KORU Medical Systems’ Strategic Revenues Growth and Product Innovation Challenges

KORU Medical Systems shows meaningful revenue gains while facing supply dependencies and regulatory complexities in a niche infusion market.

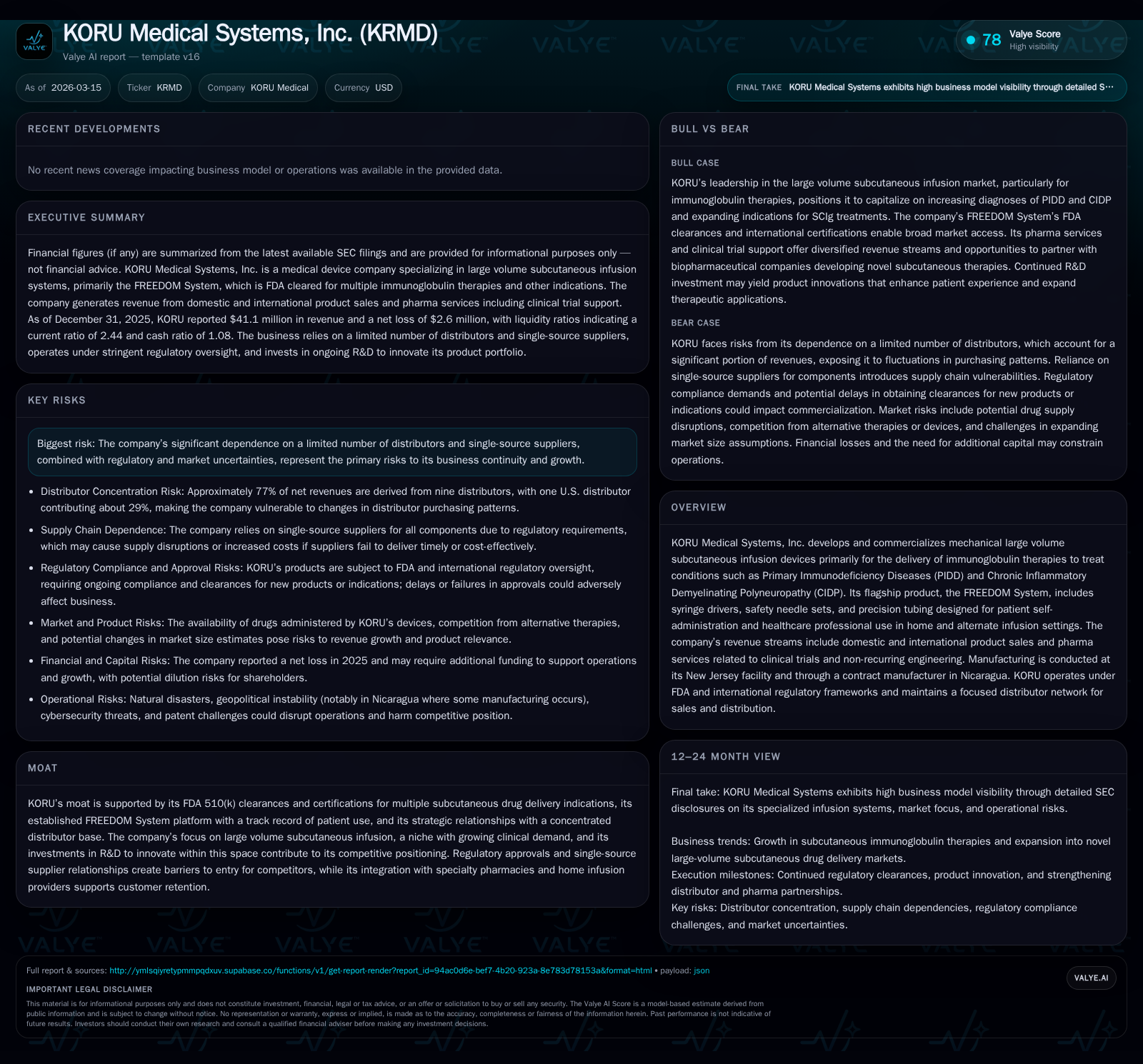

KORU Medical Systems has demonstrated robust top-line growth of 22.2% in 2025, driven by its FREEDOM System platform targeting immunoglobulin therapies for PIDD and CIDP. Despite improved operating margins with a 53.9% reduction in operating losses, the company remains unprofitable at the net income level and navigates challenges from single-source suppliers and distributor concentration risks. Regulatory demands and ongoing R&D investment underscore cautious optimism about future market expansion amid operational constraints.

Historical Revenue Acceleration with Lingering Profitability Challenges

KORU Medical Systems has posted consistent revenue growth over the past four fiscal years, culminating in a significant acceleration in 2025. Annual revenues rose from approximately $27.9 million in 2022 to $41.1 million in 2025, representing compounded growth led by expanding adoption of the FREEDOM System platform across domestic (US/Canada) and international markets [F1][S24]. The revenue increase between 2024 ($33.6 million) and 2025 ($41.1 million) marks a notable year-over-year rise of 22.2%, signaling strong demand traction.

While top-line performance improved markedly, profitability has remained elusive. Operating losses narrowed by more than half from -$6.45 million in 2024 to -$2.97 million in 2025 (a 53.9% improvement), underscoring operational efficiencies or scaling benefits; however, net income sustained a loss of -$2.64 million albeit also significantly improved compared to prior years [F1]. The company still operates below break-even but trends suggest margin gains aligned with revenue expansion.

A critically positive development is the operating cash flow turnaround: generating $462,000 in cash flow from operations in 2025 after multiple years of negative flows (e.g., -$319,000 in 2024), creating a modest free cash flow buffer when factoring out comparatively low capital expenditures [F1]. This shift provides incremental financial stability amid ongoing net losses.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 41 | -3 | 0 | -3 | +22.2% | +56.5% |

| 2024 | 34 | -6 | 0 | -6 | +18.0% | +55.9% |

| 2023 | 29 | -14 | -5 | -10 | +2.2% | -58.7% |

| 2022 | 28 | -9 | -5 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -15.5 |

| 2024 | -36.1 |

| 2023 | -67.5 |

| 2022 | -27.6 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditure data insufficient for recent years; percent changes omitted where incomplete.

Product Portfolio and FREEDOM System’s Role

Central to KORU’s business is the FREEDOM System—a family of mechanical large volume subcutaneous infusion devices including syringe drivers (Freedom60® & FreedomEdge®), HIgH-Flo Subcutaneous Safety Needle Sets™, and Precision Flow Rate Tubing™ designed primarily for immunoglobulin delivery targeting Primary Immunodeficiency Diseases (PIDD) and Chronic Inflammatory Demyelinating Polyneuropathy (CIDP). These conditions require frequent large-volume infusions typically administered at home or alternate care sites [S1][S24].

The system emphasizes patient self-administration with safety features that reduce needle-related complications while providing precise flow control essential for tolerability at higher infusion volumes. KORU’s FDA-cleared Class II medical devices benefit from established clinical use patterns that create barriers to competitor entry lacking equivalent regulatory clearance [S25][S1]. Beyond core product sales domestically and internationally, pharma services revenues arise from clinical trial support and non-recurring engineering services adapting the FREEDOM platform across biopharma contexts.

Concentration Risks: Suppliers and Distributors

Operational risks include dependency on single-source suppliers for critical product components due to regulatory validation requirements that complicate supplier changes without re-approval delays [S13][S20]. This reliance limits procurement flexibility and exposes the company to supply chain disruptions.

Additionally, KORU depends heavily on a concentrated distributor network: nine distributors accounted for approximately 77% of net revenues at year-end 2025, with one U.S.-based distributor contributing nearly one-third (29%) [S20]. This concentration creates exposure to shifts in purchasing patterns or contract renewals that could materially affect revenue streams.

Transitioning toward direct sales is possible but may be costly and less preferred by customers who value distributor convenience [S20], keeping distributor relationships critical.

Regulatory Environment Impacting Growth

KORU’s products are cleared principally via FDA’s Class II "510(k)" premarket notification pathway requiring ongoing quality management including testing protocols, post-market surveillance reporting for adverse events or malfunctions, labeling controls, recalls if necessary, plus adherence to evolving international standards such as EU MDR compliance required by December 2028 [S4][S9][S18].

Failure or delay in meeting these requirements could result in suspension or withdrawal of marketing authorizations domestically or abroad along with costly corrective actions or enforcement penalties including fines or injunctions [S6][S14].

Reimbursement dynamics also influence adoption since specialty pharmacies or ambulatory providers bill public insurance programs like Medicare/Medicaid—changes to payor policies could pressure pricing or coverage affecting device uptake [S10][S23].

Growth Opportunities Amid Market Dynamics

Long-term demand drivers include increasing diagnoses of PIDD globally—conditions requiring lifelong immunoglobulin therapy often delivered subcutaneously—and expanding indications such as Secondary Immunodeficiency Diseases (SIDD) alongside CIDP [S24].

R&D pipeline efforts aim to broaden applications into novel subcutaneous drug therapies leveraging the FREEDOM platform’s modularity supported by pharma collaborations through clinical trial feasibility work and custom engineering services within pharma service revenues [S24].

These investments are critical given competitive threats from alternative administration technologies not requiring medical devices or addressing similar disease endpoints differently [S6][S17]. Recent R&D spending around $4–5 million annually demonstrates commitment to sustaining innovation within this niche infusion segment [S13].

Financial Position: Cash Flow Turnaround & Capital Structure

At fiscal year-end December 31, 2025, KORU reported $8.9 million in cash & equivalents with current assets near $20 million against current liabilities around $8.2 million yielding a strong current ratio (~2.44x), indicating solid liquidity [F1][S15]. Equity stood at approximately $17 million though reduced relative to earlier years due mainly to cumulative losses over time.

Notably, operating cash flow turned positive at $462 thousand after consecutive years of negative cash flows ranging from hundreds of thousands to several millions since FY22—signaling improving operational efficiency supporting partially self-funded working capital needs without additional debt financing so far [F1][S15].

No recent share repurchases or dividends have been declared; prior minor buybacks were immaterial suggesting retained capital focus over shareholder distributions amid ongoing profitability challenges [F1].

Milestones & Outlook Considerations

While no explicit external guidance is provided publicly, key areas warrant monitoring:

- Advancement of R&D projects developing novel subcutaneous delivery systems compatible with emerging pharmaceutical therapies may unlock incremental revenue streams beyond immunoglobulin-focused offerings [S1][S3].

- Regulatory clearance progress especially FDA approvals facilitating label expansions or new product launches could materially impact growth trajectories though timing remains uncertain inherent to medical device sectors [S3][S9].

- Supply chain risk mitigation related to single-source suppliers including geopolitical factors affecting manufacturing operations remains vital given concentration vulnerabilities [S13][S20].

- Distributor contract renewals particularly with largest U.S.-based partners are pivotal due to revenue concentration impacting sales cadence [S20].

- Healthcare reimbursement policy developments affecting payor willingness for coverage/pricing remain macro headwinds influencing adoption rates [S10][S23].

These factors collectively shape whether KORU can convert its strategic revenue momentum into sustainable profit improvements while managing embedded operational constraints.

This report synthesizes publicly available SEC filings through March 2026 presenting an analytical overview without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments