Eve Holding's Bold Leap from R&D to Urban Air Mobility Reality

Eve Holding leverages its strategic partnership with Embraer to transition from development-heavy operations toward commercial scaling in the emerging UAM sector.

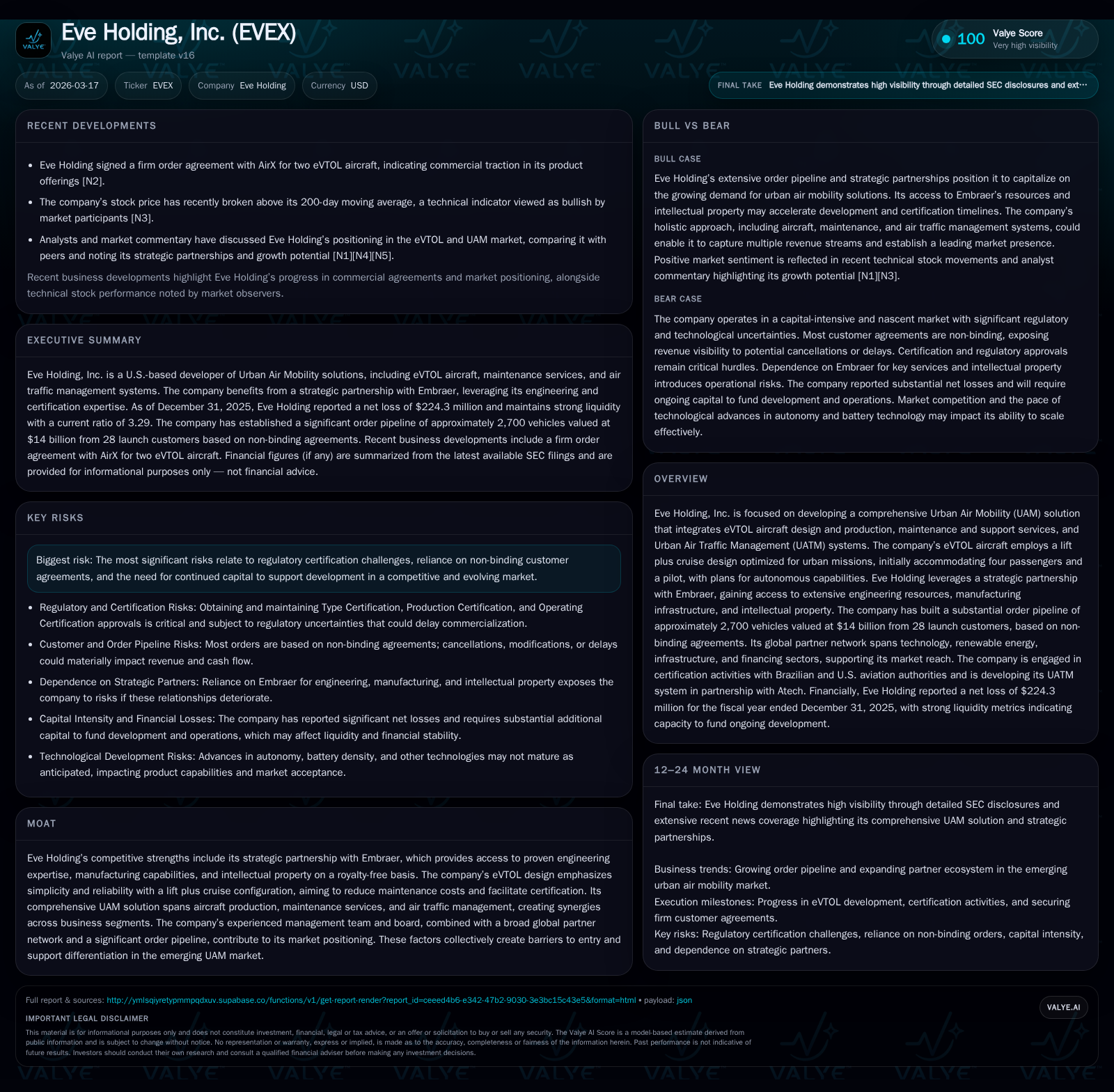

Eve Holding, Inc. is advancing its Urban Air Mobility ambitions by integrating eVTOL aircraft production, maintenance services, and air traffic management solutions supported by a significant order pipeline and the engineering prowess of Embraer. Despite steep operating losses and ongoing capital intensity reflective of the R&D phase, Eve’s access to royalty-free intellectual property and manufacturing resources underpins a competitive market positioning. The company’s financial profile shows increasing investment outlays and a strong liquidity cushion from multiple credit facilities, while certification complexities and reliance on non-binding customer orders pose near-term growth risks. Upcoming milestones include ramping pilot production and autonomous technology development that will be critical indicators of commercial viability.

Harnessing Growth: Eve’s Historical Financial Trends and Operational Drivers

Eve Holding remains in the early development stages of its urban air mobility (UAM) vision, reflected in widening operating losses alongside escalating capital investments. In fiscal year (FY) 2025, operating income deteriorated to a loss of approximately -$225 million, a sharp decline of roughly 44% compared to FY2024’s -$156 million loss. Net losses similarly deepened over 62% year-over-year to -$224 million [F1].

Operating cash flows remain negative at about -$160 million in 2025, worsening nearly 18% from the previous year. Meanwhile, capital expenditures increased dramatically by over 140% to $12.6 million in FY2025 as Eve intensified investment into expanding production capabilities and technology development [F1]. This spending pattern typifies the operational leverage dynamic common among early-stage UAM developers accelerating product certification and buildout before commercial revenue recognition.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -224 | -160 | -225 | 13 | -62.3% |

| 2024 | -138 | -136 | -156 | 5 | -8.2% |

| 2023 | -128 | -95 | -131 | 0 | +26.6% |

| 2022 | -174 | -59 | -189 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -173 | -181.2 |

| 2024 | -141 | -111.5 |

| 2023 | -95 | -77.3 |

| 2022 | -60 | -60.7 |

Source: SEC companyfacts cache [F1].

Table reflects steepening losses alongside rapid capex growth indicative of intensified R&D and production scale-up efforts.

Strategic Advantages in Product and Partnerships: The Embraer Effect

Eve's strategic alliance with Embraer provides a foundational competitive advantage uncommon among newcomers in the eVTOL space. Under multiple service agreements with Embraer (ERJ), Eve accesses approximately 5,000 employees including over 1,600 aeronautical engineers on a flexible basis at cost-based pricing [S10]. This arrangement includes royalty-free rights to Embraer's extensive background intellectual property portfolio—an invaluable asset in aerospace innovation [S25].

This collaborative leverage enables Eve’s lift plus cruise configured aircraft design—a balance of simplicity for easier certification and maintenance with sufficient performance for urban missions—to advance without reinventing tested aeronautical principles or committing to complex tilt-rotor mechanisms carrying higher certification risk [S25][S28]. Additionally, Eve benefits from Embraer-developed fly-by-wire flight systems married to proprietary human-machine interfaces enhancing safety and user experience.

Moreover, Embraer's legacy assets such as flight test infrastructure and manufacturing resources can be deployed without substantial upfront greenfield capital investment by Eve—critical given the capital intensity of aircraft development programs [S15]. This hybrid startup-incumbent model equips Eve to accelerate timelines for certification and deployment where pure startups often struggle.

Decoding Urban Air Mobility Market Entry: Order Pipeline and Customer Signals

Though active revenue generation is nascent due to the product being pre-commercial stage, Eve has constructed what it describes as the largest UAM order pipeline by volume: approximately 2,700 eVTOL units with an aggregate potential value near $14 billion stemming from engagements with 28 launch customers worldwide [S18][S22]. These include legacy fixed-wing operators such as United Airlines and Republic Airways; helicopter operators like Bristow Group; fleet lessors Azorra and Falko; plus innovative ride-sharing partners such as Flapper [S11].

Recent firm commitments include AirX’s signed purchase agreement for two eVTOL aircraft amplifying visibility into conversion beyond non-binding letters of intent (LOIs) or memoranda of understanding (MOUs) common in early aviation ventures but still contingent on final terms [N2]. Despite this encouraging pipeline breadth, nearly all orders remain non-binding typical within aerospace where regulatory milestones strongly influence procurement decisions.

This heavily front-loaded vehicle interest signals market anticipation but does not translate directly into near-term revenues or earnings until aircraft begin delivery post-certification; therefore it should be interpreted as a health indicator of demand rather than an assurance of proceeds .

Capital Structure and Liquidity Profile Underpinning Expansion Ambitions

As Eve accelerates its shift toward commercialization scale-up phases, liquidity management becomes paramount given sustained negative cash flow profiles. As of December 31, 2025, Eve held cash and equivalents totaling $103 million supported by current assets near $411 million against current liabilities of about $125 million—generating a strong current ratio around 3.29 times that attests to short-term payment ability [F1].

Further bolstering financial flexibility are multiple credit facilities aggregating over $150 million combined: notably a syndicated $150 million revolving credit facility arranged with prominent banks including Citibank NA guaranteeing funding through mid-decade to support supplier payments and prepayments essential to producing eVTOLs; also a $15.6 million Export-Import Bank backed facility detailed end-2025 directing financing toward relevant goods acquisition under favorable quarterly installment plans extending four-to-five years post drawdown date [S4][S5][S6][S7][S8].

The sophistication of this layered debt structure is complemented by equity cushions noted in shareholders’ equity near $124 million albeit down from prior levels due primarily to accumulated losses [F1]. Notably no dividends or stock buybacks have been declared given focus on reinvestment priorities amid heavy R&D spending phases.

Operating Losses, Cash Burn, and Investment Dynamics: A Closer Look

Eve’s widening losses are understood within the context of high upfront R&D spending driving an expected negative return on equity estimated near -181%. The company outlines deliberate strategy leveraging both organic talent augmented by flexible contractor expertise via Embraer along with selective potential acquisitions aiming to bolster ecosystem positioning while progressing towards scalable operations [F1][S9][S15][S16][S19].

Operating expenses incorporate rising selling general & administrative costs coupled with briskly growing research & development commitments identified as fundamental pillars enabling vehicle certification progressions under aviation authority scrutiny. Amid intense competition emerging within UAM globally—from well-funded incumbents to tech disruptors—the need for strict cost discipline must balance investment urgency.

No dividend policy exists nor share repurchase program reflecting prudent capital preservation during developmental maturity stage until consistent positive cash flows materialize inevitably lagging certification approvals and market entry.

Regulatory and Certification Challenges Shaping Growth Constraints

A pivotal hurdle constraining time-to-commerciality involves obtaining rigorous certifications mandated globally including primary Type Certification alongside Production Certifications crucial for scaled manufacturing authorization before deliveries occur [S25].

Certification complexity intensifies given novelty inherent in electric vertical take-off landings as regulators confront unprecedented standards encompassing safety redundancy validation across innovative lift plus cruise designs featuring eight independent rotors powered by redundant high-voltage battery paths ensuring failure tolerance during urban flights [S25][S28].

Eve’s favored strategy engaging Brazil’s ANAC—with recognized bilateral arrangements via FAA—aligned to Embraer’s long-standing regulatory experience ideally positions it amid relatively concentrated global certification gatekeepers who slow pace market rollout cycles industry-wide.

Governmental shifts potentially imposing additional restrictive mandates or increasing oversight could further delay timelines or elevate costs beyond internal projections compelling incremental contingency planning in operational forecasts.

Future Milestones and What Investors Should Watch Next

While explicit revenue or earnings guidance remains unavailable reflecting current developmental phase status, key value inflection points prospective observers may focus on range from successful completion of formal Type Certification tests through scaling prototype builds into early serial production batches.

Particularly notable is progress toward autonomous flight capabilities designed initially for up to six passengers allowing pilotless operation expansion envisaged within early next-decade horizons. Firm order contract finalizations surpassing existing non-binding LOIs alongside first large-scale deliveries constitute definitive market validation events ahead.

Financial health indicators tied closely to continued funding access—including utilization rates of credit lines—and progressively narrowing operating cash flow deficits will also factor substantively into longer-term sustainability narratives.

Finally, partnerships expanding both geographic reach into prominent urban centers globally as well as cross-sector alliances tapping emerging renewable energy charging infrastructure integrated within vertiport networks develop represent industry ecosystem maturation signals complementary to direct aircraft progress milestones.

This analysis is based solely on publicly available regulatory filings and reputable news sources as cited. It does not intend any investment advice or predictions but aims to provide a comprehensive overview rooted in verified data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments