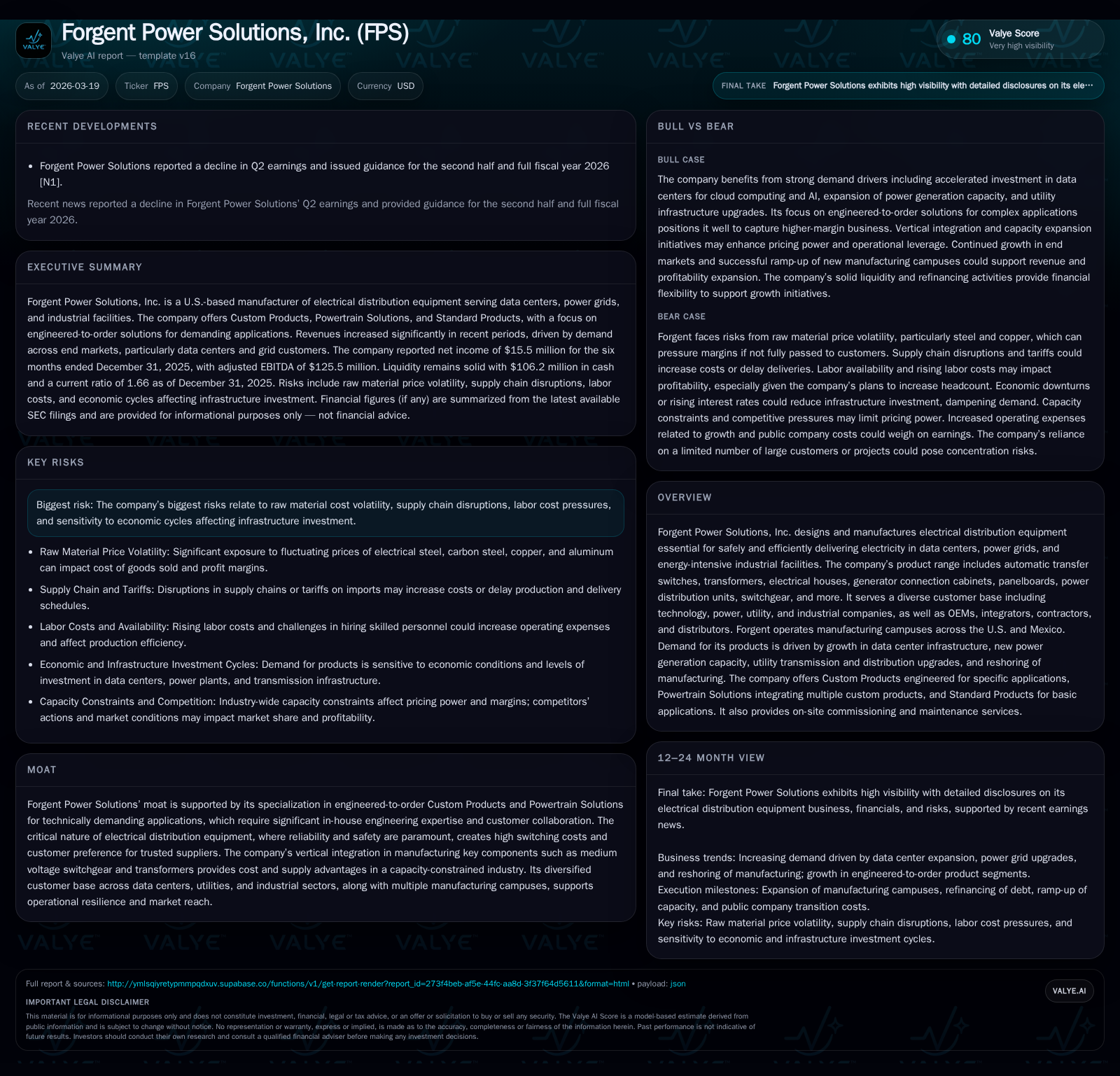

Forgent Power Solutions, a key manufacturer of electrical distribution equipment crucial for data centers, utilities, and industrial applications, has demonstrated strong revenue growth driven by rising demand in data infrastructure and power grid upgrades. Its strategic focus on custom engineered products and vertical integration creates a defensive moat amid industry capacity constraints and input cost volatility. Although profitability faces margin pressure from labor and material inflation alongside fixed cost absorption linked to new campuses, Forgent maintains solid liquidity supported by recent refinancing. Future prospects hinge on backlog conversion and capacity expansion progress as the company addresses evolving electrical infrastructure needs.

Forgent’s Growth Trajectory: Historical Financial Performance and Drivers

Forgent Power Solutions posted robust top-line growth in fiscal 2025 driven predominantly by surging sales of Custom Products and Powertrain Solutions tailored for demanding applications such as data centers and utility grids. Quarterly revenue for Q4 ended December 31, 2025 increased 69% year-over-year to approximately $296 million from $175 million a year prior. For the first six months of fiscal 2025, revenues reached roughly $580 million reflecting a substantial uplift of 76% relative to the same period last year [F1][N1].

This impressive growth traces back to intensified global build-out of digital infrastructure — including AI-driven data center expansions — coupled with upgrades across transmission & distribution (T&D) networks necessitated by rising load demands. Additionally, reshoring trends in manufacturing further buoyed orders for electrical distribution equipment particularly engineered-to-order solutions requiring collaboration with customers on design specifics.

Despite top-line acceleration, operating income scaled more modestly to about $20 million in Q4 (up 6%) while increasing about 23% over the first half year to over $51 million. The relatively constrained margin expansion owes partly to increased fixed overhead tied to new manufacturing campus startups, under-absorbed labor costs due to accelerated hiring schedules, and one-time startup expenses at recently commissioned facilities aimed at boosting capacity [F1][N1].

Historical Financial Summary FY24–FY25

Historical performance (annual)

| FY |

|---|

| 2026 |

Source: SEC companyfacts cache [F1].

Note: Net income includes adjustments related to non-controlling interests per filings [F1].

Custom Products and Vertical Integration: The Moat Behind Forgent’s Success

Forgent’s competitive edge rests heavily on its specialized engineering expertise enabling highly customized electrical distribution equipment that addresses specific project requirements. These "engineered-to-order" Custom Products necessitate close collaboration between Forgent’s in-house engineering teams and customers — especially for complex applications demanding stringent reliability, custom form factors, thermal management capabilities, and regulatory compliance.

Vertical integration into manufacturing critical components such as medium-voltage switchgear and transformers bolsters Forgent’s supply resilience amid sector-wide capacity bottlenecks. This integration not only reduces dependency on external suppliers but also enhances cost control compared with competitors who must outsource these complex subassemblies. Such manufacturing scope improves pricing power particularly during material shortages or tariff fluctuations.

High switching costs arise because replacing critical distribution equipment can be prohibitively disruptive given safety considerations plus risk of operational downtime or damage — reinforcing customer loyalty towards trusted providers like Forgent possessing proven product reliability track records [S6][S8].

Market Dynamics Shaping Demand: From Data Centers to Reshoring Initiatives

Demand for Forgent's solutions is accelerating along several major vectors. AI-enabled computing surges require substantial new data center construction leading to increased demand for robust electrical distribution frameworks supporting uninterrupted power delivery. Simultaneously, independent power producers are adding generation capacity addressing growing electricity needs.

Utilities face pressure to upgrade T&D infrastructure responsive to rapid load growth driven by electrification trends plus decarbonization initiatives demanding grid modernization. Furthermore, global trade tensions and tariff complexities have encouraged manufacturers to reshore critical production facilities domestically — consequently generating fresh demand for customized electrical equipment compatible with modern industrial processes [N1][S6].

This confluence of factors spans multiple end markets—technology sectors building data centers, regulated utilities upgrading grids, and industrial customers reshoring operations—broadening Forgent's addressable market.

Capacity Constraints and Supply Chain Pressures: Operational Challenges

Forgent operates within an industry currently marked by constrained production capacity across many product categories compounded by raw material price volatility primarily affecting steel and copper inputs essential for transformers and switchgear assemblies.

Tariffs on foreign imports exacerbate these cost pressures while geopolitical disruptions could pose additional supply chain risks. Labor markets are tight around manufacturing hubs requiring significant hiring efforts combined with increased wages which collectively inflate operating expenses.

These dynamics challenge margin stability due to operating leverage effects where fixed overhead grows faster than revenues during capacity ramp-ups or when new plants are not yet operating at full utilization levels. Effective absorption of these costs hinges on scaling throughput efficiently alongside maintaining quality standards mandatory for safety-critical equipment [S5][S25].

Profitability Patterns and Margin Analysis: Impact of Product Mix and Input Costs

Forgent’s gross margins exhibit variability aligned closely with shifts in product mix. Custom Products command higher margins reflective of significant engineering inputs justifying a customization premium whereas Standard Products are more commoditized with typical pricing elasticity limiting margin expansion.

Vertical integration affords some insulation from input cost fluctuations by controlling key component production internally; however, surging raw material prices combined with labor escalation dilute margin gains especially during periods of fast-paced hiring before workers achieve full productivity.

Under-absorbed fixed overhead tied to recently opened campuses also depress margins temporarily until volume ramps smooth unit cost loads. Moreover, quarter-to-quarter changes in service revenue proportions add complexity influencing overall profitability patterns beyond hardware sales alone [S8][N1].

Capital Structure Update: Liquidity, Debt Position, and Cash Flows

As of December 31, 2025, Forgent held cash and cash equivalents approximating $106 million supplemented by net working capital around $231 million evidencing solid short-term liquidity cushions. A recent refinancing raised about $594 million in lower-cost long-term debt enabling repayment of prior higher-cost borrowings totaling approximately $511 million thus optimizing interest expense profiles [F1][S4].

Despite strong revenues, free cash flow is negative roughly $50 million primarily reflecting aggressive capital expenditures focused on expanding manufacturing capacity undertaken through FY26. Operating cash flow generation remains positive but constrained relative to prior period due largely to increased working capital needs driven by backlog builds including higher accounts receivable balances tied to elevated sales volumes [F1][S9].

This financial positioning supports ongoing expansion but requires careful management of leverage ratios and interest coverage as the company grows.

Future Outlook: Order Backlog, Investment Plans, and Market Opportunities

Forgent reports increasing order backlog signifying demand visibility underpinning near-term revenue projections. Capital spending plans emphasize completion of new production campuses expected by end FY26 aiming at alleviating current capacity constraints allowing better absorption of fixed costs while accommodating anticipated volume growth across data center and grid sectors [N1].

Technology evolution within AI workloads alongside regulatory drives augmenting grid resilience point toward sustainable demand drivers going forward. Investors will keenly monitor timeline execution on capacity ramp-ups combined with gross margin trajectories influenced by raw material price trends.

Investor Watchpoints: Milestones, Risks, and Key Metrics to Monitor

Key milestones include achieving full operational capability at expanded manufacturing campuses projected through FY26 which should enhance operating leverage benefits potential.

Risks warranting continuous assessment involve volatile commodity inputs (steel/copper), labor market tightness pushing wages upward further than forecasted levels, supply chain interruptions possibly delaying deliveries or inflating inventory holding costs alongside macroeconomic shifts potentially dampening capital spending among utilities or industrial customers [S25].

Financial metrics such as adjusted EBITDA—used internally for compensation benchmarking—and operating income progression provide enhanced insights beyond GAAP figures considering one-time non-cash items or IPO-related expenses [S2]. Close observation on backlog conversion efficiency into revenues will provide early signals about market traction.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available information as of March 2026 without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments