Empire Petroleum’s Shrinking Revenues and Ballooning Losses Signal Urgent Liquidity Risks

The company's declining top-line and mounting losses underscore growing financial strain amid liquidity pressures.

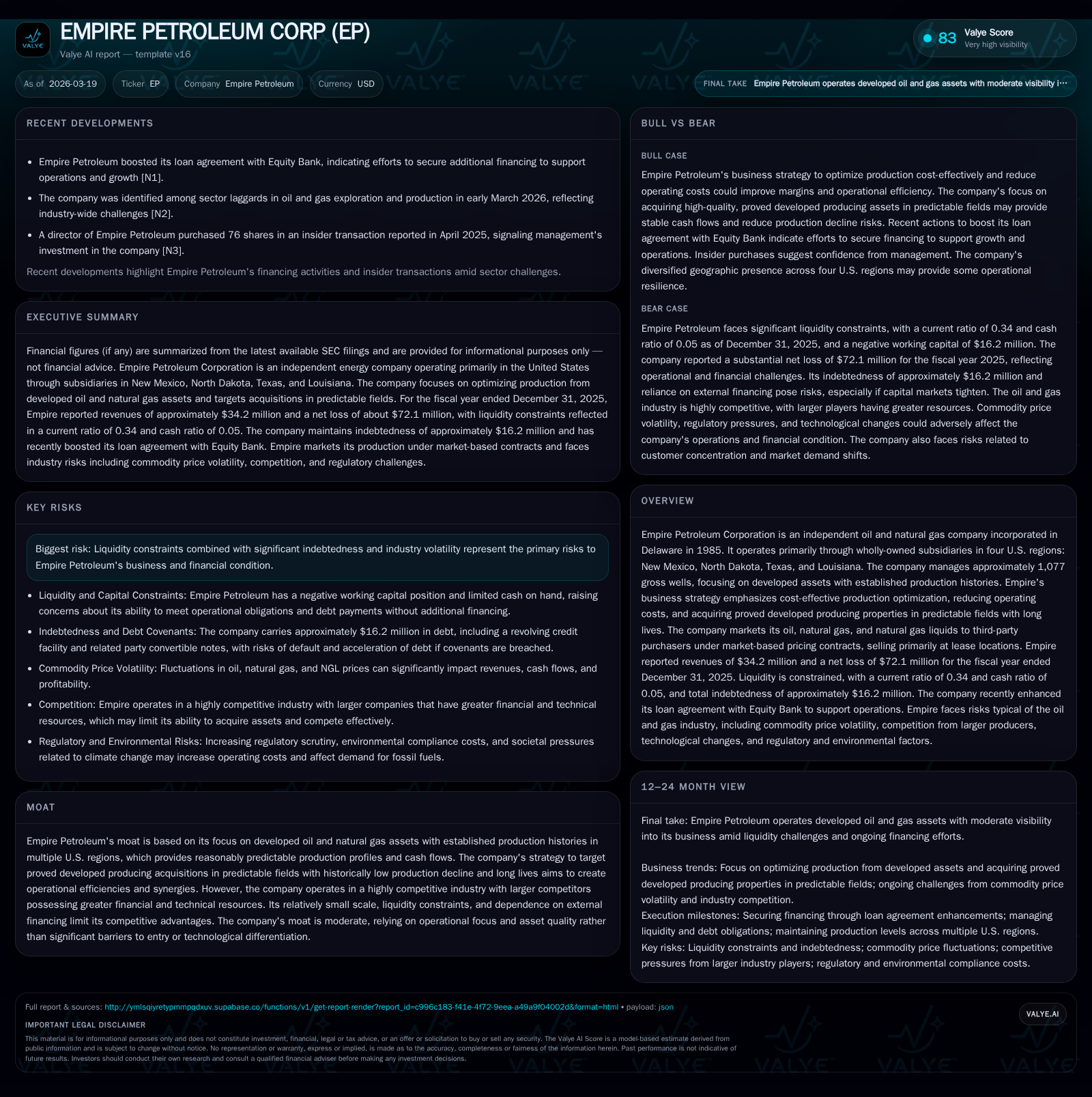

Empire Petroleum, historically reliant on stable cash flows from its focus on developed oil and gas assets, suffered a sharp deterioration in profitability and liquidity in fiscal 2025. Revenues fell over 21% year-over-year while net losses expanded to $72.1 million, driven by operating inefficiencies, commodity price volatility, and competitive pressures. The company faces constrained financial flexibility with a deteriorated current ratio of 0.34 and negative working capital, heightening the risk of financing challenges. Despite efforts to optimize production and participate modestly in development programs, Empire's liquidity risks cloud growth prospects and capital allocation strategies.

From Stability to Strain: Charting Empire’s Revenue and Profit Decline

Empire Petroleum has historically relied on a stable portfolio of approximately 1,077 gross wells across four U.S. regions—New Mexico, North Dakota, Texas, and Louisiana—focusing predominantly on proved developed producing properties with established production histories [S14]. This operational focus supported reasonably predictable production volumes and cash flows until recent years.

Fiscal 2025 marked a pronounced deterioration in key financial metrics [F1]. Revenues fell 21.6% year-over-year from $43.7 million in 2024 to $34.2 million, continuing a multi-year decline from peak revenues of nearly $52.9 million recorded in 2022. Operating income swung dramatically from moderate losses near -$13.7 million in 2024 to a staggering -$71.3 million loss last year—a decline exceeding 420%. Net income mirrored this collapse with losses expanding from -$16.2 million in 2024 to -$72.1 million for the year ended December 31, 2025.

Operating cash flow followed a volatile course, recovering briefly to about $6.2 million positive CFO in 2024 but reversing back to -$3.95 million negative last year—a clear sign of worsening core business profitability [F1]. Capital expenditures remained essentially flat at approximately $2.1 million annually during these periods, suggesting limited reinvestment beyond sustaining existing production capacity [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 34 | -72 | -4 | -71 | -21.6% | -345.0% |

| 2024 | 44 | -16 | 6 | -14 | +8.9% | -29.9% |

| 2023 | 40 | -12 | -10 | -12 | -24.2% | -276.0% |

| 2022 | 53 | 7 | 18 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1564.8 | |

| 2024 | 4 | -25.8 |

| 2023 | -12 | -35.7 |

| 2022 | 30.5 |

Source: SEC companyfacts cache [F1].

Financial figures sourced from SEC filings and XBRL data [F1].

This steep reversal reveals that Empire’s longstanding niche as an operator of stabilized producing properties is under severe operational and financial stress.

Operational Focus Versus Market Realities: Competitive Pressures Affect Asset Performance

Empire's strategy emphasizes acquiring and managing proved developed producing properties exhibiting low production decline rates and long productive lives [S14]. Its operations span New Mexico’s Greyburg/San Andres formations, North Dakota’s Bakken plays among others, Texas pockets, and Louisiana fields where it recently expanded development efforts [S5][S12][N1][S3].

However, this model faces substantial headwinds amid intensifying competition for acquisitions and service resources as larger independent and integrated players pursue similar asset profiles [S5]. Rising demand for drilling rigs, workover equipment, pipe materials, and skilled personnel has driven service costs higher while availability remains intermittently constrained—pressures disproportionately affecting smaller operators like Empire with limited scale [S5].

Simultaneously, commodity prices remain volatile due to macroeconomic factors including geopolitical events and inflationary concerns that influence realized prices under market-based contracts at lease locations [S6][S23]. This volatility compresses netbacks especially when coupled with elevated operating expenses.

Despite management initiatives targeting cost-effective well optimization and unit cost reduction [S14], competitors' superior access to capital and advanced technologies pose ongoing challenges for Empire's competitive positioning.

Liquidity Crunches and Leverage: Tight Financial Flexibility

As of December 31, 2025, Empire carried total indebtedness of approximately $16.2 million secured against substantially all producing assets among its subsidiaries [F1][S7][S10]. This includes revolving credit facilities connected with related parties such as Energy Evolution Master Fund Ltd., which has historically provided critical acquisition capital but introduces concentration risk [S8].

Current assets stood at $8.18 million versus current liabilities of $24.34 million yielding a current ratio of roughly 0.34—a marker of acute short-term liquidity challenges threatening operational funding ability [F1][S4][S10]. Negative working capital totaled about $16 million at fiscal year-end reflecting balance sheet deterioration driven by persistent net losses and negative operating cash flow [S16].

Although amendments extended maturity dates on the credit facility into late 2028 with incremental revolver commitment reductions monthly, the company remains dependent on preserving covenant compliance amid rising interest rates that elevate borrowing costs [N1][S21][S22][S25]. Failure to secure waivers or refinancing could trigger defaults including accelerated debt repayment or forced liquidation.

Environmental regulations and ESG pressures have also constrained available funding pools as institutional investors reduce exposure to fossil fuels—adding difficulty raising equity or debt capital going forward [S15][S19]. This liquidity squeeze limits financial maneuverability or growth investments without increasing leverage or diluting shareholders.

Capital Allocation Under Pressure: Reinvestment Focus Amid Losses

With net losses surpassing $72 million last fiscal year alongside negative free cash flow estimated near -$6 million (operating cash flow minus capital expenditures), shareholder distributions have been suspended entirely [F1][S24][S27]. Return on equity is distorted due to negative equity reported at approximately -$4.6 million year-end reflecting accumulated losses rather than operational efficiency.

Capital expenditures hover around $2 million annually focusing principally on maintaining existing well productivity rather than expansionary drilling programs [F1][S29], underscoring that sustaining production volumes takes precedence amid constrained funding.

No dividends or share repurchases have been reported recently given the precarious balance sheet position compounded by operating deficits—reflecting a conservative approach aimed at preserving liquidity amidst uncertain industry fundamentals.

Development Program Initiatives: Growth Intent Amid Constraints

Despite financial strains, management disclosed participation in an oil and natural gas development program located in Louisiana as of March 2026 filings indicating efforts toward incremental production growth through selective project engagement aligned with core expertise in low-decline fields [N1][S3].

While investment specifics remain undisclosed and appear limited by overall CAPEX budgets capped near maintenance levels historically, this initiative signals tactical intent to capture value enhancement opportunities within manageable risk parameters.

However, ongoing liquidity pressure evidenced by weak short-term ratios coupled with poor cash generation profiles may limit aggressive pursuit or scaling without additional external capital or asset monetization.

What to Watch: Key Milestones and Risks Over the Next Year

- Progress on refinancing the extended third amendment revolver credit facility maturing December 29, 2028 including lender support for potential further amendments due to covenant pressures [N1][S4][S22].

- Operating results from the Louisiana development program testing potential for arresting production declines or improving cash flows despite cost challenges.

- Commodity price trends influencing realized selling prices directly tied to macroeconomic variables impacting revenue stability [S23].

- Any credit covenant breaches potentially triggering accelerated debt repayments or loss of borrowing capacity necessitating asset sales or equity issuance diluting shareholders.

- Adequacy of liquidity buffers relative to monthly burn rates given negative working capital raising going concern considerations under SEC guidance.

- Shifts in market sentiment regarding fossil fuel exposure influenced by ESG investment trends restricting access to affordable capital beyond traditional lenders risking costlier funding terms.

Empire Petroleum exemplifies smaller independents grappling with heightened competition for dependable producing assets while burdened by mounting leverage amid industry cyclicality tightening liquidity avenues—severely constraining growth prospects and shareholder value mitigation options.

This report is based exclusively on publicly available data including SEC filings dated up to March 19, 2026; news releases relevant through early calendar year; company facts snapshots capturing fiscal years ended December annually through FY2025 inclusive; it does not constitute investment advice nor an offer invitation regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments