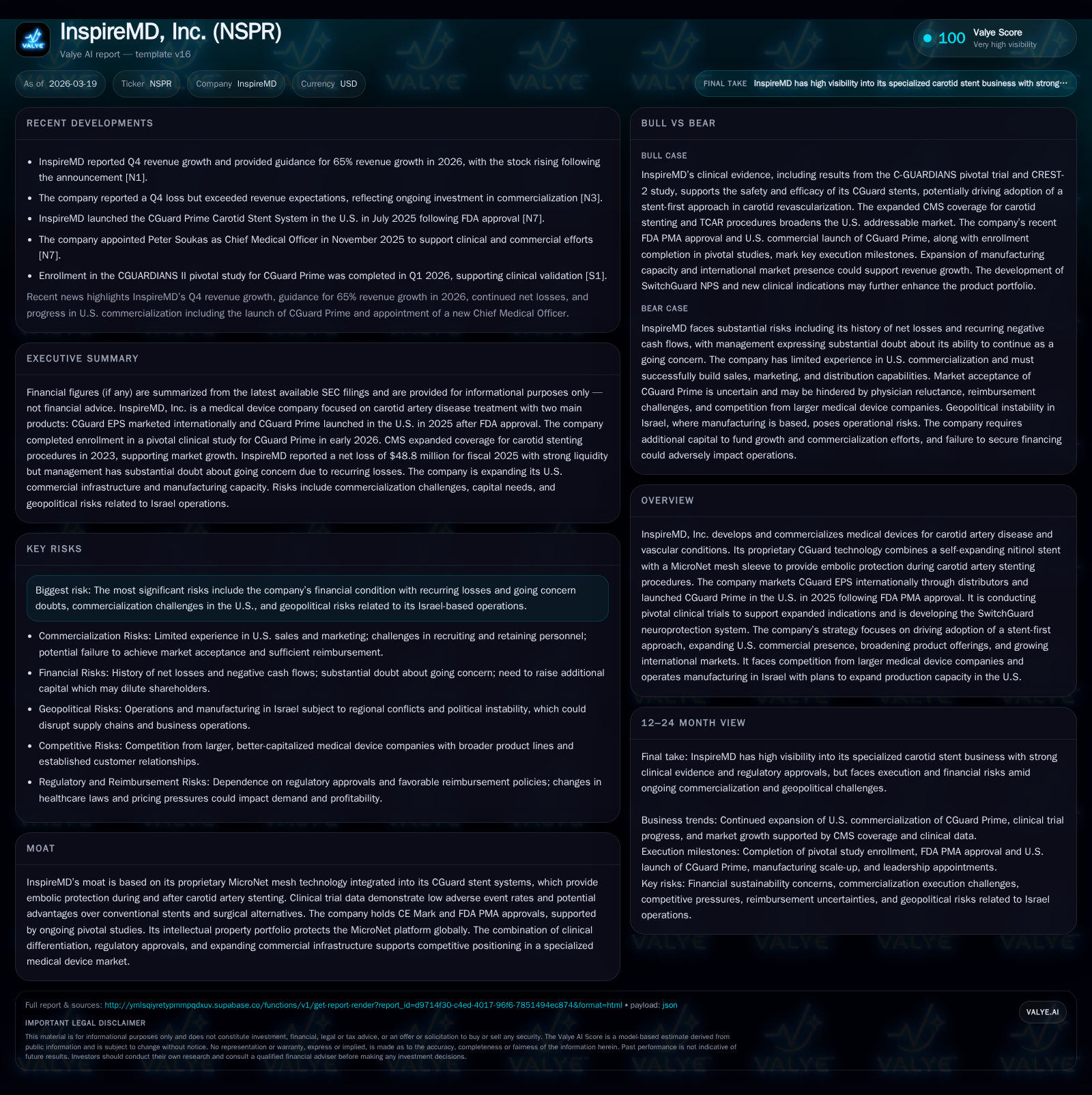

InspireMD’s Stent Technology Drives Reward and Risk in Post-Approval Expansion

InspireMD advances its proprietary embolic protection stent into U.S. markets amid enduring financial pressures and strategic growth initiatives.

InspireMD, Inc. has transitioned from clinical development to commercial launch with its innovative CGuard Prime carotid stent system, leveraging FDA premarket approval achieved in mid-2025. Despite promising regulatory milestones and expanding U.S. market coverage propelled by favorable clinical data, the company faces significant challenges including steep operating losses, considerable negative cash flows, and capital constraints underscored by going concern disclosures. Internationally, InspireMD maintains a distributor-based model while building its U.S. direct sales infrastructure and planning manufacturing capacity expansion. Intellectual property protections around the MicroNet mesh platform underpin competitive differentiation but legal and regulatory risks remain material. Key near-term developments to monitor include pivotal trial readouts, sales ramp metrics, reimbursement evolution, and production scale-up dynamics.

From Clinical Innovation to Market Launch: Historical Revenue and Loss Trends

InspireMD's trajectory from a development-stage firm into a commercial entity spotlights the growing pains typical of specialized medtech firms scaling novel technologies. The company’s revenues have declined at an average annual rate of about 18% over the past three fiscal years leading to a reported $2.31 million in revenue for FY2015 [F1]. This downward trend reflects the lag between product approvals and meaningful commercial uptake as well as competitive pressures within the carotid artery stenting (CAS) domain.

Concurrently, operating losses expanded sharply by approximately 48% year-over-year to nearly $49.6 million in FY2025 [F1]. Net losses followed suit with a $48.8 million deficit in the same year indicating that operational expenses scale faster than nascent revenue inflows—largely driven by investments into U.S. commercialization infrastructure, R&D for new indications, and manufacturing capability build-out. Operating cash flows remain deeply negative ($35.1 million deficit), accentuated by capital expenditure increases coinciding with facility enhancement efforts [F1]. This dynamic underscores the arduous path from FDA approval to achieving stable profitability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -49 | -35 | -50 | 1662000 | -52.4% |

| 2024 | -32 | -22 | -34 | 1402000 | -60.7% |

| 2023 | -20 | -16 | -21 | 381000 | -7.7% |

| 2022 | -18 | -16 | -19 | 473000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -37 | -88.4 |

| 2024 | -23 | -88.7 |

| 2023 | -17 | -50.4 |

| 2022 | -16 | -106.3 |

Source: SEC companyfacts cache [F1].

Note: Figures for operating income and net income are from fiscal years ending December; revenue trends show contraction despite product launches.

CGuard Platform's Differentiation: Technical Edge & Regulatory Milestones

At InspireMD’s core lies the proprietary MicroNet mesh technology embedded within the CGuard stent platforms—a self-expanding nitinol scaffold coupled with a fine-mesh sleeve designed to trap embolic debris during CAS procedures [S1]. Nitinol’s superelastic properties enable reliable deployment conforming to vessel architecture while maintaining luminal patency.

This dual-layer design addresses one of CAS’s critical procedural risks: embolization leading to perioperative stroke events. By physically containing plaque fragments that might otherwise embolize downstream during balloon angioplasty or stent placement—and potentially afterwards due to plaque prolapse—the MicroNet platform proposes a clinically meaningful safety advantage over conventional bare metal or drug-eluting stents.

The company's CGuard EPS received CE Mark certification initially under MDD and was recertified under MDR in early 2024; more significantly for U.S.-centric growth ambitions is CGuard Prime's FDA Premarket Approval secured on June 23rd, 2025 [S1]. This PMA status followed rigorous preclinical data submissions and is supported by ongoing IDE-compliant pivotal studies such as CGUARDIANS II focusing on applications including transcarotid artery revascularization (TCAR) [S1], [S2].

The differentiation extends beyond materials science: CGuard Prime introduces refinements in delivery mechanisms facilitating ease of implantation—an important factor impacting physician preference in complex neurovascular interventions.

Expanding U.S. Market Opportunity: Impact of Coverage and Clinical Data

U.S. reimbursement dynamics have been pivotal for InspireMD’s planned revenue trajectory. October 2023 witnessed a landmark CMS National Coverage Determination (NCD) publication that expanded Medicare coverage for CAS—including TCAR procedures—to encompass asymptomatic as well as standard risk patient populations [S1]. This effectively widened the size of the addressable market within the U.S., bridging prior gaps where stenting was largely confined to high-risk or symptomatic cases.

Complementing this policy advancement was the November 2025 release of CREST-2 study results sponsored by NIH—demonstrating statistically significant stroke risk reduction when CAS was employed alongside optimized medical therapy relative to medical therapy alone for patients harboring severe asymptomatic carotid stenosis [N1], [S1]. Notably carotid endarterectomy (CEA), traditionally considered an alternative therapeutic modality in such cohorts did not show similar benefit.

These data carry strategic import: they validate clinical rationale for expanded device adoption beyond symptomatic indications—potentially accelerating uptake momentum particularly when combined with CMS coverage assurances.

Despite these tailwinds however inherent procedural volumes remain dependent on physicians’ shift toward minimally invasive interventions over surgery—a transition requiring sustained education efforts which InspireMD must manage through its fledgling U.S. sales force.

Commercial Infrastructure Build-out and International Growth Strategy

With FDA PMA clearance fueling the go-to-market launch of CGuard Prime in July 2025 [S2], InspireMD embarked on constructing a foundational commercial infrastructure headquartered in Miami [S2]. Building a direct sales organization anew poses operational challenges given prior reliance on distributor partnerships internationally.

International distribution still accounts for sales across more than thirty countries utilizing established third-party channels that manage local regulatory compliance and logistics—a practical approach given varying market access requirements globally [S1].

Manufacturing operations remain primarily based in Israel but plans exist for scaling capacity stateside consistent with anticipated demand growth post-FDA approval [S1]. This manufacturing expansion seeks to mitigate supply chain complexities while aligning production closer to key U.S. markets.

Scaling commercial capabilities will necessitate recruiting experienced vascular device sales personnel adept at articulating nuanced MicroNet benefits vis-à-vis entrenched alternatives—a demanding task compounded by fast-evolving competitive landscapes typified by large incumbents employing bundled product-service offerings.

Financial Health Under Pressure: Persistent Losses, Liquidity Risks, and Capital Needs

Despite tangible regulatory validation and initial revenue generation efforts,[F1],[N1],[S1] InspireMD’s financials remain strained with an operating loss near $49.6 million accompanied by net losses approximating $48.8 million in FY2025 [F1]. These deficits exhibit steepening trajectories compared with prior years’ figures reflecting accelerated expenditure on marketing infrastructure buildup and manufacturing scale-up.

Operating cash flow remains significantly negative at $35.1 million alongside incremental capital expenditures around $1.66 million [F1], highlighting ongoing free cash flow deficits exceeding $36 million annually—an unsustainable condition without fresh capital inflows or marked revenue acceleration.

Liquidity concerns are acute as management explicitly acknowledged substantial doubts regarding continuing as a going concern within most recent SEC filings due to recurring losses coupled with financing uncertainties [S2], [S19]. While recent warrant exercises injected some proceeds ($17.9 million net mid-2024), additional funding rounds will likely be prerequisite given projected capital requirements encompassing commercialization expansion plus ongoing R&D commitments such as SwitchGuard development.

This tenuous financial footing may elevate cost of capital premiums or dilute existing shareholders through equity issuance—critical factors to monitor amid competitive pressures constraining pricing power and reimbursement landscapes that could compress future margins further.

Governance of Intellectual Property and Legal Risk Landscape

InspireMD holds an extensive intellectual property portfolio centered on its MicroNet mesh technology deployed globally providing defensive moats against generic replication or direct competitor infringement attempts . However patent enforcement challenges arise from numerous incumbent competitors controlling overlapping stent-related patents covering materials composition nuances, delivery mechanisms including rapid exchange systems, and drug-eluting adjuncts prevalent across vascular interventions .

Past litigation activity within neurovascular device segments has been frequent among major players such as Boston Scientific and Medtronic raising inference about potential future contentious IP disputes facing smaller rivals like InspireMD [S7],[S8]. Such legal battles can consume managerial bandwidth while imposing unpredictable financial burdens ranging from damages awards to costly redesign mandates or injunctions against sale of infringing products.

Regulatory compliance risks persist including adherence to FDA IDE conditions governing pivotal studies; failure here could delay approvals or trigger enforcement actions with material adverse outcomes [S1],[S6],[S15]. Vigilant monitoring of adverse event reporting under Medical Device Reporting (MDR) regulations and proactive quality control measures are essential mitigants against reputational damage via recalls or safety alerts which historically have impacted medical device manufacturers disproportionately when operating near critical anatomical regions like carotid arteries supplying brain tissue [S6],[S23].

Additionally exposure exists under myriad healthcare laws targeting anti-kickback statutes, fraudulent claims acts, and physician payment transparency requirements constraining promotion practices particularly salient given nascent U.S. commercial footprint expansions where accidental non-compliance risks increase due to evolving organizational processes [S16],[S20].

Near-Term Catalysts and What Investors Should Monitor

Looking ahead several key milestones stand poised to impact InspireMD’s operational momentum:

- Completion of enrollment in CGUARDIANS II pivotal IDE study early Q1 FY2026 provides critical dataset underpinning potential PMA supplements addressing expanded indications including TCAR uses aligning with procedural innovations preferred by interventionalists [S1],

- Development progress on SwitchGuard neuroprotection system represents a strategic diversification leveraging existing technology know-how targeting neurovascular embolic protection beyond carotid arteries expanding total addressable markets if successful,

- Early adoption rates tracked through third-quarter/annual sales results offer vital signals regarding U.S. deployments' success relative to competitor offerings requiring close scrutiny given limited historical references,

- Manufacturing scale-up progression especially anticipated moves toward U.S.-based production facilities affecting cost structures,

- Reimbursement environment shifts either through CMS policy refinements or private payer decisions which directly influence procedure volumes incentivization schemes.

All aforementioned factors constitute forward-looking elements contingent on execution capabilities alongside external healthcare environment influences necessitating contextual vigilance rather than prognostication beyond disclosed management guidance indicating expected revenue growth acceleration post-commercial launch phases[N1].

Capital Deployment: Assessing ROI, Cash Flow Trends, and Shareholder Returns

Capital allocation historically emphasizes reinvestment into R&D pipelines alongside building requisite commercial platforms required for sustainable positioning within complex carotid intervention markets [F1]. Modest capital expenditures reported ($~1.66 million FY25) reflect focus on manufacturing site enhancements supporting projected demand ramp-ups rather than substantial physical asset accumulation [F1].

Meanwhile operating free cash flows remain deep negative territory underscoring intense burn rates driven predominantly by payroll expansion within sales/marketing teams and expanded clinical trial activities aimed at label broadening hurdles typical for PMA-stage medtech organizations transitioning from concept validation toward scale commercialization.

No dividends or stock repurchases have been pursued consistent with early lifecycle investment prioritization balancing tight liquidity scenarios signaled through recent going concern rhetoric thereby limiting shareholder returns strictly to latent equity value appreciation dependent on eventual profitability pathways [F1].

Approximated return on equity based on trailing net loss relative to equity levels stands near -88%, exemplifying currently weak capital efficiency metrics reflective primarily of elevated R&D expenditure phases paired with nascent revenue inflows inadequate yet to offset fixed costs burden.

Strategic emphasis thus tilts heavily toward sustaining adequate capital runway allowing product adoption cadence maturation necessary before recalibration toward value extraction becomes feasible.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments