Harte Hanks Inc Confronts Revenue Slump While Advancing Project Elevate Transformation

Harte Hanks faces a challenging revenue decline and rising pension costs, offset by leadership realignment and efficiency-focused transformation efforts.

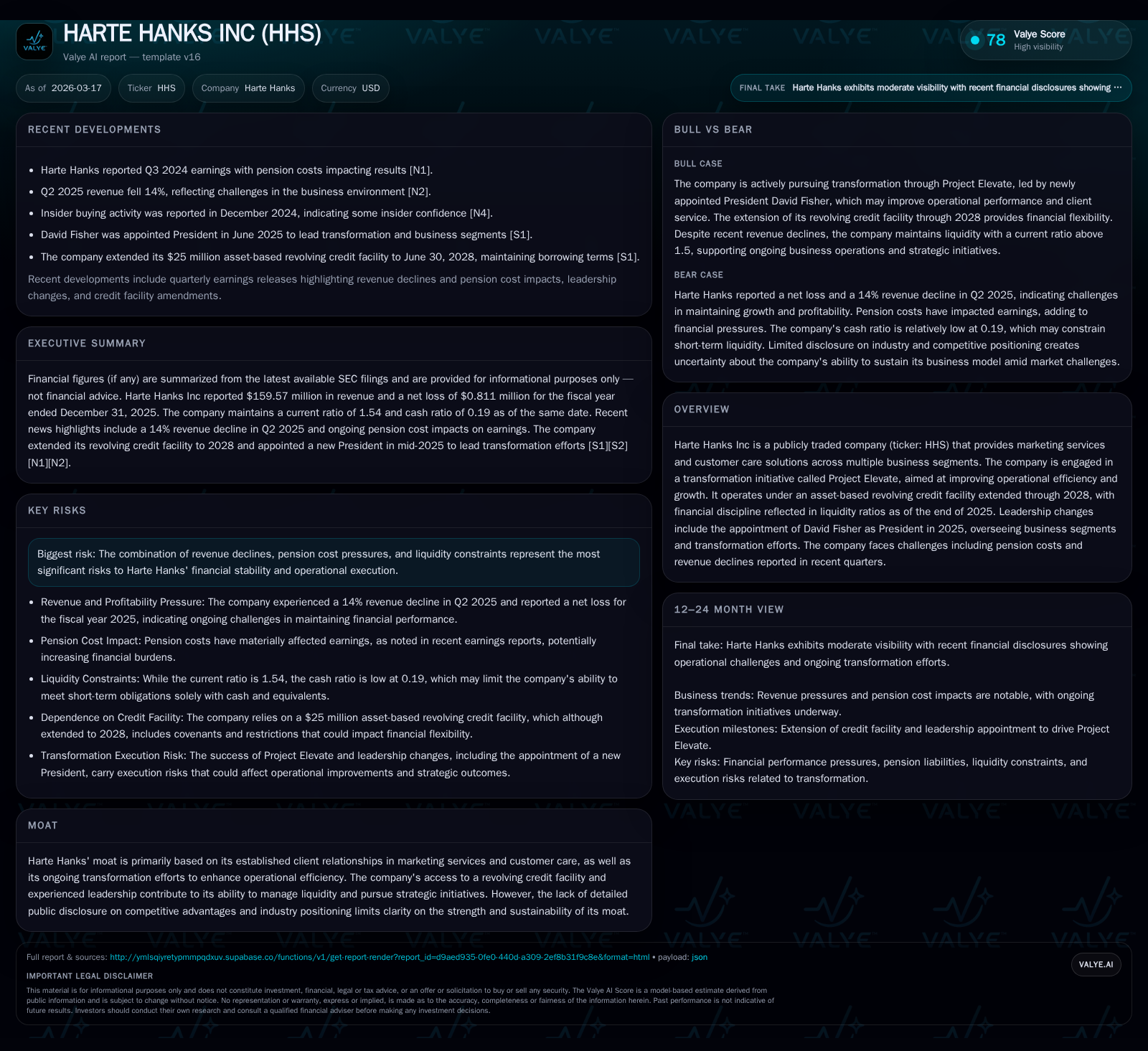

Harte Hanks Inc has experienced consistent top-line contraction since 2022, with revenues falling nearly 14% in 2025 and operating income suffering steep compression. Amid these headwinds, the company is driving operational improvement through its Project Elevate initiative under newly appointed President David Fisher. Liquidity management benefits from a $25 million asset-based revolving credit facility extended to 2028, although free cash flow remains negative due to operating losses and capital expenditure. Pension cost pressures and ongoing revenue declines present clear risks that could restrain near-term recovery despite the strategic refocus underway.

Historical Performance: Revenue Downturn and Profit Compression

Since 2022, Harte Hanks has faced sustained top-line contraction, with revenues declining from $206 million to $160 million by the end of 2025—a compound pressure culminating in a -13.9% drop year-over-year most recently [F1]. This reduction in scale exerted considerable EBITDA pressure with operating income shrinking precipitously by about 81.6% last year to just $0.39 million. The company’s margin compression reflects increased cost burdens relative to declining sales volumes, further underscored by the swing into recurring net losses: although net income loss narrowed substantially to -$0.81 million in 2025 from a severe -$30 million hit in 2024, profitability remains elusive [F1].

Operating cash flows echo the earnings challenges; positive inflows of $29 million in 2022 gave way to distinctly negative cash generation of around -$1.7 million in the latest fiscal year amid the free cash flow squeeze caused by persistent operating losses and working capital demands. Capital expenditures followed a prudent trimming trend from $5.8 million in 2022 down to approximately $2.8 million in 2025 reflecting tightened capital discipline as part of the company’s turnaround focus [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 160 | -1 | -2 | 0 | -13.9% | +97.3% |

| 2024 | 185 | -30 | -3 | 2 | -3.3% | -1829.7% |

| 2023 | 191 | -2 | 10 | 3 | -7.2% | -104.3% |

| 2022 | 206 | 37 | 29 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -4 | -4.0 | |

| 2024 | 0 | -7 | -139.7 |

| 2023 | 2 | 8 | -7.9 |

| 2022 | 23 | 195.5 |

Source: SEC companyfacts cache [F1].

Table: Harte Hanks Historical Financial Summary (FY2022-FY2025) [F1]

This historic profile depicts a business grappling with top-line contraction that cascades into margin erosion and tightening liquidity.

Project Elevate: Steering Operational Efficiency Amidst Market Headwinds

Harte Hanks embarked on Project Elevate as its signature turnaround program designed to boost operational efficiency within its marketing services and customer care portfolio ([N1], [S13]). This initiative targets structural cost rationalizations, process optimizations, and enhanced integration between its main business lines to arrest margin deterioration caused partly by commoditization pressures in outsourced marketing solutions.

The transformation office institutionalizes efficiency levers including labor productivity improvements, technology adoption for workflow automation, and renegotiation of vendor contracts—common levers among legacy-marketing service firms undergoing digital pivoting efforts.

Progress integration into broader business segment strategy creates synergy capture opportunities while attempting to stabilize client retention rates amid competitive market dynamics documented in segment disclosures ([S4]). The ongoing nature of Project Elevate underscores incremental benefit realization rather than immediate results.

Leadership Evolution: David Fisher’s Role in Renewal and Oversight

In June 2025, David Fisher was appointed President following his tenure as Chief Transformation Officer ([S13]). His mandate covers direct supervision of Harte Hanks’ four principal business units—including Marketing Services and Customer Care—and stewardship of Project Elevate's execution alongside M&A initiatives.

Fisher’s compensation package aligns incentives with turnaround success featuring base salary plus up to a full base salary bonus threshold paired with staged stock options and RSU awards vesting over three years—a typical structure aimed at retaining transformation officers focused on medium-term structural change ([S13]).

This leadership consolidation conveys governance intent to streamline decision-making for accelerating operational turnaround while pulling together oversight on capital allocation aligned with synergy capture potential.

Financial Position: Liquidity Management and Revolving Credit Facility Dynamics

Critical to managing near-term challenges is Harte Hanks’ liquidity posture supported by an asset-based revolving credit facility (ABL) originally set at $25 million and extended via second amendment through June 30, 2028 ([S6], [S9]). This facility ties availability primarily to borrowing base calculations centered on cash, equivalents, and accounts receivables—typical asset-based lending characteristics providing flexibility aligned with working capital fluctuations.

At amendment time mid-2025, borrowings were zero with only $1 million in letters of credit outstanding—implying disciplined usage relative to available capacity ([S6]). Covenants embedded include classic restrictions on new indebtedness issuance, dividend pay-outs, liens creation, mergers or acquisitions approval controls, all designed to safeguard lender interests ([S9]).

The current ratio stood at roughly 1.54 at FY-end indicating adequate short-term coverage ([F1]). The ABL agreement also includes an accordion feature permitting a lender-approved increase of up to $10 million augmenting strategic optionality for further borrowing capacity expansion should conditions improve or acquisition opportunities arise.

This structure situates Harte Hanks within typical asset-light funding mechanisms common among marketing service firms balancing working capital needs without resorting to term debt burdens.

Capital Allocation Practices: Dividends, Buybacks, and Free Cash Flow Constraints

Historical capital allocation reflects caution grounded by persistent negative free cash flow trending since early loss periods with no dividends paid recently ([F1], [S11]). Notably shares repurchased showed some activity in prior years but dropped off entirely from FY24 onwards coinciding with widening operating margins pressures.

The approximate negative free cash flow calculated as operating cash flow less capex was around -$4.5 million for FY25 signifying ongoing squeeze on internal funds available for discretionary spending or shareholder returns ([F1]). Capital expenditure cuts have been tactical—reducing from nearly $6 million several years ago down below $3 million suggesting prudence during this turnaround phase.

Planned uses of liquidity remain focused on project funding rather than shareholder distributions given the priority placed on structural repair amidst volatile earnings dynamics and pension-related costs exerting further margin pressures ([N1], [S19]).

Growth Outlook and Market Risks: Pension Costs and Revenue Headwinds

Pension obligations stand out as a key margin risk factor addressed explicitly by Harte Hanks’ latest filings where higher pension-related expenses exacerbate cost structures amid rolling revenue declines ([N1],[S2],[S5],[S7]). This burden complicates near-term cash flow management especially given their typical non-discretionary nature.

Concurrently, the shrinkage in revenues is partially attributed to client retention difficulties compounded by increasing commoditization trends across marketing services sectors where pricing power wanes against digital alternatives ([S4],[N1]). Such headwinds challenge efforts to stabilize top-line growth even as project-driven (~Project Elevate) efficiencies aim for offsetting impacts.

With no recent updates altering risk profiles per latest quarterly disclosures ([S7]), these factors collectively underscore material operational constraints potentially capping growth prospects until a successful durable turnaround materializes.

What to Monitor: Key Results, Milestones, and Financial Covenants

From an analyst perspective, key inflection points include tracking quarterly operating results for signs of stabilization or improvement in both revenue trends and margin profiles post-Project Elevate initiatives rollout ([N1],[S17],[S18]). Milestone achievements within Elevate related process efficiencies or contract wins would indicate momentum gains.

Simultaneously monitoring covenant compliance under the ABL agreement is critical given borrowing base sensitivity particularly if working capital metrics worsen during prolonged revenue weakness ([S6],[S12],[S15],[S17]).

Liquidity metrics such as current ratio preservation above critical thresholds coupled with incremental enhancements in operating cash flow could signal successful structural adjustment ameliorating free cash flow deficits.

Investors should also watch leadership transitions beyond Fisher’s presidency for continuity given recent executive retirements reducing corporate governance depth ([S19]).

This analysis leverages publicly disclosed financial data from SEC filings through FY25 alongside recent news coverage without speculation beyond documented company facts or stated risks related to Harte Hanks' performance trajectory and strategic initiatives.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments