Lument Finance Trust Harnesses Multifamily Floating-Rate Debt for ROI Resilience

Lument Finance Trust leverages its affiliation with Lument Investment Management and ORIX USA to structure a predominantly floating-rate, middle-market multifamily CRE debt portfolio paired with CLO and secured financing strategies.

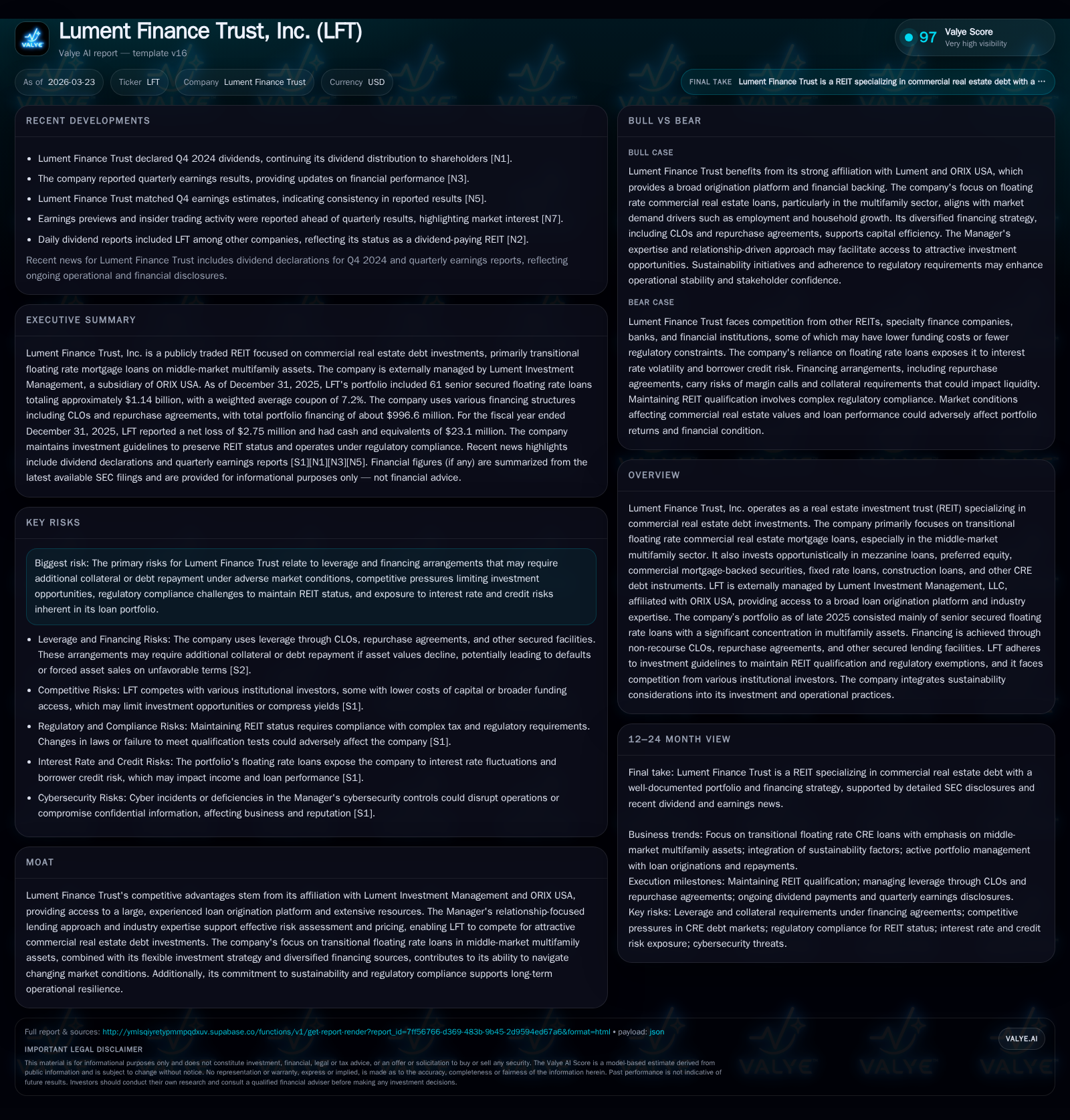

Lument Finance Trust (LFT) specializes in transitional floating-rate commercial real estate loans focusing on middle-market multifamily assets, driven by its external manager Lument Investment Management, an ORIX USA affiliate. Despite a sharp net income decline in 2025, LFT sustains operational cash flow via its large senior secured loan portfolio. The company utilizes non-recourse CLOs, repurchase agreements, and term loans to match fund assets, controlling interest rate risk amidst market volatility. Dividend payouts remain consistent, supported chiefly by strong cash flows. Going forward, LFT faces challenges from collateral call risks under repurchase agreements and competitive pressures but benefits from a seasoned origination platform and disciplined governance including robust cybersecurity oversight.

Track Record: Growth Trajectory and Recent Profitability Reversal

Lument Finance Trust has established a focused trajectory centered on transitional floating rate commercial real estate loans largely anchored in middle-market multifamily assets. Over the four-year period ending in FY2025, the company demonstrated consistent net income growth through FY2024 but experienced a dramatic contraction in FY2025. Specifically, net income declined by over 112% year-over-year from $22.6 million in FY2024 to a loss of approximately $2.7 million in FY2025 according to companyfacts data [F1]. This reversal highlights operational pressure despite maintaining a steady investment focus.

Operating cash flow similarly decreased from $27.1 million to roughly $10.1 million (-62.8% YoY), indicating reduced cash generation capacity yet positive CFO retained even during the earnings dip, reflecting underlying portfolio cash yield support [F1]. Equity levels showed moderate contraction from $237.8 million to $219.0 million during the same period, signaling some capital erosion but retention of substantial invested capital base.

Dividends increased steadily from roughly $11.6 million in FY2022 to $18.3 million paid in FY2025, underscoring management’s commitment to shareholder yield even amid earnings volatility [F1]. This disconnect between accounting earnings and cash distributions suggests reliance on stable interest income streams bolstered by careful capital management.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -3 | 10 | -112.1% |

| 2024 | 23 | 27 | +14.9% |

| 2023 | 20 | 25 | +99.9% |

| 2022 | 10 | 16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 18 | -1.3 |

| 2024 | 16 | 9.5 |

| 2023 | 13 | 8.2 |

| 2022 | 12 | 4.1 |

Source: SEC companyfacts cache [F1].

Investment Focus: Multifamily Floating Rate Loans and Opportunistic Debt Instruments

LFT’s core business model centers on originated or acquired transitional floating-rate commercial real estate mortgage loans primarily secured by middle-market multifamily properties [S14][S9][S11]. These loans exhibit key features typical for the sector: principal balances typically range between $5 million and $75 million with loan-to-value ratios up to approximately 85% as-is value or up to 75% as stabilized value [S9][S11]. The loan terms are mostly three years with two one-year extension options and interest is linked to the one-month term SOFR index plus spread floors (historically around a weighted average coupon of ~7.2% as of end-2025) [S10][S11].

Beyond senior secured loans making up almost all of the $1.14 billion portfolio balance at year-end FY2025 (61 loans), LFT opportunistically allocates capital across mezzanine loans issued against equity interests in borrowers (junior to first mortgages), preferred equity positions within commercial structures and CMBS tranches as market conditions dictate [S14][S28]. This flexible approach allows efficient capital deployment tailored for risk/return optimization.

Capital Structure: Matching Funding via CLOs, Repurchase Agreements, and Term Loans

An essential pillar sustaining LFT's investment platform is an actively managed capital structure designed to match fund assets with appropriate liability templates minimizing tenor or index mismatches that could exacerbate market dislocations.

As of December 31 2025:

- The company issued $663.8 million in commercial real estate CLO notes backed predominantly by the mortgage loan portfolio — this represents non-recourse financing that provides about an effective advance rate of approximately 88%, funded at a cost of SOFR + ~191 basis points pre-transaction costs [S4][S6].

- A new master repurchase agreement with JPMorgan set at up to $450 million also signed in late 2025 provides revolving liquidity subject to collateral valuation thresholds [S2][S7][S19]; advances here accrue interest at term SOFR plus negotiated spreads.

- A separate secured term lending agreement supplements the capital base with access up to $50 million at fixed or floating rates depending on terms currently drawn down to around $17 million as per Q4 reporting [S8][S16].

This matched funding framework supports duration alignment between assets with relatively short maturities (~1.7 years weighted average) against liabilities structured not to incur margin calls or forced sales unless severe collateral value deterioration occurs [S4]. The blend of unsecured credit facilities alongside asset-specific securitizations permits flexible leverage adjustment calibrated for risk tolerance.

Leverage Mechanism and Risk Controls: Managing Collateral Calls and Interest Risks

Central leverage-related risks stem primarily from contractual obligations under repurchase agreements where collateral pledged may see marked-to-market declines necessitating additional collateral posting or partial debt repayment [S2][S12]. If unable to meet these margin calls timely due to liquidity constraints or unfavorable market conditions forcing asset disposals at depressed prices may trigger defaults leading to escalated funding costs or covenant breaches.

While organizational documents do not cap maximum leverage outright — financing facilities impose explicit leverage ratios and borrowing base tests ensuring overall leverage remains commensurate with portfolio risk profiles [S4],[S7],[S12]. There is no external leverage governance beyond board-mandated policies but contractual covenants enforce prudence.

Risk mitigation is supported by the external Manager’s credit assessment protocols leveraging extensive industry expertise via Lument originations teams focused on sponsor quality and property market fundamentals — fostering disciplined underwriting standards that help withstand cyclical downturns [S9]. Board-level Audit Committee oversight extends into monitoring financial risk exposures including margin posting contingencies under counterparties’ credit terms ensuring proactive collateral management [S1].

Dividends and Returns: Evaluating Payout Consistency Against Earnings Fluctuations

Despite recorded negative net income in FY2025 (-$2.75 million), LFT continued regular dividend payments totaling approximately $18.3 million that year — up from about $15.7 million paid the prior year — reflecting commitment to delivering shareholder yield primarily funded through ongoing operating cash flows exceeding $10 million in FY2025 albeit diminished from prior levels [F1][N1][S21].

The implied payout ratio based purely on net income appears untenable given losses but aligns more reasonably when assessed against operating cash flow coverage demonstrating dividend coverage albeit compressed relative to previous years where positive NI supported distributions more robustly.

This pattern is emblematic across many CRE debt REITs focusing on stabilized interest income over mark-to-market gains/losses and aligns with maintaining REIT qualification which requires substantial distributions of taxable income excluding certain non-cash items per tax code provisions discussed among regulatory disclosures [S21][S27].

Future Outlook: Growth Constraints and Opportunities Under Current Market Conditions

Looking ahead while LFT leverages significant origination depth via its affiliation with Lument IM/ORIX USA — competitive pressures have intensified as multiple REITs and alternative lenders compete aggressively for middle-market multifamily transitional loans often compressing yields relative to earlier investment cycles [N1][S13]. Some competitors benefit from broader capital access or strategic flexibility unavailable under REIT regulations.

Additional growth challenges arise from managing financing structure risks especially potential margin calls tied to repurchase agreements requiring conservative liquidity management amidst interest rate uncertainty affecting refinancing affordability or borrower creditworthiness [S2][S12][S15]. Regulatory compliance vigilance remains critical given tax qualification dependencies demanding diversified ownership structures alongside precise adherence to distribution mandates.

However, opportunities persist to exploit niche expertise deploying capital efficiently into transitional CRE sectors benefiting from demographic-driven demand like multifamily housing supported by ORIX’s extensive industry network enabling timely execution of borrower-centric deals with favorable risk-adjusted return prospects .

Governance and Cybersecurity Oversight within External Management Framework

The governance structure relies significantly on oversight by an independent board administering risk management responsibility directly supplemented by specialized committees including an Audit Committee charged with supervising financial risks encompassing leverage-related exposure and cyber threat vulnerabilities [S1].

Day-to-day operations including investment decisions are outsourced to Lument Investment Management LLC — a subsidiary under ORIX USA umbrella — providing not only origination capabilities but also shared IT infrastructure supporting cybersecurity governance aligned explicitly with NIST Cybersecurity Framework standards ensuring layered defense mechanisms through ORIX’s global technology operations managed by HCLTech experts continually monitoring threat landscape via SIEM/SOAR platforms.

This 'defense in depth' strategy focuses on protecting confidentiality integrity availability pillars critical for operational continuity safeguarding sensitive information assets against sophisticated cyber threats prevalent across financial services sectors today emphasizing proactive incident response training exercises conducted annually for preparedness validation within risk frameworks overseen formally at board level reinforcing stakeholder confidence.

Disclaimer: This report is based solely on publicly available information as of March 23rd, 2026 including SEC filings and verified news sources provided herein. It is intended solely for informational purposes without any investment recommendation or advice regarding securities of Lument Finance Trust Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments