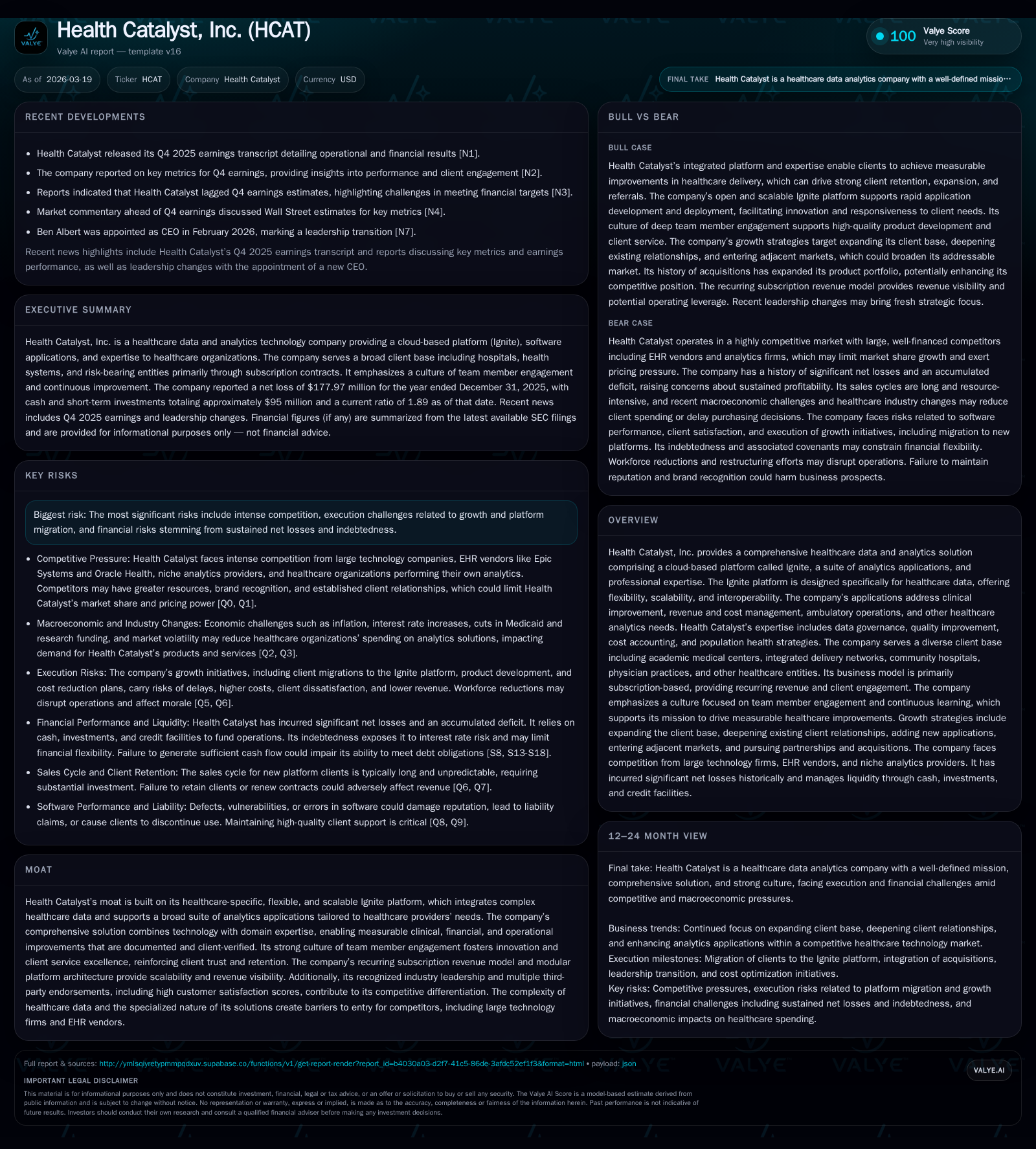

Health Catalyst’s Declining Profitability Challenges Growth Trajectory and Capital Efficiency

Persistent operating losses raise questions on scalability despite a strong healthcare-specific analytics platform.

Health Catalyst, Inc. operates a specialized cloud-based data and analytics platform for healthcare providers, aiming to deliver measurable clinical and financial improvements. Over the past four years, the company has exhibited recurring net losses with operating income deteriorating sharply in 2025 despite a business model grounded in subscription revenues and client engagement. The future growth is contingent on client renewal, expansion, and successful new product adoption amid intense competition and regulatory challenges. Capital allocation highlights minimal share repurchases and constrained free cash flows, reflecting ongoing profitability and leverage concerns.

Company Overview

Health Catalyst, Inc. presents itself as a leading provider of healthcare-specific data analytics technology aimed at enabling measurable clinical improvement alongside financial and operational optimization for a broad clientele including academic medical centers, integrated delivery networks, hospitals, physician practices, ACOs, and health insurers [S17][S15]. Its core offering centers on the Ignite platform—a cloud-based data ecosystem tailored specifically for healthcare data ingestion, integration of standardized terminologies, and development of analytic applications [S15][S19]. Complementing technology with domain expertise such as quality improvement strategy and population health management forms the backbone of its comprehensive solution [S17][S19].

Past Growth & Historical Performance

Historically spanning fiscal years 2022 through 2025, Health Catalyst’s financial results reveal an intensification of operating losses despite an established recurring revenue base driven by subscription contracts. The company's operating income deteriorated from -$140.0 million in FY22 to -$69.8 million in FY24 before worsening substantially to -$160.9 million by FY25 [F1]. Similarly, net income trends show deepening deficits: from -$137.4 million in FY22 to a steep -$177.9 million in FY25 [F1].

Operating cash flow (CFO) followed a volatile path—negative through 2022 (-$35.3M) and 2023 (-$33.1M)—with a modest rebound to $14.6 million in FY24 but falling back close to neutral at $0.7 million in FY25 [F1]. Capital expenditures have been relatively restrained around low single-digit millions annually ($0.97M in FY25), resulting in near nil free cash flow (CFO minus capex) at -$0.24 million most recently [F1].

This trend indicates ongoing operational scaling costs that have not yet translated into profitability or sustained positive cash generation despite the firm's steady client base.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -178 | 1 | -161 | 1 | -156.1% |

| 2024 | -70 | 15 | -70 | 2 | +41.2% |

| 2023 | -118 | -33 | -127 | 1 | +14.0% |

| 2022 | -137 | -35 | -140 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 5 | 0 | -72.4 |

| 2024 | 0 | 13 | -19.0 |

| 2023 | 2 | -34 | -32.2 |

| 2022 | 8 | -37 | -32.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are unavailable from provided datasets; YoY changes calculated where applicable.

Future Growth Prospects

Growth prospects hinge on expanding adoption of the Ignite platform’s modular architecture that supports multiple analytics applications across key focus areas such as clinical improvement, revenue cycle management, ambulatory operations management, registry reporting (e.g., cardiology and cancer), cost accounting models (PowerCosting), labor productivity tools (PowerLabor), population health strategy (Value Optimizer), patient engagement solutions (Upfront), care orchestration (Lumeon), among others [S17][S19][S22].

The company invests heavily in augmenting this ecosystem combined with expert advisory services—data governance support through managed offerings designed to accelerate time-to-value for providers [S19]. With over 2000 documented client-verified improvements historically delivered across domains that build trust driving account expansion and referrals (“Health Catalyst Flywheel”), client loyalty forms a pillar for incremental revenue growth [S13][S17].

Nonetheless,the prospect faces tangible ceilings from intense competitive pressures posed by both broader tech giants like IBM and Optum Analytics as well as entrenched EHR vendors such as Epic Systems and Oracle Health who offer their own analytics modules [S11][S14]. Additionally, industry niche vendors and some health systems’ in-house technologies challenge market capture [S11][S14]. Price competition may compress margins on new contracts.

Regulatory uncertainties also loom large: compliance with HIPAA privacy laws combined with scrutiny on anti-kickback statutes and potential FDA oversight over analytical software perceived as medical devices raise execution risks that could slow product rollout or enhance compliance costs [S8][S12][S18][S24][S25]. Moreover, covenants restricting dividend payments or further indebtedness limit financial maneuverability [S16].

Forecasts / Milestones / Expectations

Explicit forward-looking guidance is absent from the public filings but key monitoring criteria shall include quarterly trends toward narrowing operating losses or margin improvements per new deal ramps reported most recently for Q4 FY25 earnings [N1][N2]. Furthermore, the impact of newly installed CEO Ben Albert appointed February 2026 introduces anticipated strategic shifts potentially impacting operational efficiency or sales effectiveness [N7]. Client addition/loss trends are also essential metrics.

Revenues tied closely to subscription renewals imply stability if churn remains low but securing sizable new enterprise platforms will be obligatory for step function enterprise growth beyond current scale.

Returns / Capital Allocation

From a capital allocation perspective at least $5 million were deployed toward share repurchases during FY25 with no dividends declared [F1][S9], consistent with a nascent stage post-IPO growth profile focused on reinvestment rather than shareholder distributions.

Equity contracted alongside rising accumulated losses—equity declined from $425 million at end-2022 down to approximately $246 million by end-2025—reflecting ongoing net deficits eroding retained earnings [F1]. The calculated return on equity based on latest net loss was about negative -72%, underscoring unprofitability despite invested resources.

Liquidity remained reasonable supported by approximately $50 million cash balance at year-end plus availability under credit facilities reflecting leverage capacity managed conservatively yet influenced by outstanding debt accruing interest at SOFR+6.5% per annum [F1][S5][S7][S16].

Operating cash flow volatility reflects ongoing investment needs with just-breakeven FCF indicating constraint toward discretionary spend or aggressive buyback plans absent profit recovery [F1]. This dynamics necessitates scrutiny over capital use effectiveness amid competitive pressures.

Competitive Moat and Risks

Health Catalyst’s moat stems from its healthcare-specialized Ignite platform which integrates complex heterogeneous data types specific to hospital operations far beyond generic analytics platforms; this flexibility combined with integrated domain expertise offers providers actionable insights leading to documented high-impact outcomes yielding client loyalty .

However competitiveness includes formidable players with broader resources capable of replicating or bundling similar features into existing electronic health records or analytics suites challenging pricing power or client acquisition velocity [S11][S14]. Regulatory interpretations affecting software classification or healthcare service definitions may trigger costly compliance responses harming growth trajectories or margins [S18][S24]. Its historical cumulative losses necessitate sustained execution discipline around expense management.

Conclusion: What to Monitor Going Forward

Despite notable strengths rooted in healthcare-specific product design paired with expert services promoting documented client improvement outcomes forming a virtuous "flywheel", Health Catalyst faces layered challenges balancing scaling commitments against persistent operating deficits compounded by stiff competition and regulation.

Investor attention should focus on sequential improvement in profitability metrics; effectiveness of new leadership under CEO Ben Albert; progress in expanding platform client count beyond existing footprints; regulatory environment developments impacting software products; and capital structure actions signaling confidence or urgency.

--

Disclaimer: This analysis is based solely on publicly available information without any non-public material insights. It is not intended as investment advice or recommendations but rather an informational review aligned with rigorous internal research standards.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments