Black Diamond Therapeutics Achieves Profitability Amid Clinical Progress and Strategic Licensing

Advancements in precision oncology programs and a key licensing partnership underpin Black Diamond’s financial turnaround and growth outlook.

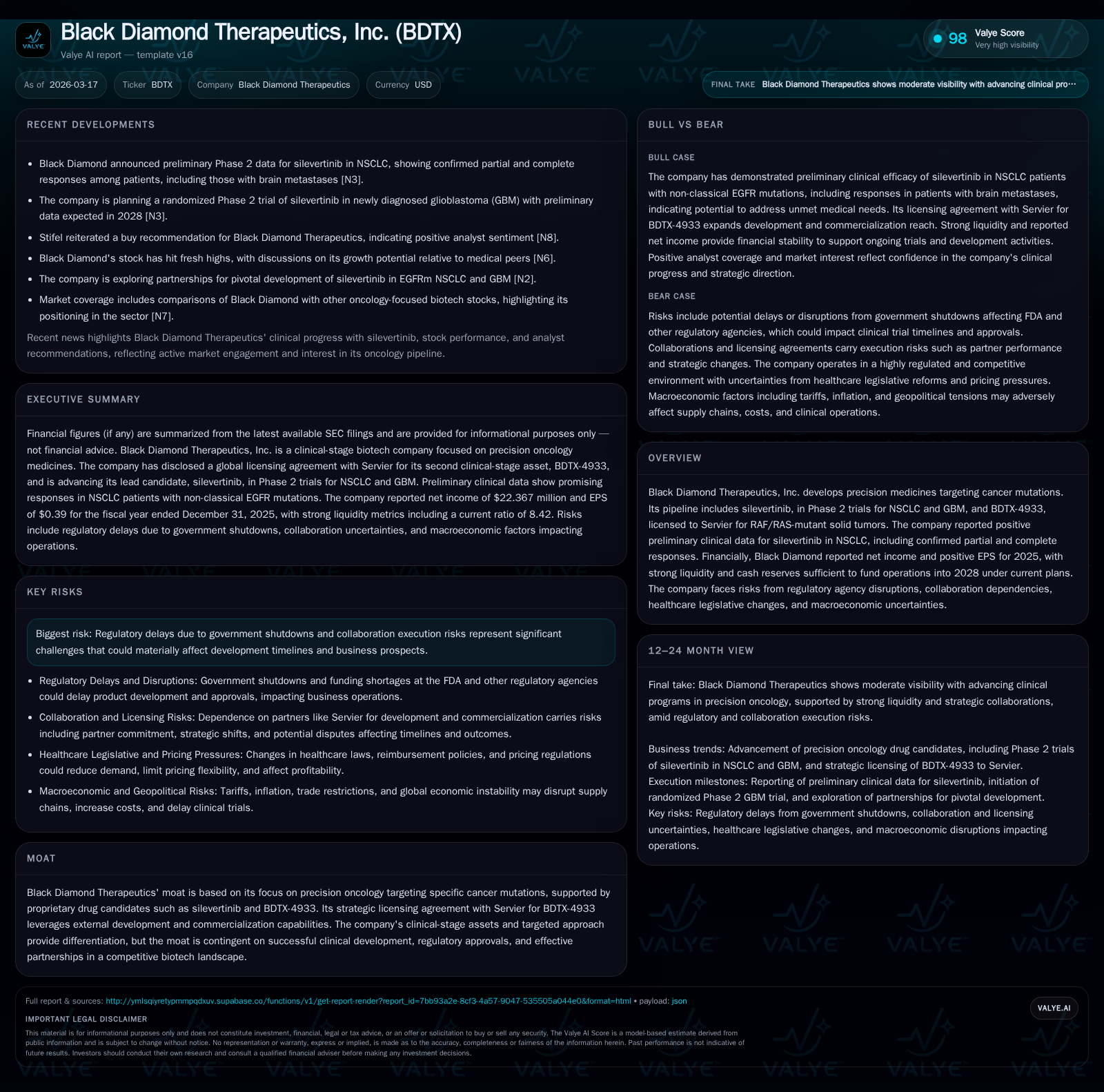

Black Diamond Therapeutics, specializing in targeted cancer therapies, reported a significant financial turnaround in 2025 with net income of $22.4 million and operating income of $12.5 million, reversing prior multi-year losses. Its lead asset, silevertinib, progressed in Phase 2 trials for EGFR-mutant NSCLC and glioblastoma, supporting future growth. The outlicensing of BDTX-4933 to Servier diversifies risk and extends development reach. With strong liquidity through 2028, the company faces clinical, regulatory, and macroeconomic challenges but is positioned to capitalize on its MasterKey therapy platform.

Historical Financial Performance

Black Diamond Therapeutics demonstrated a marked financial turnaround for the fiscal year ended December 31, 2025. After several years of substantial net losses (e.g., approximately -$91.2 million in 2022 and -$69.7 million in 2024), the company reported net income of about $22.4 million in 2025 [F1]. Operating income similarly reversed from negative results exceeding $78 million in the prior year to positive operating income near $12.5 million in 2025 [F1].

Operating cash flow improved significantly from negative $62.3 million in 2024 to positive $29.6 million in 2025 [F1]. Capital expenditures remained minimal (zero reported for FY24), supporting free cash flow generation and liquidity preservation [F1]. At year-end 2025, cash and equivalents stood at approximately $21.0 million with current assets totaling around $132.4 million against current liabilities close to $15.7 million—yielding a strong current ratio of approximately 8.42x [F1]. Equity was reported at about $112.2 million at December 31, 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 22 | 30 | 13 | +132.1% | |

| 2024 | -70 | -62 | -79 | 0 | +15.5% |

| 2023 | -82 | -67 | -86 | 33000 | +9.6% |

| 2022 | -91 | -85 | -93 | 192000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 19.9 | |

| 2024 | -62 | -83.7 |

| 2023 | -67 | -70.6 |

| 2022 | -85 | -78.8 |

Source: SEC companyfacts cache [F1].

Source: SEC filings and company facts data [F1]

Growth Drivers and Clinical Advances

The company’s improvement is primarily driven by its focus on precision oncology therapies targeting oncogenic mutation families through its MasterKey platform [S1]. The lead compound silevertinib is a brain-penetrant fourth-generation irreversible EGFR inhibitor undergoing Phase 2 clinical evaluation for EGFR-mutant non-small cell lung cancer (NSCLC). Additionally, an investigator-sponsored Phase 0/1 study in glioblastoma multiforme (GBM) has been completed with plans to initiate a randomized Phase 2 trial for newly diagnosed EGFR-altered GBM patients anticipated in Q2 2026 [S1].

The strategic outlicensing of BDTX-4933 to Servier focuses on RAF/RAS mutant solid tumors and serves to reduce development expenses while leveraging Servier's global commercialization expertise [N1],[S1].

Black Diamond’s MasterKey approach targets families of oncogenic driver mutations that share conformational activation profiles rather than single point mutations alone—a strategy designed to broaden patient populations eligible for targeted therapies and potentially overcome resistance mechanisms encountered with narrower agents [S1].

Outlook and Risk Factors

Looking ahead, the company’s prospects depend heavily on successful clinical progress with silevertinib’s ongoing Phase 2 trials and timely initiation of the GBM randomized study [S3],[S1]. Milestone achievements from the Servier licensing agreement may provide additional revenue streams.

However, risks remain substantial including inherent uncertainties in clinical development outcomes; potential delays or disruptions in FDA regulatory review processes exacerbated by government funding constraints and staffing challenges noted amid recent federal shutdowns [S2],[S14],[S21]; evolving healthcare policy reforms targeting drug pricing transparency and reimbursement frameworks that could impact commercial viability [S4]-[S8],[S14]; as well as dependency on collaboration agreements which carry execution risks including possible termination or intellectual property sharing limitations [S8],[S12]. Macroeconomic factors such as inflationary pressures affecting clinical trial costs or supply chains add further complexity.

Returns and Capital Allocation

For the year ended December 31, 2025 Black Diamond realized an approximate return on equity near 20%, calculated as net income divided by equity ($22.37M / $112.21M), highlighting emerging profitability relative to invested capital despite a history of losses [F1].

Operating cash flow turned decisively positive at nearly $29.6 million reflecting operational improvements or milestone-related inflows while capital expenditure remained negligible—indicative of R&D-focused investment rather than asset-heavy expansion typical of early-stage biopharmaceutical firms [F1]. No dividends or share buybacks were reported; earnings appear retained to support pipeline advancement.

Liquidity remains strong with year-end cash balances of approximately $21 million complemented by substantial current assets providing runway coverage into the medium term as per management disclosures covering plans through at least mid-decade horizons [F1],[N1],[S3].

Conclusion

Black Diamond Therapeutics has transitioned from sustained preclinical loss phases into operating profitability supported by advancement of its precision oncology pipeline led by silevertinib alongside strategic partnerships such as the Servier licensing deal. Strong liquidity coupled with positive operating cash flow supports ongoing clinical development efforts.

Its MasterKey therapy platform presents an innovative approach targeting mutation families across tumor types that could expand patient access to targeted treatments beyond conventional single-mutation drugs; however clinical validation remains critical amidst a competitive oncology landscape.

Investors should monitor upcoming clinical milestones including Phase 2 GBM trial initiation expected shortly as well as progression updates from collaboration arrangements that may materially influence future valuation within this high-risk/high-reward sector.

This report summarizes publicly available financial information from SEC filings and news sources without offering investment advice or price targets. Operational outcomes remain subject to inherent uncertainties requiring continuous reassessment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments