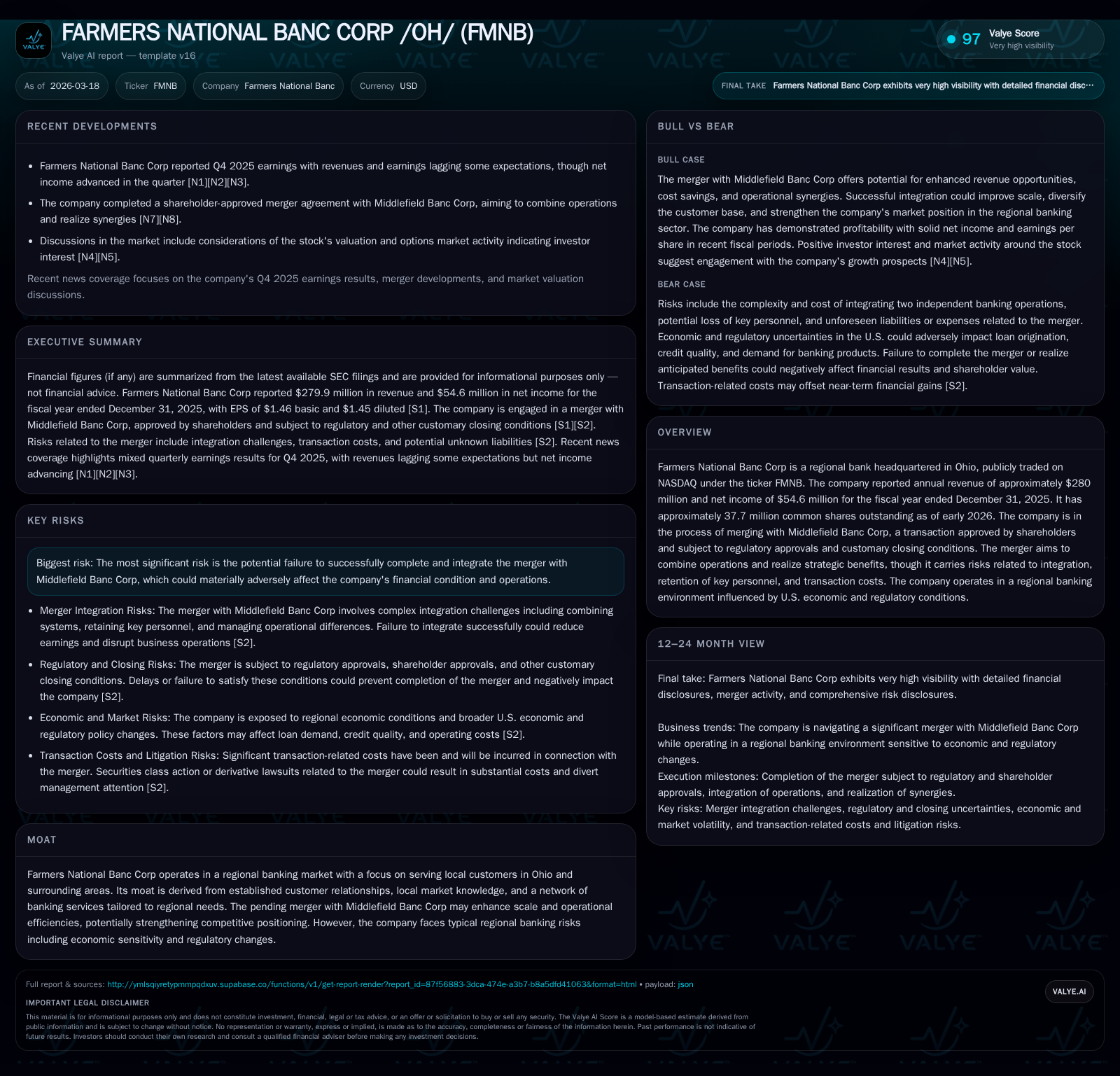

Farmers National Banc’s Growth Trajectory and Merger Ambitions in Ohio's Regional Banking

Farmers National Banc Corp has shown steady financial growth and is poised to reshape its regional footprint through a transformative merger, while navigating integration and regulatory challenges.

Farmers National Banc Corp reported solid revenue and net income growth for fiscal 2025, building on a multi-year performance improvement driven by stable local banking operations. The company is advancing a significant merger with Middlefield Banc Corp, approved by shareholders but pending regulatory approvals, aiming to capitalize on scale efficiencies and market expansion. However, integration complexities and regulatory uncertainties present material risks that could affect operational continuity and financial outcomes. Capital allocation remains disciplined with consistent dividends but no recent buybacks, reflecting cautious liquidity management amidst merger plans.

Financial Growth Patterns: Solid Gains Amid a Dynamic Market

Farmers National Banc Corp has exhibited a commendable upward trajectory in its financials over the recent fiscal periods. Its revenue reported for FY2025 stood at approximately $280 million, marking a 3.9% increase over FY2024's $269 million figure [F1]. This steady top-line expansion reflects ongoing demand for regional banking services within Ohio and surrounding locales where Farmers has entrenched customer relationships.

More strikingly, net income surged 18.8% year-over-year from about $45.9 million in FY2024 to $54.6 million in FY2025 [F1]. This acceleration suggests effective cost controls or credit quality improvements despite broader economic headwinds. Operating cash flow told a somewhat different story: it declined by approximately 9.9% in the same period to $60 million, signaling either working capital shifts or near-term operational cash usage increases [F1]. Conversely, capital expenditures contracted notably by nearly a third (32.8%) to around $7.9 million in FY2025 from nearly $11.7 million the prior year, indicating cautious investment spending aligned with scaling considerations [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 280 | 55 | 60 | 8 | +3.9% | +18.8% |

| 2024 | 269 | 46 | 67 | 12 | -8.0% | |

| 2023 | 50 | 62 | 4 | +273.9% | ||

| 2022 | 13 | 84 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 52 | 11.2 |

| 2024 | 0 | 55 | 11.3 |

| 2023 | 12 | 58 | 12.3 |

| 2022 | 0 | 78 | 4.6 |

Source: SEC companyfacts cache [F1].

Table: Historical Performance Summary (FY2022–FY2025)

Merger with Middlefield Banc Corp: Strategic Rationale and Integration Risks

The company's ongoing pursuit of a merger with Middlefield Banc Corp represents a pivotal inflection point—a regional nexus transition aimed at boosting overall scale and operational efficiencies [S1][S16][S17]. Shareholders have ratified this deal decisively as of early 2026, demonstrating confidence in the strategic rationale behind expanding geographic reach and consolidating banking platforms given intense local competition and net interest margin pressures inherent to regional bank ecosystems.

Nonetheless, the merger carries an embedded integration risk premium typical for such transactions within regulated bancorp jurisdictions: aligning complex IT systems, harmonizing operational procedures, merging divergent corporate cultures, and retaining key personnel pose substantial challenges that may detract from intended benefits or delay synergy realization [S5][S6]. These transactional complexities are compounded by potential unknown liabilities or unforeseen expenses that could erode near-term earnings or liquidity.

Legal exposures also accompany the process as securities class action or derivative suits related to the Merger Agreement could impose unanticipated costs adversely affecting overall financial condition [S6][S10]. Thus far, Farmers has acknowledged these risks explicitly, signaling a cautious but determined approach bolstered by governance oversight.

Navigating the Regulatory and Economic Landscape Affecting Regional Banks

Regional banks like FMNB operate under a particularly dynamic backdrop shaped by sudden shifts in U.S. federal policies that alter regulatory examination priorities and enforcement attitudes among agencies governing financial institutions [S2][S5]. Recent years have seen sharp changes in trade restrictions, tariffs, and monetary policy imbued with inflationary pressures that reverberate throughout lending volumes and credit quality.

Macroeconomic uncertainty—chiefly potential recession scenarios combined with fluctuating consumer confidence—may constrain loan origination pipelines or amplify credit losses if borrowers encounter repayment difficulties due to local economic contractions [S2]. Further unpredictability arises from structural U.S government dysfunction risks impacting financial markets broadly.

Farmers' business model hinges critically on nuanced asset-liability management practices calibrated for regional deposit franchises sensitive to such stimulus shifts; maintaining compliance amid evolving federal mandates also adds incremental operating expense burdens that may influence profit margins [S5].

Capital Allocation Framework: Balancing Dividends, Buybacks, and Investments

Amidst this transition phase triggered by the impending merger, Farmers National Banc appears prudent in its capital deployment strategies [F1][S16][S17]. The bank sustained consistent dividend distributions across recent years reflecting commitment to shareholder income stability; however, it refrained from share repurchases during FY2024 and FY2025 following a modest buyback program totaling roughly $11.5 million completed in FY2023 – indicative of conservative liquidity management pending integration uncertainties.

Reducing capital expenditures substantively last year further underscores restraint favoring free cash flow preservation rather than aggressive expansion outlays during this transformation interval [F1]. These moves collectively suggest measured discipline designed to underpin balance sheet robustness without sacrificing operational agility.

Profitability Metrics and Return on Equity Analysis

Calculating return on equity for FY2025 — derived from net income of approximately $54.6 million over shareholders’ equity approximating $485.7 million — yields an ROE near 11.2% [F1]. This level denotes an efficient use of equity capital consonant with typical benchmarks observed among regionally focused banks.

Profitability drivers include stable interest income supported by tight local market relationships combined with judicious cost controls as evidenced by net income gains outpacing revenue increases significantly last year [F1]. Although explicit margin compositions are not disclosed, such ROE sustains Farmers’ positioning amidst intensifying pressure on net interest spreads observed industry-wide.

Liquidity, Debt Profile, and Funding Strategy

Liquidity disclosures reflect a well-managed capital structure without major reliance on volatile debt forms; no new significant borrowings have been documented recently — consistent with sector tendencies favoring core deposit bases augmented by conservative leverage postures ahead of large-scale structural consolidation efforts like mergers [S4][S7][S8][S25].

Core deposit funding remains essential given historical stability exhibited within Farmers’ franchise territory. The absence of fresh debt issuance indicates an intent to avoid layering refinancing complexities during regulatory evaluations accompanying the merger.

Cash balances reported latest date back several years due to data limitations but past indications suggest sufficient buffers exist alongside capital reserves maintained per regulatory standards.

Forward Outlook: Key Milestones and Market Watchpoints

While explicit forecasts are not provided within current disclosures, monitoring specific milestones is paramount for stakeholders tracking FMNB's evolution:

- Timely satisfaction of merger closing conditions including regulatory clearances remains critical given their uncertain duration and potential gating effects on transaction completion [S13].

- Effective integration leadership appointments—such as the recently named Chief Banking Officer tasked with overseeing post-merger orchestration—signal proactive governance focus on seamless operational fusion [S3].

- Realization of expected synergies involves close scrutiny as delays or shortfalls could materially affect earnings trajectories jeopardizing anticipated value creation objectives outlined at announcement.

- Market perception sensitivity towards any litigation developments or unexpected cost overruns may cause share price volatility absent offsetting positive operating newsflows.

In aggregate, Farmers National Banc enters a high-stakes chapter balancing momentous growth ambitions through acquisition against inherent risks prevailing across regulated mid-sized community banking spaces.

This analysis synthesizes disclosed company filings and accessible financial data as of March 18, 2026 without extrapolations beyond stated information or speculative projections outside officially communicated parameters.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments