reAlpha Tech Corp. Leaps Toward Integrated AI Homebuying Amid Substantial Losses

reAlpha rapidly scaled revenues with AI-driven vertical integration in homebuying services but continues to face persistent losses and capital intensity.

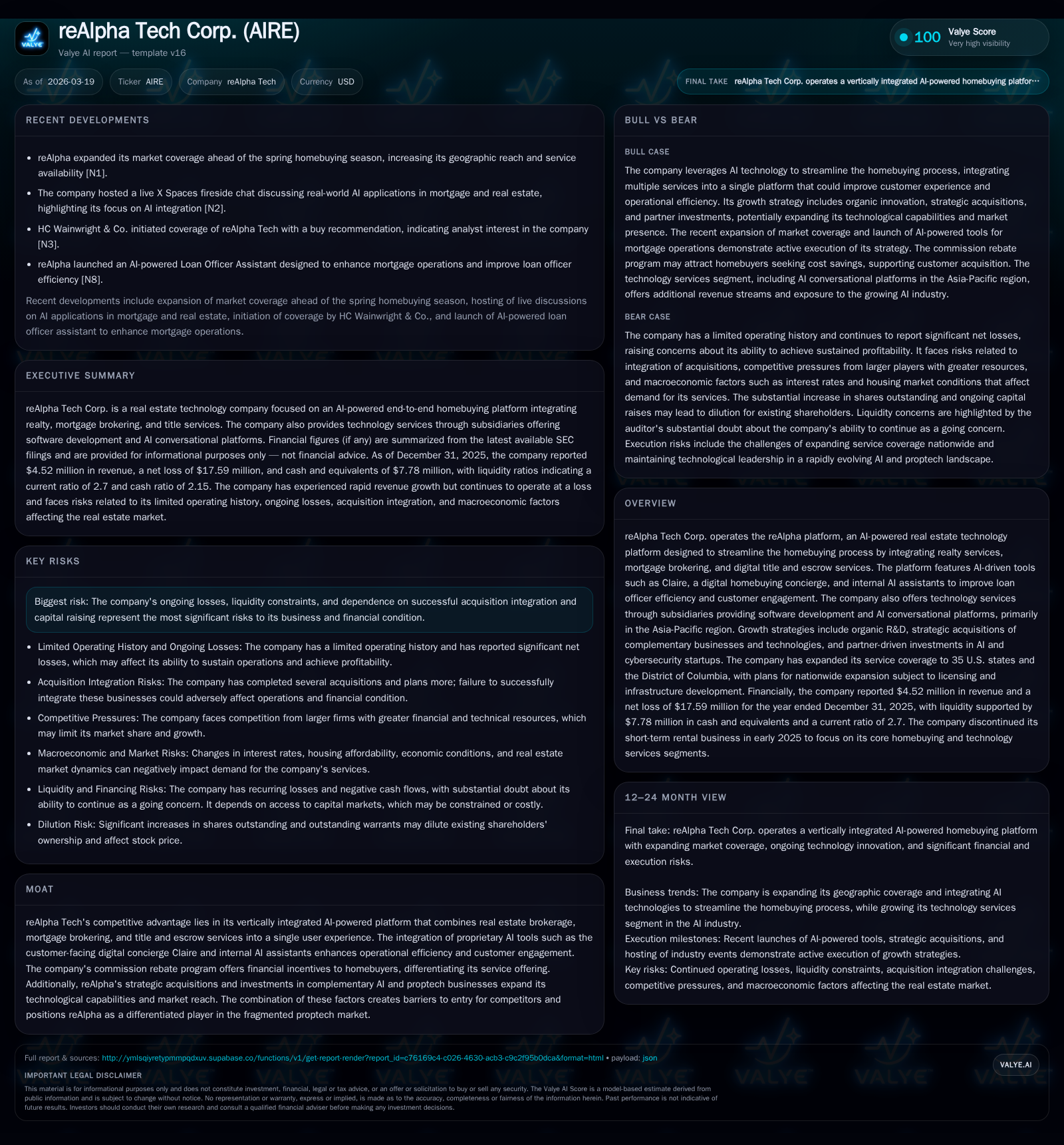

reAlpha Tech achieved a significant revenue increase from $121K in FY2023 to $4.52M in FY2025 by expanding its AI-powered integrated platform combining real estate brokerage, mortgage brokering, and title/escrow services. The company leverages proprietary AI tools like Claire — a digital concierge — to enhance customer experience and internal efficiencies. Despite rapid top-line growth, reAlpha incurs substantial operating losses and negative cash flows due to ongoing investments, acquisition-related costs, and scaling challenges, resulting in negative returns on equity. The firm’s aggressive acquisition strategy and licensing expansion plans are key inflection points amid regulatory and operational risks. Capital raising remains essential to sustain growth.

Strong Revenue Acceleration Driven by Platform Expansion and Acquisitions

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -18 | -11 | -16 | +376.4% | +32.4% |

| 2024 | 1 | -26 | -6 | -7 | +679.4% | -1979.0% |

| 2023 | 0 | -1 | -3 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -153.1 |

| 2024 | -1668.1 |

| 2023 | -5.1 |

Source: SEC companyfacts cache [F1].

Over the past three years, reAlpha Tech Corp. has demonstrated explosive revenue growth as it transitioned toward its integrated AI-powered real estate platform model. Annual revenue surged from $121K in FY2023 to nearly $4.52M by FY2025 — a compound increase driven by expanding homebuying service offerings and key acquisitions across mortgage brokering, title/escrow services, and related technology subsidiaries [F1][S1][S13]. The latest fiscal year alone showed revenue growth of over 376% year-over-year.

This acceleration aligns with expanded user-centric features such as Claire — an AI-based digital homebuying concierge — enhancing property search personalization and buyer support through a seamless web/iOS interface [S5][S26]. Supporting services like mortgage brokering (via reAlpha Mortgage) and digital escrow (through Hyperfast Title) have complemented core real estate brokerage capabilities.

AI-Enabled Vertical Integration Fuels Competitive Differentiation

reAlpha’s competitive advantage lies in its vertically integrated platform combining realty brokerage licenses (13 states plus D.C.), mortgage brokering licenses (31 states), and title agency licenses (3 states) into one unified journey enhanced by proprietary AI technology [S5][S26]. This model provides an end-to-end experience allowing customers to search homes, secure financing via brokerage or potential direct lending (pending InstaMortgage acquisition), and close with digital title/escrow services without leaving the platform.

Notably, 'Claire' operates as a 24/7 customer-facing assistant powered by advanced language models delivering personalized guidance through every homebuying stage. Complementing this is the internal AI "Loan Officer Assistant" designed to improve back-office productivity by automating underwriting reviews and engagement processes [S5][S26]. Additionally, reAlpha offers commission rebates up to 1% of the home purchase price as closing cost credits—reflecting consumer demand for pricing transparency following National Association of Realtors® settlement reforms [S17].

Acquisition Strategy and Challenges in Scaling Operations

The company pursues inorganic growth via strategic acquisitions focusing on complementary revenue-generating entities within services (mortgage brokering, title insurance lookup, escrow settlements) and products (AI-driven proptech solutions) aligned closely with its platform vision [S4][F1]. Recent acquisitions include reAlpha Nepal (technology & software development), AiChat (AI conversational platforms servicing APAC markets), Hyperfast Title LLC, Debt Does Deals LLC (rebranded reAlpha Mortgage), Prevu Inc., alongside the proposed merger with InstaMortgage aimed at embedding direct lending capabilities.

However, integration risks persist: notably the GTG Financial acquisition completed early 2025 was rescinded later that year due to issues impacting consolidation plans—highlighting operational challenges inherent in merging diverse service entities into a unified platform architecture [S1]. Successfully integrating InstaMortgage will be critical for scaling mortgage origination fees beyond brokerage commissions.

Licensing Footprint and Geographic Expansion Plans

ReAlpha currently holds mortgage brokerage licenses valid across 31 U.S. states with active real estate brokerage licenses covering 13 states plus Washington D.C., as well as title agency licensure spanning three jurisdictions [S5][S20]. Such licensing is foundational yet complex due to state-level regulatory controls governing broker activities including capital adequacy minimums for title agencies or controlled business statutes limiting referral volumes.

The company plans phased national expansion contingent upon securing licensing approvals particularly for bundled service regions where all three functions operate simultaneously—a key enabler for maximizing the integrated user journey effect. Regulatory compliance overheads thus represent both an operational barrier and a protective moat against low-cost competition.

Financial Performance: Operating Losses Despite Revenue Growth

A stark contrast emerges when evaluating profitability versus top-line gains. While revenues soared approximately thirty-seven fold between FY2023 ($121K) and FY2025 ($4.52M), operating losses widened from about -$6.3M to nearly -$16M over the same period [F1]. Net losses deepened from just over -$1.25M in FY23 to -$17.6M by FY25 reflecting scale expenditures.

This disconnect stems primarily from heavy investments into R&D for AI development (Claire enhancements), expanding operational capacity across acquisitions along with elevated SG&A costs underpinning geographically dispersed servicing infrastructure [F1][S4]. Return on equity stands deeply negative at roughly -153%, highlighting persistent shareholder dilution pressure amid significant cash outflows.

Capital Structure, Liquidity, and Cash Flow Dynamics

At fiscal year-end 2025, reAlpha reported cash & equivalents totaling approximately $7.8M alongside current assets near $9.8M supporting a current ratio close to 2.7x—a buffer sufficient for short-term obligations [F1][S11]. Nevertheless operating cash flow remains firmly negative at -$11.3M owing largely to escalating expenses tied mainly to platform improvements and acquisition costs forcing reliance on external financing.

Capital strategy involves issuing equity securities given sub-$75 million public float triggering “baby shelf” limitations—and targeted debt incurrence subject to favorable terms [S11]. There have been no dividends or share repurchases recently reflecting retention of capital toward growth initiatives rather than shareholder returns [S17]. Ongoing access to capital markets under reasonable terms remains critical given substantial acquisition ambitions.

Risk Factors: Regulatory, Litigation, and Integration Complexity Risks

Key risks include:

- Operating losses with high burn rates placing liquidity under pressure absent successful financing rounds or profitable scaling ventures [S1].

- Compliance challenges amid evolving privacy/data protection laws across multiple jurisdictions including U.S., EU member states, Singapore, India where subsidiaries operate [S6][S7][S19].

- Litigation involving CEO Giri Devanur related to historic allegations from prior roles contested vigorously but potentially impacting reputation or resources if extended unfavorably [S6].

- Operational risk from failed acquisition integrations exemplified by rescinded GTG Financial deal illustrating potential pitfalls affecting financial results or synergy realization [S1][F1].

- State-level regulatory licensing complexity restricting rapid nationwide rollout requiring patient phased approvals posing timing uncertainty for growth plans [S23].

- Dependency on third-party MLS data providers exposes operations to external policy changes potentially limiting data access needed for accurate listings feeding AI components [S8].

- Intellectual property infringement risks linked with software use notwithstanding legal protections around proprietary codebase elements [S18][S24].

Future Growth Constraints and Innovation Outlook

Licensing challenges gate full-stack service availability as broader state approvals are needed before seamless multi-service bundling can scale nationally impacting customer conversion economics outside core fully served regions like Florida or Virginia.

Competition intensifies from national real estate technology incumbents such as Opendoor or Zillow offering overlapping digital brokerage/mortgage ecosystems alongside emerging startups leveraging ‘super app’ strategies prevalent especially in Asia-Pacific markets where AiChat subsidiary competes leveraging popular messaging apps integration but faces entrenched local players requiring continuous innovation investment [S10][S13].

To stay ahead technologically reAlpha pursues organic R&D internally complemented by strategic minority investments into cutting-edge AI startups focused on cybersecurity or conversational capabilities that can enhance scalability of customer interactions beyond initial sales funnel stages reflecting partner-driven innovation approach detailed in filings ([S4],[S21]). However integrating complex AI systems reliably under real-world loads poses execution risk.

What Investors Should Monitor Next

Investors should watch:

- Progress toward closing the InstaMortgage acquisition enabling transition from brokered referrals toward direct origination capturing higher fees if smoothly integrated ([S1]).

- Expansion of licensed service footprints achieving simultaneous licensure across all core domains enabling full vertical bundle nationwide ([S20]).

- Operational metrics like loan officer efficiency improvements driven by internal AI assistants coupled with customer engagement metrics via Claire offering signals on technology impact ([S5],[S26]).

- Cash runway sustainability given ongoing net losses requiring monitoring capital raises alongside disciplined expense management balancing growth ambitions ([F1],[S11]).

- Regulatory developments relating specifically to MLS data sharing policies or new privacy regimes around consumer data used within generative AI models affecting service functionality or compliance costs ([S8],[S19]).

DISCLAIMER: This report is prepared solely for informational purposes based on publicly available SEC filings and company disclosures as of March 19, 2026. It does not constitute investment advice or recommendations regarding buying or selling securities of reAlpha Tech Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments