AXT INC’s Revenue Surge and Strategic Investment in China Capacity

AXT INC has experienced rapid revenue growth driven by specialty semiconductor substrates, but faces operating losses and geopolitical headwinds, prompting a substantial capital raise to expand Chinese manufacturing capacity.

AXT INC's revenue ballooned from $20M in 2023 to nearly $100M in 2024, fueled by increased demand for indium phosphide, gallium arsenide, and germanium wafers largely in Asia-Pacific markets. Despite this top-line surge, the company struggled with operating losses worsening to -$22M in 2025 amid rising raw material costs, trade tariffs, and environmental shutdowns in China. Geopolitical tensions have complicated export controls and operational flexibility. To address capacity constraints and market growth opportunities, AXTI raised $93.9M in late 2025 to scale its Tongmei subsidiary’s indium phosphide wafer output. Its proprietary Vertical Gradient Freeze (VGF) technology and integrated supply chain contribute to competitive positioning but require careful navigation of regulatory risks. Financially, liquidity improved significantly post-offering, yet negative free cash flow and a negative ROE highlight ongoing challenges.

Dramatic Revenue Growth Fueled by Specialty Substrate Demand

AXT INC’s revenue trajectory over recent years displays a striking expansion centered on its specialty semiconductor substrates portfolio. The company’s reported revenues leapt from $20.4 million in FY2023 to an impressive $99.4 million in FY2024 ([F1]). This near-fivefold increase was chiefly driven by robust global end-market demand for indium phosphide (InP), gallium arsenide (GaAs), and germanium (Ge) wafer substrates.

A substantial share of these sales flows from international customers concentrated particularly in China, which accounted for over 60% of total revenues by late 2025 ([S4], [S5]). These wafers serve critical applications within fiber optic communication networks, wireless telecommunications infrastructure, LED lighting technologies, laser devices, and photovoltaic solar cells targeting both terrestrial and space markets—segments witnessing technological advancements that amplify substrate consumption.

Despite overall growth momentum, revenue composition shifts influenced margin compression as product mix moved toward raw materials sales with thinner margins relative to higher-margin substrate products. Notably, revenues from raw materials such as purified gallium and pBN crucibles also contributed materially through consolidated subsidiaries and joint ventures based primarily in China ([S24]).

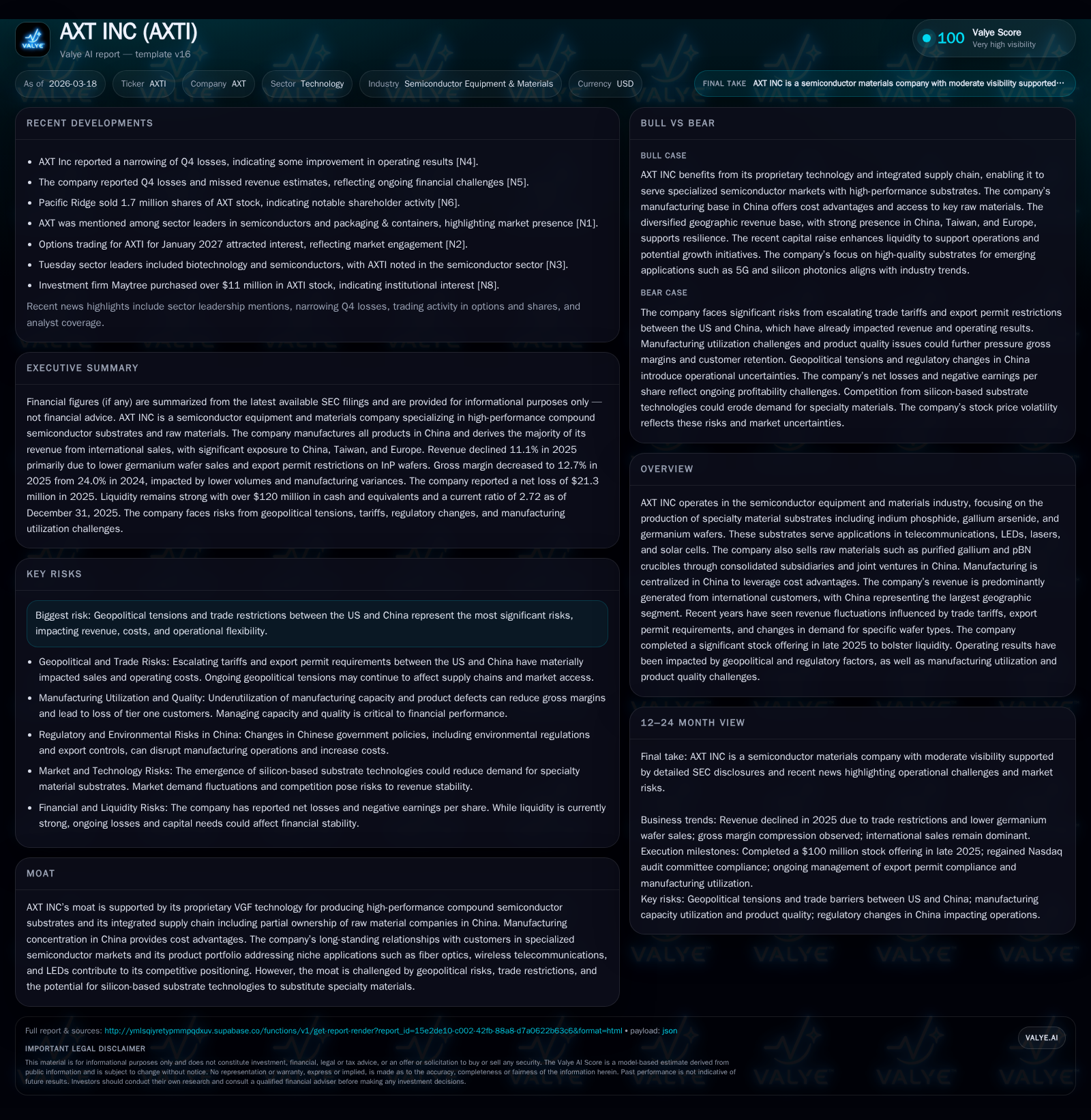

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -21 | -13 | -22 | -82.9% | ||

| 2024 | 99 | -12 | -12 | -15 | +386.4% | -221.0% |

| 2023 | 20 | -4 | 3 | -22 | -23.8% | -370.0% |

| 2022 | 27 | 1 | -9 | 13 | -29.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -19 | -7.8 |

| 2024 | -18 | -6.0 |

| 2023 | -7 | -1.8 |

| 2022 | -37 | 0.6 |

Source: SEC companyfacts cache [F1].

Table summarizes AXTI's recent annual financial performance highlighting significant revenue growth coupled with profitability challenges ([F1]).

Profitability Struggles Amid Rising Costs and Operational Challenges

Profitability trends sharply diverged from top-line growth as escalating raw material costs—particularly purified gallium—compressed gross margins over the recent period ([S2], [S4]). Operating income shifted dramatically from a positive $12.5 million profit in FY2022 to negative $21.9 million by FY2025 ([F1]). This downturn coincided with U.S.-imposed tariffs affecting input costs and expediting export permit requirements imposed by Chinese regulators starting early 2025 that curtailed supply chain fluidity.

Manufacturing operations centralized in China further faced non-economic headwinds including government-mandated environmental shutdowns to address pollution concerns ([S2]). Such intermittent halts lowered manufacturing yields — a critical metric for wafer producers where impurities or defects sharply reduce substrate value.

Operational leverage accentuated losses as fixed overheads remained elevated amidst constrained volume realizations during periods of curtailed production capability.

Free cash flow remained under pressure; despite relatively stable capital expenditures around $6 million annually supporting capacity expansion initiatives aimed at growing InP substrates ([F1], [S21]). Operating cash flows declined to -$12.8 million in FY2025 ([F1]).

Geopolitical Risks Shaping Business Fundamentals

AXT INC confronts considerable geopolitical risks stemming from ongoing U.S.-China trade tensions that directly influence its cost base and customer access ([S1], [S2]). Specifically, export controls enacted by the Chinese government since February 2025 have limited shipments of indium phosphide wafers—a core product—to key international customers including those in Taiwan, Japan, Europe, and North America ([S12]).

These policies have led to a contraction of sales outside mainland China post-implementation: North American revenue plummeted approximately 77%, European sales declined nearly 19%, while Taiwan saw a reduction of roughly 7%, all year-over-year for calendar year 2025 ([S12]). In contrast, sales within China remained relatively stable at about $55 million but decelerated slightly compared to prior years amid deliberate reductions in lower-margin germanium substrate shipments due to raw material prices ([S24]).

Such regulatory dynamics complicate AXTI's operating model as its competitive advantage hinges on cost-efficient manufacturing in China combined with supply chain tightness enhanced through joint ventures controlling purified gallium and related materials (). However, reliance on these geographies exposes the company to abrupt changes in export licensing regimes or transit restrictions that could cause shipment delays or cost increases ([S2]).

Capital Infusion Targeted at Scaling Indium Phosphide Production

In response to these operational constraints accompanied by strategic ambition to capitalize on expanding global demand for InP substrates—widely used for high-speed optical communication devices—AXTI completed a significant common stock offering on December 30, 2025 ([N11], [S6]). The issuance raised net proceeds of approximately $93.9 million after underwriting fees.

This capital injection is earmarked primarily for scaling manufacturing capacity at Tongmei subsidiary facilities located within China, aiming explicitly to increase output of indium phosphide wafers intended for global markets ([N11], [S6]). Secondary uses include funding continued research & development efforts focusing on product enhancement alongside meeting general corporate financial obligations.

Market reception acknowledged the necessity of bolstering liquidity given stretched operating cash flows amid ongoing losses while highlighting potential upside leveraging expanded capacity once new volumes ramp effectively ([N11],[N7]).

Sector-Specific Competitive Edges: VGF Technology and Integrated Supply Chain

At the core of AXTI’s competitive moat is its proprietary Vertical Gradient Freeze (VGF) process—a crystal growth technique enabling high-purity compound semiconductor substrates with superior wafer uniformity critical for performance-sensitive applications such as fiber optics communication modules and advanced LEDs (, [S22]).

The VGF process typically yields larger grain sizes with fewer defects compared to alternative Bridgman or Liquid Encapsulated Czochralski methods favored elsewhere across the industry—a technical differentiation helping AXTI command technical credibility amongst specialized clients.

Moreover, partial ownership stakes held via subsidiaries and joint ventures related to purified gallium extraction and pBN crucible production underpin vertical integration benefits that improve pricing control alongside shortened lead times vital in volatile supply environments characteristic of the semiconductor materials market (, [S22], [S8]).

This tightly coupled supply chain synergy facilitates some insulation against raw material shortages or price escalations observed globally yet remains vulnerable given geopolitical uncertainties surrounding cross-border resource access.

Outlook and Milestones: Watching Export Policy and Demand Shifts

The company has not issued explicit forward guidance recently but highlights several key near-term factors warranting investor attention ([N1], [N7], [S3]):

- Changes or relaxations in Chinese export permit regimes affecting compound substrate shipments could catalyze recovery outside core domestic markets.

- The pace at which Tongmei’s expanded InP manufacturing lines become fully operational will materially influence top-line stabilization or growth beyond current levels.

- Monitoring order book trends particularly within Asia-Pacific telecommunications and LED sectors where next-generation device cycles may spur substrate demand surges.

- Competitive threats via advances in silicon-based substrate technology potentially encroaching upon niche segments previously reserved for compound semiconductors.

These indicators serve as critical barometers for assessing whether capacity expansions deliver profitable scaling or if macro uncertainties persistently restrain earnings trajectories.

Financial Health: Liquidity, Debt Profile, and Capital Allocation Discipline

Post-offering liquidity improved markedly with cash & equivalents climbing from about $33.8 million at December end-2024 to roughly $120.3 million at December end-2025 reflecting the large capital raise combined with moderate cash burn reduction ([F1], [S6], [S16]). Current assets stood robust at approximately $246.6 million against current liabilities near $90.5 million yielding a strong current ratio around 2.72x that supports near-term operational needs comfortably ([F1]).

Short-term bank loans aggregated roughly $58.5 million; total debt including long-term portions approximated $63 million predominantly secured by real estate assets tied to subsidiaries’ manufacturing facilities within China ([S6],[S10],[S13],[S14],[S15],[S16]). Interest rates range mostly between low-to-mid single digits consistent with Chinese banking benchmarks.

Capital allocation has been cautious: no fresh share repurchases have occurred since policy scaling back post-2017; dividend activity remains confined to preferred stock accruals unpaid so far limiting distributable cash flows available for common shareholders ([F1],[S20],[S25],).

Return on equity calculated approximately -7.8% based on net losses against sizable shareholder equity near $273 million confirms negative value creation contemporaneous with restructuring efforts ([F1]). Free cash flow remains challenging; estimated near negative $18.8 million indicating continuing pressure on internal funding requiring external liquidity injections consistent with recent offerings ([F1]).

This analysis synthesizes publicly available SEC filings and reputable news sources up through March 2026 regarding AXT INC's financial performance, market positioning, operational challenges, geopolitical context, strategic financial actions, and competitive attributes within specialty semiconductor substrates manufacturing sector without providing any investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments