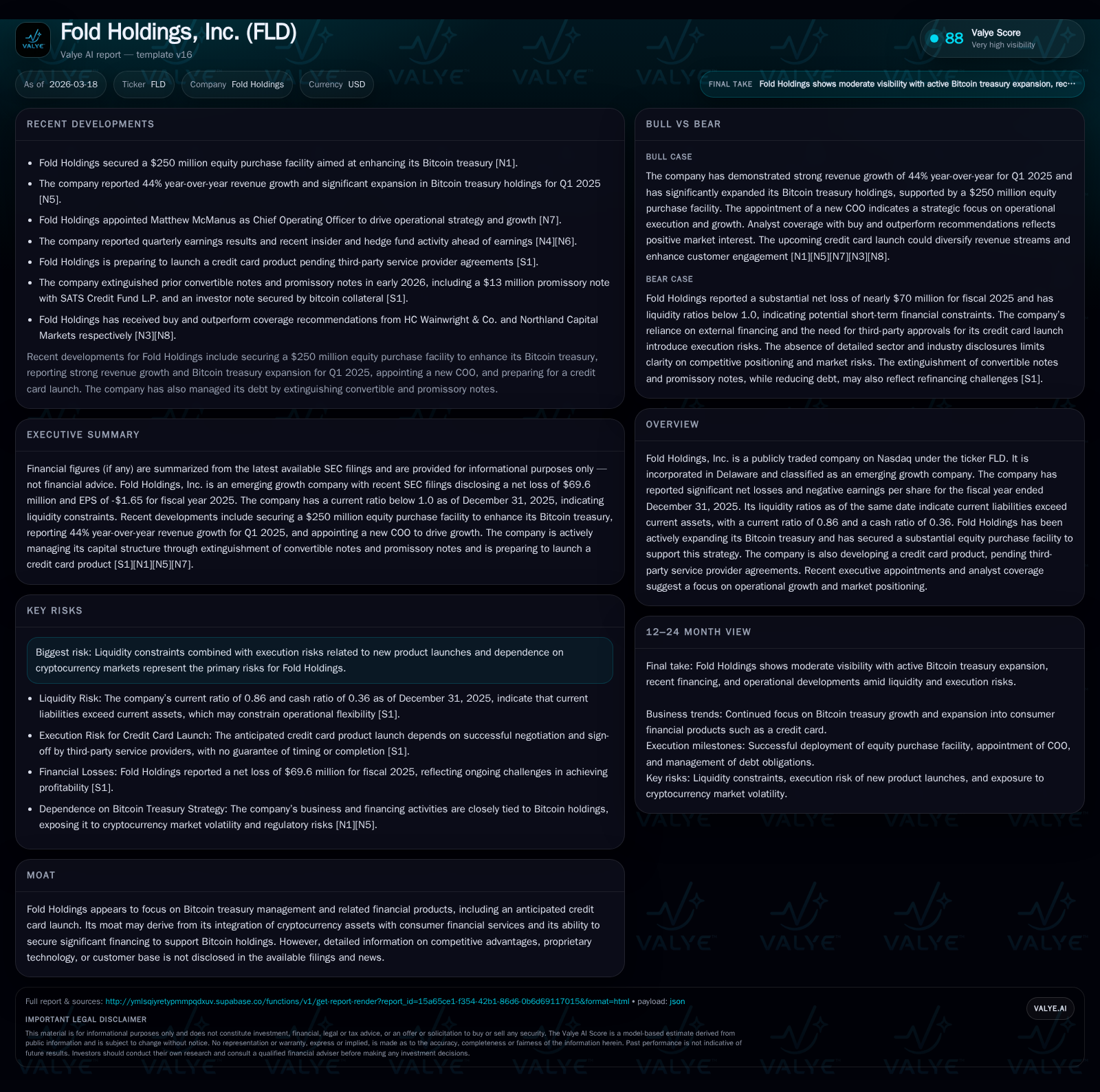

Fold Holdings’ Bitcoin Treasury Strategy and Credit Card Vision

Fold Holdings integrates bitcoin treasury management with consumer financial innovation despite significant losses and capital constraints.

Fold Holdings, Inc. pursues a distinctive strategy that marries a growing bitcoin corporate treasury with a suite of consumer financial products centered on bitcoin rewards. Founded in 2019 to facilitate everyday bitcoin use integrated with traditional finance, Fold has expanded its product offerings but faces steep operating losses and liquidity pressures. Its upcoming bitcoin rewards credit card represents a pivotal growth initiative hinging on critical third-party agreements. Capital structure revisions including a higher-cost loan and equity-backed promissory note support ongoing operations but introduce refinancing risk. Monitoring execution on the new credit card, bitcoin price triggers affecting debt repayments, and regulatory developments will be essential in assessing Fold's trajectory.

Evolution of Fold’s Business Model and Historical Results

Founded in 2019, Fold Holdings set out to create a seamless financial platform that integrates bitcoin into everyday consumer financial activity. The company’s vision centers around enabling customers to accumulate, save, and utilize bitcoin alongside traditional U.S. dollar financial products. Its offerings have expanded beyond early-stage bitcoin reward programs to include FDIC-insured checking accounts, prepaid Visa debit cards, bill payment services, and notably an anticipated bitcoin rewards credit card.

Fold’s business model seeks to capitalize on generational shifts in wealth perception where younger demographics increasingly view bitcoin as fundamental to their financial lives rather than an alternative asset class [S1]. This strategic positioning involves operational complexity inherent in fintech product development - from initial pilots through stage-gated rollouts towards full go-to-market readiness.

Financially, Fold’s operating income has consistently been negative but showed progressive improvement from FY2021 (-$100K) through FY2024 (-$2.9M), representing a roughly 21.7% year-over-year uplift at the latest point available [F1]. However, net income tells a more severe story: after reporting profits in FY2022 (+$1.12M) and FY2023 (+$4.44M), it plunged massively into negative territory reaching -$69.6M by FY2025 [F1], underscoring significant investment into growth initiatives including bitcoin treasury expansion and new product development.

This trajectory embodies the classic fintech expansion phase but also stresses the vast operational expenditures required to scale a regulated crypto-financial ecosystem.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -70 | -16 | -3624.3% | |

| 2024 | -2 | -3 | -3 | -142.0% |

| 2023 | 4 | -5 | -4 | +298.3% |

| 2022 | 1 | -2 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | -110.5 | |

| 2024 | 117 | 22.5 |

| 2023 | 97 | -103.1 |

| 2022 | -13.1 |

Source: SEC companyfacts cache [F1].

Fold’s improving operating income juxtaposed with widening net losses reflects heavy non-operating costs and strategic growth spending [F1].

Bitcoin Treasury Building: Strategic Rationale and Risks

Central to Fold’s unique value proposition is its corporate treasury holding significant bitcoin assets. The company views this as directly aligning corporate interests with those of its customer base who are increasingly invested in bitcoin appreciation [S1]. Consequently, Fold has actively expanded its corporate bitcoin holdings supported through sophisticated capital structures.

Key among these is the Master Loan Agreement (MLA) with Two Prime Lending Limited executed in late 2025 allowing advances secured against bitcoin collateral. The MLA was amended multiple times to reflect harsher terms: interest rates stepped up from an initial 6.5% per annum to currently 8.5%, while collateral thresholds tied to maintenance requirements were lowered significantly — initial collateral levels dropped from 250% down to 160%, collateral call levels fell from 175% to 135%, increasing the likelihood of margin calls during volatile markets [S5].

This structure embeds a material execution risk: downturns in bitcoin price below predefined trigger points compel repayment or liquidation events placing liquidity stress on Fold's balance sheet. Moreover, decreased cushion percentages give Two Prime more latitude to act swiftly in adverse conditions [S5][S6].

In addition, on February 26, 2026, Fold refinanced prior convertible notes by entering into a new promissory note agreement with SATS Credit Fund L.P., featuring a higher interest rate of 10% per annum and deleveraging prior secured notes collateralized by hundreds of bitcoins [S6]. This new note adds renewable capacity for indebtedness up to $25 million excluding debt related directly to the planned credit card program, reflecting flexible but costlier funding avenues.

Thus, while Fold’s treasury strategy deepens alignment with client value creation potential via asset appreciation exposure, it carries substantial collateral management challenges tied to market volatility.

The Upcoming Bitcoin Rewards Credit Card: Development Status and Market Implications

A critical growth driver for Fold lies in its forthcoming bitcoin rewards credit card offering designed to enhance user engagement within its consumer financial ecosystem [S1]. The product promises to deliver bitcoin-based rewards on everyday spending utilizing established payment rails like Visa networks.

As per filings dated early March 2026, the launch is imminent but remains conditional upon finalizing contracts with third-party service providers necessary for issuance and processing infrastructure [S15]. Success in these negotiations will advance “go-to-market readiness” positioning the credit card as a pivotal revenue stream capable of scaling user acquisition and increasing bitcoin transaction volumes.

However, these dependencies inject operational execution risk typical for fintech entrants seeking regulatory approval and integration within existing payment frameworks. Regulatory compliance along with robust payment rails integration are necessary prerequisites before public rollout can occur; any delay or failure here could impede expected revenue acceleration timelines [S8][S15].

Should the launch proceed smoothly, the credit card could transform Fold’s top-line prospects by cementing bitcoin usage habits within mainstream financial behavior patterns — bridging volatility exposure embedded in treasury holdings with steady revenue inflows from transactional fees.

Liquidity Dynamics and Debt Structure Underpinning Growth Ambitions

Liquidity metrics underline the challenges Fold faces sustaining operations amid net losses compounded by heightened debt servicing costs.

As of December 31, 2025, total current assets stood at approximately $18.1 million versus current liabilities exceeding $21 million resulting in a sub-1 current ratio of about 0.86 [F1]. The cash ratio lagged further at roughly 0.36 reflecting limited immediately available liquid resources (cash & equivalents around $7.65 million). These ratios indicate tight short-term liquidity positioning requiring active working capital management and access to financing markets.

Loan amendments during late 2025 increased annual interest expenses notably while simultaneously reducing collateral buffer levels which creates refinancing pressure if operating cash flows do not improve markedly or if market conditions worsen [S5][S6]. Equity financing partially offsets these pressures; however, sustaining an investment-grade rating or favorable lending terms remains uncertain given negative profitability trends.

Pragmatically speaking for stakeholders versed in fintech capital structure analysis, Fold operates close to covenant triggers embedded in loan documents (e.g., maintaining Nasdaq listing status) where breach events could accelerate debt repayments or restrict incremental borrowing capacity – often referred to as covenant risk scenarios within credit facility management contexts [S6][S20].

Thus liquidity availability is heavily contingent on both stable bitcoin valuations protecting collateral integrity plus timely equity raises or cash flow improvements enabling sustainable debt servicing.

Capital Allocation Trends: Share Buybacks, Dividends, and Cash Flow Realities

Intriguingly for an emerging growth company entrenched in early stage product evolution coupled with sharp negative cash flow (operating cash flow declined nearly four-fold YOY between FY2024 and FY2025), Fold maintained aggressive share repurchase programs evident especially throughout FY2023–FY2024 periods [$96M then rose to $116M respectively] [F1][S7–S25]. This policy stands out given typical fintech peer conservatism during capital-intensive expansions prioritizing reinvestment over shareholder returns.

No dividends have been declared consistent with fintech growth-stage norms preserving internal capital for innovation cycles instead.

This buyback approach could reflect management signaling confidence or attempts at supporting share price levels amid prevailing volatility impacting crypto-related equities broadly; however operational sustainability suggests prudent scrutiny of buybacks given simultaneous escalating net losses (-$69 million FY2025) combined with ongoing operating cash deficits nearing $16 million annually [F1].

From a sector perspective incorporating speculative crypto-fintech dynamics this duality underscores potential tradeoffs between investor sentiment management versus rigorous liquidity stewardship needed for foundational product launches.

Financial Health Snapshot: Profitability Metrics and Operating Challenges

Fold exhibits persistent unprofitability characterized by expanding net loss magnitudes yet marginally improving operating income figures prior fiscal year-end indications:

- Operating income shifted from approximately -$3.73M in FY2023 improving ~21.7% YOY by end-FY2024 though remaining negative (-$2.9M)

- Net income collapsed from modest profits ($4.44M FY23) into heavy losses (-$69.6M FY25), driven largely by increased non-operating expenses including interest costs associated with heavier debt loads

- Operating cash flow worsened drastically reflecting operational scaling expenditures outpacing revenue generation capacity [-$16.12M FY25 vs -$3.43M FY24]

- Book equity turned positive reaching +$62.99M end-2025 indicating favorable capital injections despite prior deficits

- Approximate ROE approximates negative ~110%, illustrating lack of near-term profitability relative to equity base [F1]

These figures cumulatively paint a picture of intense financial strain inherent within rapid fintech expansion trajectories complicated by volatile asset backing (bitcoin holdings) requiring continuous capital access while awaiting key product monetization events.

Outlook and Milestones: What Investors Should Monitor

Looking forward without explicit earnings guidance provided by management at filing time,[N/A] attention should center on several key milestones influencing Fold’s capacity to stabilize finances while unlocking growth pathways:

- Timely launch and market acceptance of the anticipated bitcoin rewards credit card dependent on securing contractual arrangements with third-party service providers representing go-to-market readiness hurdles as well as adherence to regulatory requisites impacting payment network integration timelines [S15]

- Monitoring of prevailing bitcoin price levels especially around defined "trigger prices" ($45K/$40K/$37K per BTC thresholds) directly affecting debt prepayment obligations under new promissory note facilities which bear heavily on liquidity planning given their collateral call implications [S6]

- Regulatory environment evolutions cited within risk disclosures highlighting potential compliance burdens specific to cryptocurrency banking products requiring proactive oversight adapting policy changes rapidly impacting operational cost structures or permissible business activities [S4]

- Analyst coverage dynamics reflecting external assessments that may influence market sentiment around speculative crypto fintech enterprises amidst broader macro-economic volatility contexts

Given these factors intrinsic "execution risks" remain elevated though aligned incentives via corporate treasury stakeholding provide strategic coherence between investor value creation potential tightly woven within innovative product pipeline progression alongside fluctuating bitcoin valuation dynamics.

This analysis relies strictly on reported SEC filings and company facts as of March 17, 2026 [F1],[S1–S25] without projecting future financial outcomes or issuing investment opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments