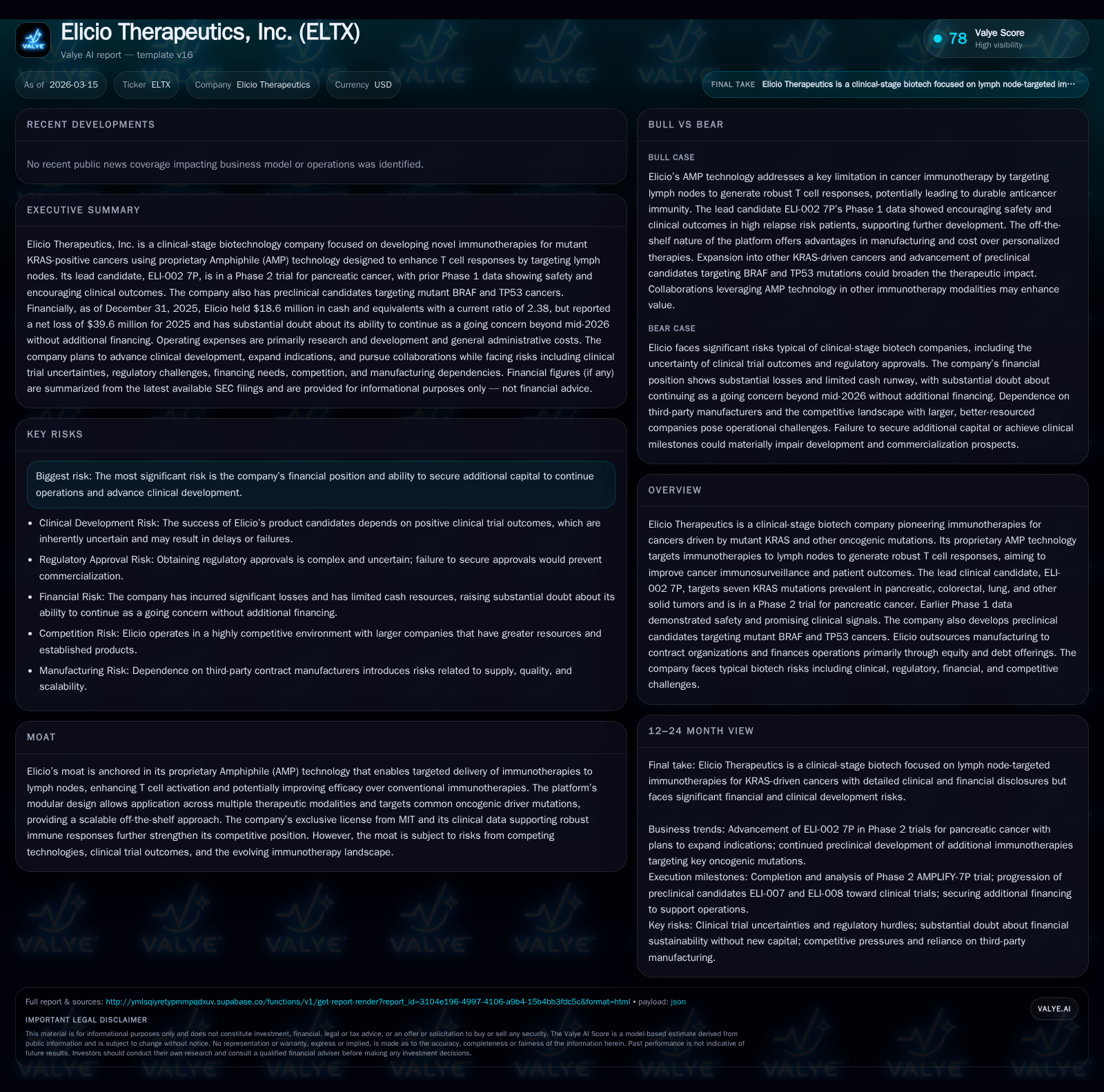

Elicio Therapeutics Advances AMP-Driven Immunotherapy Amid Financial and Clinical Milestones

Elicio Therapeutics progresses its proprietary lymph node-targeted AMP platform with key upcoming clinical readouts, balancing innovation with capital challenges.

Elicio Therapeutics, a clinical-stage biotech focused on immunotherapies for mutant KRAS-driven cancers using its proprietary Amphiphile (AMP) technology, is advancing its lead candidate ELI-002 7P in pancreatic cancer with an anticipated pivotal disease-free survival analysis in H1 2026. The company’s off-the-shelf approach targets lymph nodes to elicit robust T cell responses, potentially overcoming limitations of conventional immunotherapies. Despite promising early clinical data and a diversified preclinical pipeline targeting BRAF and TP53 mutations, ELTX faces significant operating losses and liquidity constraints. The firm relies on capital raises to sustain operations and fund clinical development. Investors should monitor upcoming trial data and financing developments as critical factors shaping ELTX’s outlook.

Historical Financial Performance and Growth Context

Elicio Therapeutics operates as a clinical-stage biotech focused on immunotherapies for mKRAS-driven cancers including pancreatic ductal adenocarcinoma (PDAC), colorectal cancer (CRC), and lung cancer. Over recent fiscal years through December 31, 2025, reported revenues declined sharply from $28.3 million in FY2021 to $2.3 million in FY2022, reflecting a strategic shift toward research and development centered on the proprietary Amphiphile (AMP) platform [F1].

Operating losses have persisted but showed some improvement from -$44.99 million in FY2024 to -$37.71 million in FY2025 (+16.2%), underscoring sustained investment in clinical development despite limited near-term revenues [F1]. Net losses remained significant at -$39.57 million in FY2025.

Operating cash flows have consistently been negative around $37 million annually despite minimal capital expenditures ($16,000 in FY2025), indicating operational burn primarily driven by R&D expenses rather than fixed asset investments [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -40 | -37 | -38 | 16000 | +23.8% |

| 2024 | -52 | -37 | -45 | 87000 | -47.5% |

| 2023 | -35 | -33 | -36 | 66000 | +9.3% |

| 2022 | -39 | -38 | -40 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -37 | -2418.8 | |

| 2024 | 0 | -37 | 458.8 |

| 2023 | 150000 | -33 | -309.5 |

| 2022 | -38 | -88.7 |

Source: SEC companyfacts cache [F1].

Table: Selected Annual Financial Metrics for Elicio Therapeutics (FY2022-FY2025) [F1]

Proprietary AMP Technology and Clinical Pipeline

Elicio's AMP platform enables targeted delivery of immunotherapeutic agents to lymph nodes—the central hubs for initiating adaptive immune responses—thereby enhancing T cell activation beyond traditional systemic therapies [S1][S2]. The off-the-shelf design uses well-characterized neoantigens linked to oncogenic mutations such as KRAS variants prevalent in solid tumors.

ELI-002 7P is a multi-peptide formulation targeting seven KRAS mutations found in approximately 88% of PDAC patients [S1]. Early Phase 1 results from the AMPLIFY-201 study demonstrated median recurrence-free survival of 16.3 months and overall survival of approximately 28.9 months in high relapse-risk patients post-surgery and chemotherapy [S1], supporting the potential clinical benefit of AMP-mediated immune activation.

Phase 2 AMPLIFY-7P Trial Milestones

The ongoing Phase 2 AMPLIFY-7P trial evaluating ELI-002 in mKRAS-driven PDAC has passed an interim review by an Independent Data Monitoring Committee (IDMC) which recommended continuation without modifications based on favorable safety and efficacy signals [S1][S2]. Final disease-free survival data are anticipated during the first half of 2026 and represent a critical inflection point for regulatory advancement and commercial evaluation [S1].

Expansion plans include exploring indications beyond PDAC into other mKRAS-positive solid tumors such as lung cancer contingent upon positive Phase 2 outcomes.

Preclinical Pipeline Expansion: ELI-007 and ELI-008

Building on AMP platform versatility demonstrated clinically with ELI-002 candidates, ELTX is progressing two preclinical programs targeting oncogenic drivers:

- ELI-007: Directed at mutant BRAF-driven cancers,

- ELI-008: Targeting mutated tumor protein p53 (TP53)-expressing malignancies.

Both candidates aim to leverage lymph node targeting for enhanced antigen-specific T cell responses [S1][S2], indicating strategic pipeline diversification.

Capital Structure and Liquidity Considerations

Since inception as Vedantra Pharmaceuticals Inc., Elicio has raised approximately $219.7 million through equity offerings including common stock sales, warrants exercises, convertible securities placements along with merger proceeds from Angion Biomedica Corp [S1][S9][F1]. These funds have primarily supported R&D activities reflected by substantial net losses totaling over $230 million accumulated deficit by end-FY25 [F1].

Cash and cash equivalents stood at approximately $18.6 million at year-end FY25 while shareholders' equity was marginally positive at $1.6 million after erosion from sustained losses [F1]. Operating cash flows remain negative near $37 million annually whereas capital expenditures are minimal reflecting outsourcing strategies rather than infrastructure investment [F1][S27].

There have been no recent share repurchases or dividend payments; capital raises have historically involved equity issuance or debt financings without returning cash to shareholders.

Risks: Clinical Uncertainty and Financing Needs

Key risk factors include:

- Clinical trial outcomes remain uncertain; adverse events or failure to meet endpoints could delay or halt development [S4][S6].

- Dependence on companion diagnostic collaborations necessary for patient selection may impact regulatory approval timelines [S4].

- Regulatory environment complexities including pricing reform under the Inflation Reduction Act may affect future reimbursement levels [S4][S12].

- Compliance with extensive healthcare laws governing marketing practices is essential to avoid penalties or reputational damage [S14][S15].

- Significant reliance on external financing exists given ongoing operating losses; inability to raise capital could force program curtailment or cessation [S9][S10].

- Competitive landscape includes alternative neoantigen platforms and cellular therapies that could challenge market positioning despite AMP advantages.

Outlook Summary

Elicio Therapeutics stands at a critical juncture balancing promising immunotherapy innovation against financial constraints typical of clinical-stage biotechs. The forthcoming final analysis from the AMPLIFY-7P Phase 2 trial will be a key catalyst informing regulatory strategy and investor sentiment amid ongoing funding requirements. Continued development of preclinical candidates targeting additional oncogenic drivers offers long-term pipeline growth potential but depends on successful capital acquisition.

This assessment synthesizes publicly available SEC filings up through March 2026 combined with reported financial data without speculative forecasting or investment advice but aims to provide a comprehensive view into ELTX’s operational status within oncology immunotherapy.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments