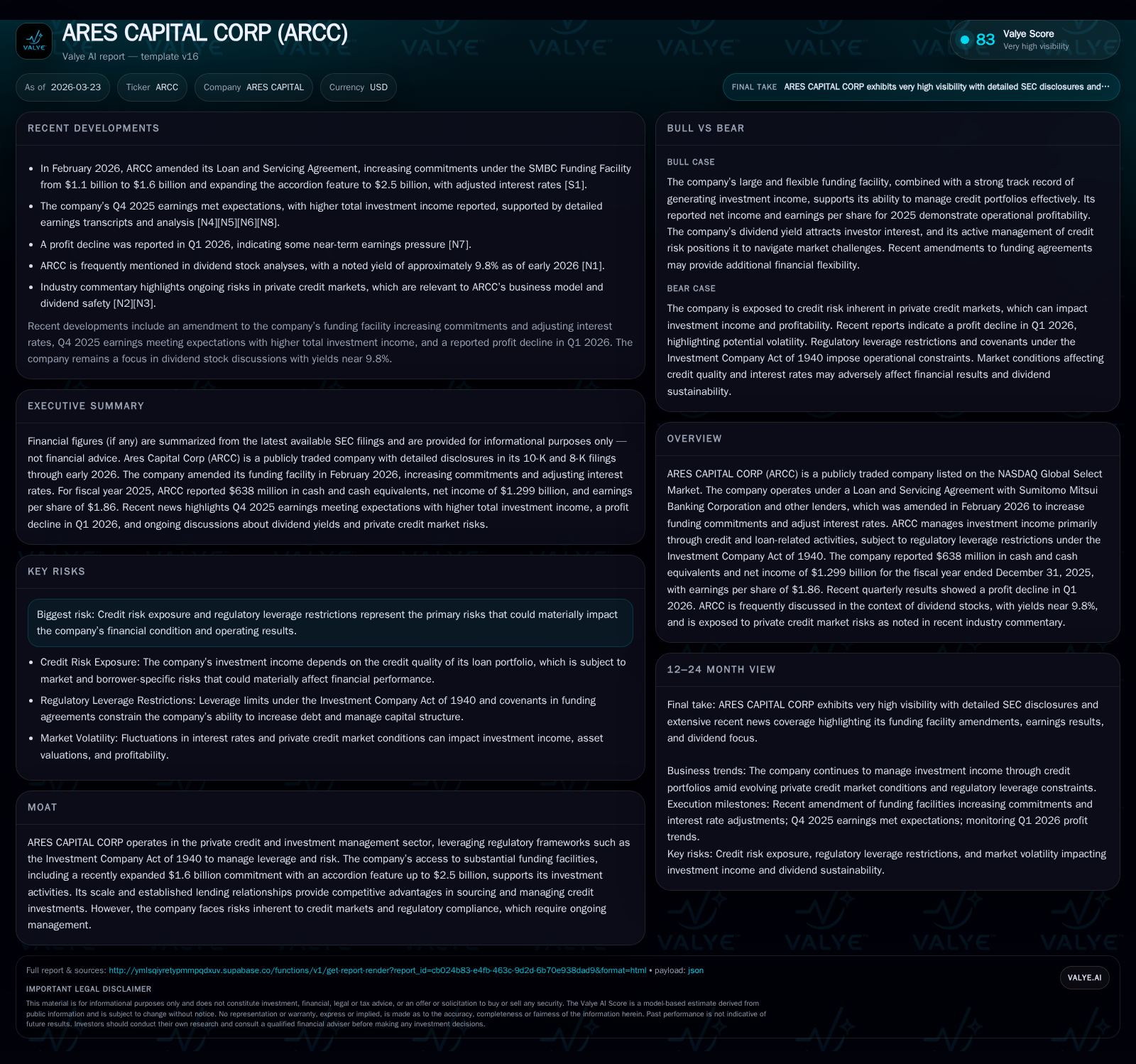

ARES CAPITAL CORP Shows Capital Adaptation as Private Credit Landscape Shifts

ARCC leverages enhanced funding facilities and navigates operating headwinds amid evolving private credit market dynamics.

Ares Capital Corp (ARCC) expanded its SMBC funding facility in early 2026, raising commitments by nearly 45% and increasing the accordion capacity to $2.5 billion, reflecting proactive capital management. Despite this, ARCC reported a net income decline of 14.7% in fiscal 2025 with operating cash flow remaining negative though improving year-over-year. The company maintains a generous dividend yield near 9.8%, raising questions on payout sustainability against operating cash flow deficits under strict leverage constraints governed by the Investment Company Act of 1940. Market exposure to private credit risks and regulatory compliance remain key operational considerations as ARCC balances growth ambitions with capital discipline.

Historical Growth Trajectory and Profit Drivers Through 2025

Ares Capital Corporation has demonstrated significant balance sheet growth over recent years while navigating profit volatility consistent with private credit investment cycles. Equity surged from $9.56 billion at fiscal year-end 2022 to approximately $14.3 billion by the close of 2025—a robust 50% increase that underscores ARCC’s expanding financing capacity ([F1]). Net income exhibited a sharp rise between 2022 ($600 million) and stable results in both 2023 and 2024 ($1.522 billion each), before declining by roughly -14.7% in fiscal 2025 to $1.299 billion ([F1]). This contraction reflects multiple headwinds including increased credit risk provisioning and market volatility during the year.

Dividends paid have consistently grown alongside equity expansion, rising from $912 million in 2022 to $1.264 billion in the latest fiscal year ([F1]). This steady increase fuels investor interest given the yield nearing double digits but pressures payout coverage given operating cash flow dynamics.

Summary Table: ARES CAPITAL CORP Historical Financials Summary (FY2022-FY2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | Net YoY |

|---|---|---|---|

| 2025 | 1299 | -1.7 | -14.7% |

| 2024 | 1522 | -2.1 | 0.0% |

| 2023 | 1522 | 0.5 | +153.7% |

| 2022 | 600 | -1.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 1264 | 9.1 |

| 2024 | 1139 | 11.4 |

| 2023 | 1031 | 13.6 |

| 2022 | 912 | 6.3 |

Source: SEC companyfacts cache [F1].

Note: ROE derived as Net Income / Equity per fiscal year.

Analyzing the YoY Earnings Variations and Their Underlying Causes

The notable dip in net income during FY2025 compared to prior years warrants dissection through several lenses documented in recent filings [S1],[S7] and market commentary [N3],[N6]. ARCC’s revenue is predominantly derived from interest income on its loan portfolio within private credit markets which saw increased stress transitioning into late-2025.

Declines correspond partly to growing non-accrual assets as borrowers face tighter liquidity conditions, alongside conservative reserve builds that weigh on reported profitability [S7]. Furthermore, macroeconomic headwinds such as inflationary pressures forcing cost adjustments and interest rate fluctuations exacerbated challenges.

Recent quarterly disclosures have highlighted these dynamics further [N3], noting margin compression linked to competitive lending spreads and regulatory leverage restrictions constraining opportunistic borrowing.

Capital Structure Evolution: The Role of the SMBC Funding Facility Amendment

In February 2026, ARCC announced a critical amendment [S3],[S4],[S5],[S6] to its Loan and Servicing Agreement with Sumitomo Mitsui Banking Corporation (SMBC), increasing the committed funding from $1.1 billion to $1.6 billion—a near-45% uplift—while boosting the accordion feature allowing expansions up to $2.5 billion if warranted.

This facility amendment also included a marginal reduction in interest rate spreads, from a spread of either (a) +180 bps over SOFR or +80 bps over the base rate down to (b) +175 bps over SOFR or +75 bps over base rate ([S4]). Such shifts signal subtle cost improvements potentially tied to yield curve movements or renegotiated credit terms.

Borrowing under this facility remains tightly regulated under Investment Company Act guidelines limiting leverage ratios [S4], ensuring ARCC maintains compliance while preserving liquidity to fund new deals and refinance existing positions without triggering restrictive covenants.

The expanded facility markedly enhances ARCC's flexibility in sourcing new transactions amid fluctuating private credit supply-demand balances.

Dividend Policy amidst ~9.8% Yield and Operating Cash Flow Challenges

ARCC’s dividend yield attracting ~9.8% attention is supported by steadily increasing distributions totaling approximately $1.264 billion for FY2025 ([F1],[N2]). However, operating cash flows remain negative at -$1.717 billion–albeit improved compared with -$2.128 billion last year—implying dividends are supplemented by capital market activities or non-cash accounting effects ([F1]).

Within Business Development Company (BDC) frameworks, maintaining high dividend payouts is essential for tax benefits but poses sustainability risks absent positive core operating cash generation.

Industry practitioners note that such payout mechanics often rely on regulated leverage ceilings allowing external borrowings and equity raises; nonetheless, persistent negative CFO warrants monitoring for potential liquidity stress points or dividend policy recalibration [N2].

The juxtaposition of attractive income streams against underlying cash flow deficits highlights a classic BDC risk-return tradeoff where investors must weigh yield versus potential capital erosion risks.

Private Credit Market Exposure and Regulatory Leverage Constraints

Operating within a niche private credit segment exposes ARCC to unique vulnerabilities amplified by macroeconomic uncertainty [N10]. Rising non-accrual loans evidence borrower distress requiring vigilant provisioning ([N10],[S7]) while tighter lending spreads compress incremental returns.

Regulatory oversight under the Investment Company Act imposes leverage ratio ceilings mandating prudence in debt accumulation relative to equity [S4]. This governance restricts risk appetite but also institutes guardrails protecting solvency and asset quality.

Practitioners emphasize continuous covenant monitoring coupled with dynamic portfolio rebalancing as critical for maintaining operational flexibility without breaching these thresholds.

Non-accrual trends should be closely watched by stakeholders given their direct bearing on realized investment income and future earnings visibility.

Outlook: Investment Income Prospects and Risk Factors to Monitor

Forward-looking analysis based on public disclosures [N1],[N6],[S1] suggests investors should prioritize several indicators: sustained access to diversified funding sources post-facility amendment; evolving credit performance metrics; and macroeconomic influences affecting underwriting standards.

No explicit earnings guidance was provided recently; however, sector commentary underscores a cautious environment where careful deal selection amid persistent credit headwinds will define performance trajectories [N1],[N6]. Liquidity management remains paramount with tightened covenant constraints posing ongoing strategic considerations.

Dividend continuity will need alignment with improved operating cash flows or alternative capital strategies if market conditions deteriorate.

Evaluating Return Efficiency: ROE Trends and Capital Allocation Discipline

Despite operational challenges, ARCC’s approximate return on equity stood near a moderate ~9.1% for FY2025 based on reported net income against total equity levels ([F1]). This figure reflects constrained profitability typical of large-scale BDCs balancing asset-heavy portfolios against regulatory limitations.

Capital allocation via dividends increased consistently over four years while no buyback program was reported ([F1]), indicating emphasis on rewarding shareholders through distribution rather than share repurchases.

Negative operating cash flows introduce complexity around reinvestment capacity; nonetheless, improved CFO trends are encouraging signals toward regaining self-sustaining earnings power.

The company’s capital discipline through incremental equity growth combined with amended borrowing agreements indicates strategic intent not only to fund pipeline opportunities but also manage shareholder expectations prudently.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations regarding Ares Capital Corp or any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments