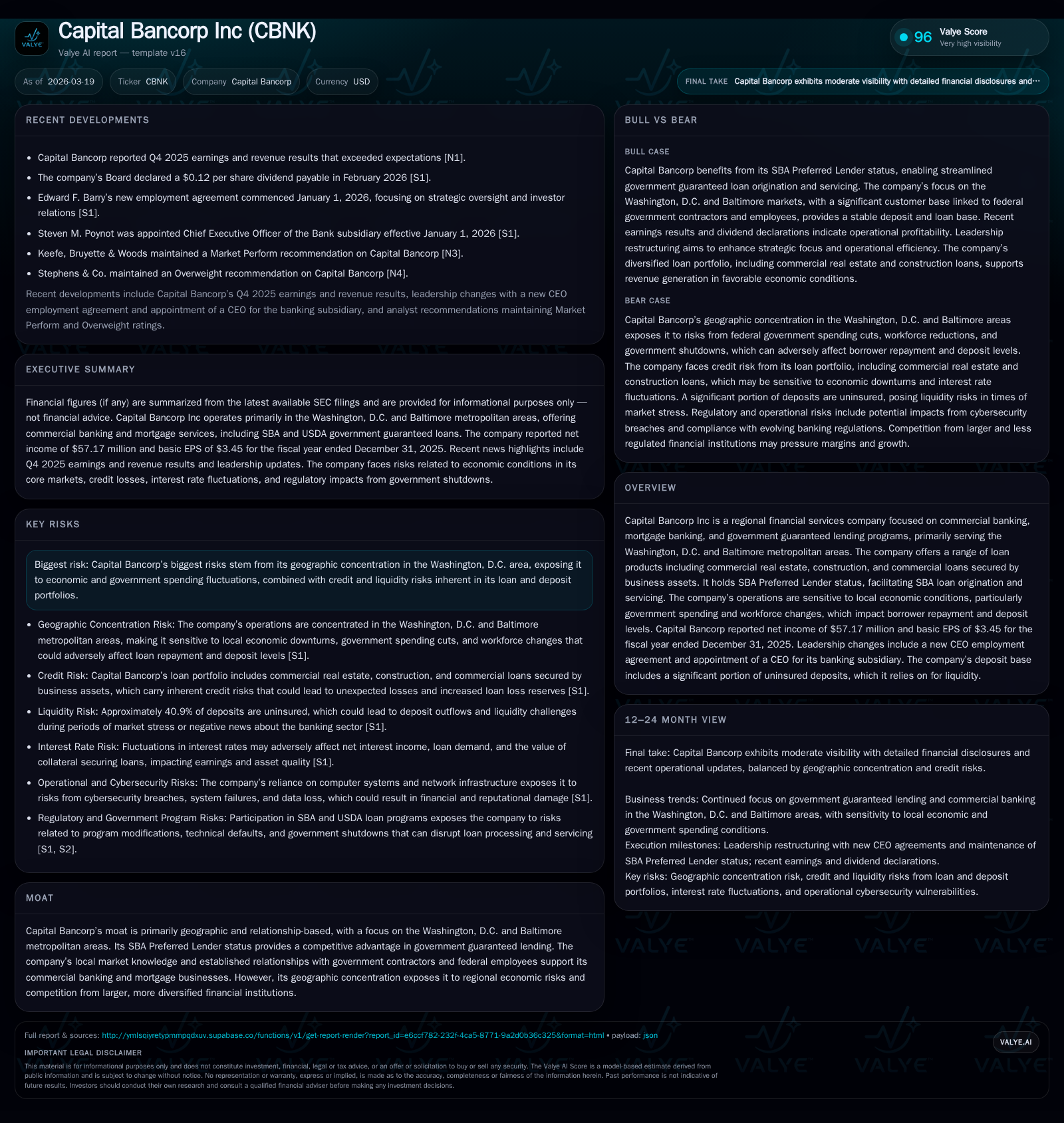

Capital Bancorp’s Earnings Surge Highlights Regional Bank Resilience

Capital Bancorp leverages its Washington, D.C. metro area focus and SBA lending expertise to drive a significant 2025 earnings rebound amid ongoing regional economic and regulatory challenges.

Capital Bancorp Inc reported a sharp resurgence in profitability for fiscal year 2025, with net income soaring 84.6% year-over-year to $57.17 million [F1]. This turnaround is largely underpinned by its specialization in SBA Preferred Lender programs and deep hometown banking relationships in the Washington, D.C. and Baltimore areas, despite ongoing government shutdown pressures impacting loan origination and borrower repayment [S1][S2]. The bank faces material risks from regional economic concentration, elevated commercial real estate loan concentrations, and liquidity sensitivities due to its uninsured deposit base representing approximately 40.9% of total deposits [S1][S17]. Capital allocation shows renewed confidence with an aggressive share repurchase program surpassing $11 million in 2025 alongside rising dividends, supporting an estimated return on equity of 14.2% [F1][S14].

From Struggle to Strength: Historical Financial Trajectory

Capital Bancorp’s financial results from FY2022 through FY2025 illustrate a meaningful operational rebound driven by its core lending niches. Net income fell from $41.8 million in FY2022 down to $31.0 million in FY2024 before surging to $57.17 million in FY2025 — an 84.6% increase year-over-year according to SEC XBRL data [F1]. Operating income remained negative but improved by nearly 20% from -$4.61 million in FY2023 to -$3.71 million in FY2024; operating income figures for FY2025 are not explicitly available but inferred improved cash flows suggest profitability progression.

The jump in operating cash flow to $69.7 million (a near doubling from $34.9 million the previous year) anchors this turnaround and supports growing equity base now exceeding $400 million (+13.1% YoY), facilitating greater lending capacity while maintaining regulatory capital buffers [F1]. Dividends paid increased robustly as well (+38.3% YoY), complemented by a sevenfold increase in stock buybacks totaling $11.73 million—underscoring management confidence.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 57 | 70 | +84.6% | |

| 2024 | 31 | 35 | -4 | -13.7% |

| 2023 | 36 | 47 | -5 | -14.2% |

| 2022 | 42 | 51 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | 12 | 14.2 |

| 2024 | 5 | 1 | 8.7 |

| 2023 | 4 | 9 | 14.1 |

| 2022 | 3 | 18.7 |

Source: SEC companyfacts cache [F1].

Table: Summary of Capital Bancorp Annual Financial Results (FY2022-FY2025) drawn from official filings [F1]

How Washington’s Economy Shapes Capital Bancorp’s Core Business

Capital Bancorp’s geographic moat is anchored by strong ties to the Washington, D.C., and Baltimore metropolitan areas where federal employees and government contractors dominate the economic landscape [S7][S17][S25]. This concentration creates unique opportunities and risks that critically affect borrowing demand, repayment ability, deposit inflows, and asset quality.

Federal government workforce reductions, debt ceiling debates leading to shutdowns, furloughs without pay, or contract funding suspensions directly impact payroll-dependent borrowers and their businesses servicing government contracts [S1][S2]. These disruptions can cause increases in loan delinquencies and nonperforming assets within their commercial real estate loans — a large portfolio segment given local demand for CRE financing for office space and government-related facilities development [S7][S12][S25].

Furthermore, fluctuations in government spending ripples through the broader regional economy affecting retail businesses supported by federal workers’ wages as well as housing demand — both important drivers for mortgage banking operations at Capital Bancorp [S2]. This sensitivity leads to elevated borrower repayment risk during protracted shutdowns or workforce downsizing.

Government-Backed Lending as a Differentiator in Growth Prospects

A cornerstone of Capital Bancorp’s competitive positioning lies in its SBA Preferred Lender status which permits streamlined approval authority on Small Business Administration guaranteed loans without requiring direct SBA intervention for each application—a competitive advantage accelerating loan origination cycles relative to non-preferred lenders [S26].

However, persistent federal budget impasses have induced processing backlogs at both SBA and USDA agencies that retard new loan volume resumption post-shutdowns and complicate servicing timelines for existing guaranteed loans originated via Windsor Advantage™, Capital Bancorp's lending service platform [S2][S3]. These backlogs represent tangible growth constraints with extended underwriting timelines diminishing refinancing activities and dampening expected fee income.

Despite these headwinds, government-backed lending programs mitigate credit risk through guarantees supporting asset quality stability even when collateral values fluctuate amid CRE market cyclicality [S26]. Maintaining status as an approved SBA Preferred Lender remains critical; any loss could materially impair origination volumes and customer retention.

Leadership Transition and Its Strategic Implications

Recent executive developments include new CEO employment agreements at the holding company level along with appointment of a CEO for the subsidiary bank entity itself indicating deliberate succession planning aimed at sustaining strategic execution within core markets amid evolving external pressures .

While specific filings do not delve deeply into leadership profiles or initiatives beyond overview references, these changes point toward management continuity focusing on capital deployment discipline and risk mitigation aligned with the firm’s regional relationship banking ethos.

Regulatory Challenges and Risk Management in a Concentrated Market

Capital Bancorp confronts substantial regulatory scrutiny typical for banks with pronounced concentrations in commercial real estate (CRE), infrastructure heavily leveraged on local government contractor economies, and sizable uninsured deposit levels that amplify liquidity oversight requirements.

Regulatory agencies consider construction loans constituting ≥100% of bank capital—and non-owner occupied CRE loans exceeding roughly ≥300% capital—as triggers mandating enhanced capital cushions above minimum thresholds [S20][S26]. At December 31, 2025, Capital Bank's ratios exceeded these guidelines with construction-to-capital at approximately 100% and CRE including construction at over 302%, necessitating heightened risk monitoring practices and potentially constraining leverage expansion strategies.

Liquidity management faces challenges due to approximately 40.9% of deposits being uninsured as of year-end—heightening exposure to volatile withdrawal dynamics especially amid digital platforms facilitating rapid fund movements during stress events like high-profile bank failures seen earlier in the decade [S1][S17][S22][S24]. Regulatory powers include enforcement against unsafe or unsound practices imposing corrective actions that could impact growth or capital plans if compliance or asset quality deteriorate substantially [S5].

Capital Allocation: Buybacks, Dividends, and Return on Equity Trends

Reflecting increased earnings strength, Capital Bancorp has amplified shareholder returns with dividends rising over +38% YoY paid out amounting to $7.3 million in FY2025 while concurrently executing robust share repurchases totaling $11.73 million—an escalation from prior years marking a nearly eightfold jump from FY2024's activity level ($1.4 million) [F1][S14].

The freshly authorized $15 million stock repurchase program active through December 31, 2026 enables flexibility for opportunistic capital deployment tied closely to market conditions—a signal of confidence in intrinsic business value generation capacity despite external uncertainties.[S14]

Estimated return on equity based on net income versus shareholders’ equity stands around a healthy approximate rate of roughly 14.2%, evidencing effective use of equity capital post-profit rebound amid elevated risk environment typical for regionally concentrated lenders engaging heavily with CRE loans requiring keen risk calibration.[F1]

What to Watch: Backlogs, Deposit Stability, and SBA Program Dynamics

Forward-looking operational drivers imperative for attention include resolution speed of SBA/USDA loan application backlogs which influence originations pipeline replenishment; borrower repayment behavior tied closely to continuation or cessation of government shutdowns impacting liquidity among federal employees; deposit base stability particularly managing uninsured portions sensitive to market sentiments around regional bank resilience; alongside tracking changes impacting CRE portfolio credit quality driven by local economic conditions.[Analysis based on S2/S3 commentary]

A key monitoring vector is management’s ability to remediate identified material weaknesses in internal controls over financial reporting—a process underway but still carrying execution risk influencing investor perceptions and regulatory scrutiny.[S13]

Continued vigilance around cybersecurity defenses remains critical given established vulnerabilities presenting operational risks that could disrupt services or result in reputational damage.[S8][S19]

This analysis compiles publicly filed financial data alongside regulatory disclosures without offering investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments