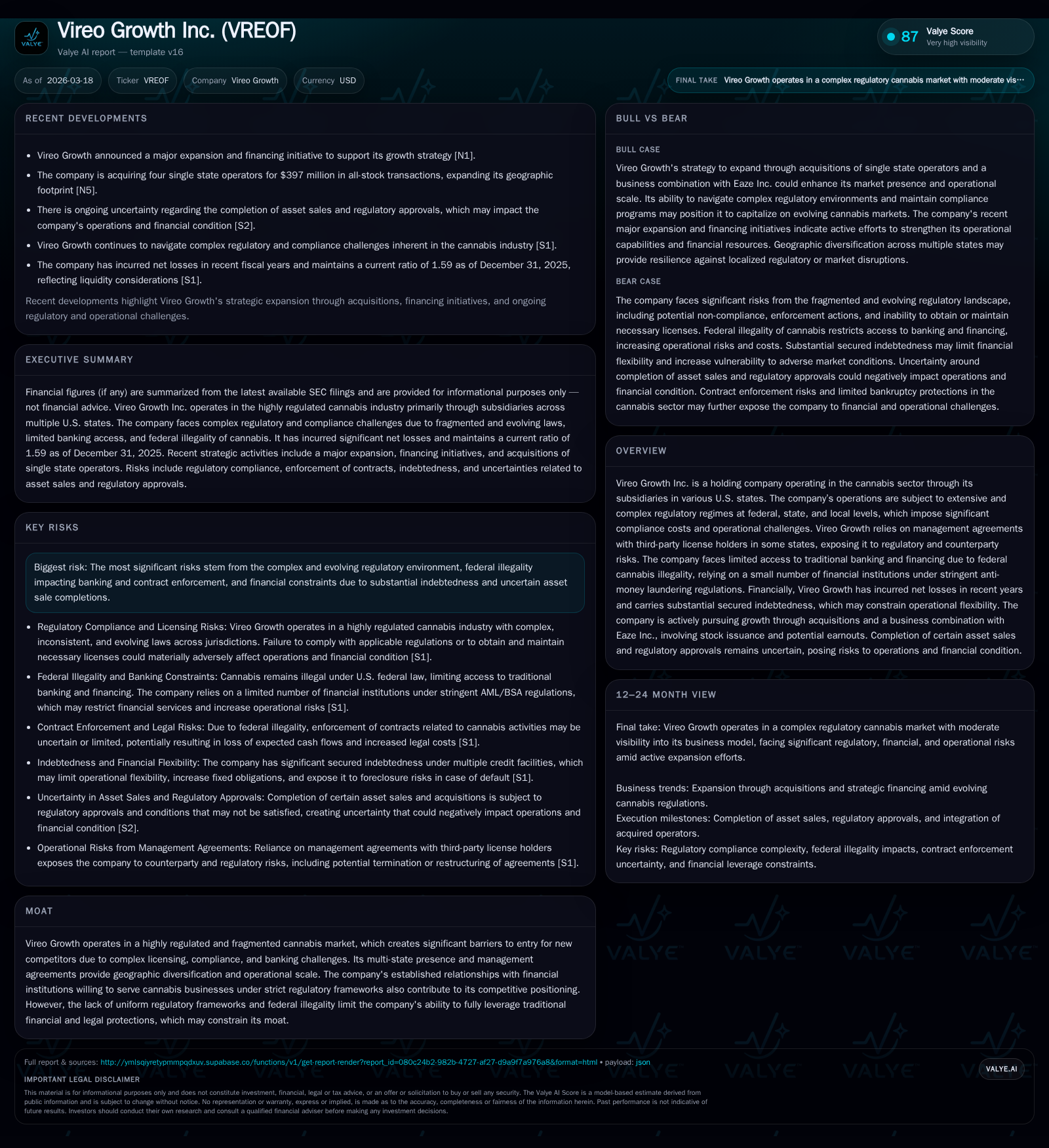

Vireo Growth Inc. Pushes Expansion Amid Regulatory and Financial Crosswinds

The company leverages a multi-state cannabis presence through acquisitions while confronting intricate regulatory frameworks and a substantial debt load.

Vireo Growth Inc. operates across several U.S. states within the tightly regulated cannabis sector, carrying significant secured debt and facing federal prohibition complexities that impact its financial flexibility and operational risk. Historical trends reveal a sharp operating income decline in 2025 despite prior gains, compounded by high capital expenditures and ongoing net losses. The company’s growth is fueled by planned acquisitions, notably the Schwazze asset sale pending regulatory approval, which embodies both opportunity and uncertainty. Capital structure constraints and inconsistent profitability underscore challenges ahead for cash flow management and investor returns.

Historical Financial Performance Reflecting Operational Shifts

Vireo Growth’s recent financial data delineates a volatile trajectory with distinct inflection points. In fiscal year 2024, the company reported positive operating income of approximately $13.6 million, reversing earlier years of operating losses (notably -$6.9 million in 2022). However, this gain rapidly reversed in FY2025 when operating income declined sharply to a slight loss of about $1 million ([F1]). Net income fared worse, deepening into a substantial loss of over $68 million in 2025 compared to approximately -$28 million in the prior year, reflecting escalated operational costs including compliance burdens related to regulatory expansions and intense competitive pressures intrinsic to the fragmented cannabis market.

Despite these losses at the bottom line, operating cash flow presented a turnaround from negative figures (-$10.2 million in 2024) to positive $3.7 million in 2025 ([F1]), indicating improved underlying cash-generating capacity even as net income deteriorated. This anomaly reflects non-cash charges or working capital movements but calls attention to the importance of cash metrics over pure accounting profitability.

Capital expenditure (capex) surged beyond doubling year-on-year to $28.3 million in 2025 from $11.7 million in 2024 ([F1]). This reflects aggressive investments into cultivation facilities, dispensaries, or processing assets—the physical backbone for future revenue scaling but one which exacerbates cash outflow pressures during continued unprofitability.

Equity grew significantly to about $307 million in 2025 from roughly $56 million in 2024 ([F1]), likely driven by equity raises or revaluations connected to capital transactions, although such expansion dilutes historical return ratios given accumulated deficits approaching $300 million.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -68 | 4 | -1 | 28 | -143.2% |

| 2024 | -28 | -10 | 14 | 12 | -9.6% |

| 2023 | -26 | -1 | 11 | 5 | +39.8% |

| 2022 | -42 | -18 | -7 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -25 | -22.2 |

| 2024 | -22 | -50.4 |

| 2023 | -6 | 159.2 |

| 2022 | -24 | -1233.9 |

Source: SEC companyfacts cache [F1].

Operating income’s steep drop in FY2025 follows an incremental build during FY2023-24 but reveals flattening margins under expanding compliance costs and operational complexity ([F1]).

Navigating Fragmented Cannabis Regulatory Regimes

Vireo Growth operates within an exceptionally tangled web of state-specific cannabis laws layered atop the ongoing federal Schedule I prohibition that classifies marijuana as illegal under the Controlled Substances Act ([S1]). States where Vireo holds licensed subsidiaries—New York, Minnesota, Maryland, Missouri, Nevada and Utah—have distinct licensing scopes catering either to medical or adult-use cannabis markets ([S14]). Regulatory regimes vary considerably by jurisdiction with different testing protocols, packaging rules including child-resistant requirements, and strict track-and-trace systems designed to prevent diversion and unauthorized use ([S1],[S7],[S14]).

The lack of harmonized regulations imposes significant compliance overhead as simultaneously complying with conflicting standards elevates administrative costs and risks non-compliance penalties ([S7]). For example, one state may allow certain formulations or marketing claims prohibited elsewhere. Licensing regimes enforce tight controls on ownership structures with "unsuitable persons" provisions possibly forcing redemptions an outcome that can divert company resources unexpectedly ([S5]).

Federal prohibition further complicates financial operations by restricting access to traditional banking services due to anti-money laundering mandates and FinCEN reporting guidelines ([S25]). Vireo relies on limited financial institutions willing to serve cannabis businesses under stringent terms but faces rising financing costs reflective of heightened counterparty risks. This constrained access limits liquidity options and elevates financing risk.

Collectively these conditions create a complex operating environment often described within the industry as requiring robust "compliance frameworks" tailored to each license jurisdiction—a costly endeavor that serves as both barrier for new entrants but also pressure point for existing operators aiming for scale ([S7],[S14]).

Strategic Growth Through Acquisitions and Expansion Plans

Vireo's chosen route for growth primarily hinges on acquisitions across its multi-state footprint rather than relying solely on organic expansion ([N1],[S2]). The most material development is its planned credit bid acquisition of assets from Schwazze via an Asset Sale process structured under a Restructuring Support Agreement (RSA) ([N1],[S2]).

The credit bid strategy effectively allows Vireo to acquire Schwazze's collateralized assets through offsetting owed debt rather than upfront cash purchase but this approach carries risk: competing bids might emerge at auction under UCC public disposition rules, and required regulatory approvals—including multiple state-level consents—remain outstanding with uncertain timelines ([S2]). Failure could derail integration plans reducing anticipated scale benefits.

Management emphasizes acquisition synergies aimed at solidifying Vireo's geographic diversification while achieving operational scale necessary to manage fragmented state markets efficiently; however, failure risks around asset sale completion or regulatory hurdles underscore vulnerability inherent to expansion-by-acquisition models in this sector ([N1],[S2]). The deal follows previous failed M&A attempts such as the aborted Verano transaction that gave rise to litigation settled recently at modest consideration ([S13],[S15]).

Capital Structure Risks and Debt Burden Impacting Flexibility

An unmistakable constraint shaping Vireo's operational latitude is its substantial secured indebtedness across multiple credit facilities totaling up to $120 million plus ancillary convertible notes totaling roughly another $10 million ([S4],[S5],[S6]). These financing arrangements require fixed quarterly amortizations of about $3 million underscoring sizable mandatory cash outlays for debt service independent of business performance. All debt instruments are secured by liens on substantially all present and future assets meaning any default could trigger foreclosure procedures jeopardizing control over core operational assets or compulsory asset sales potentially at distressed valuations. This scenario poses systemic risk not only financially but also operationally given lenders’ possible interference disrupting supplier or customer relationships critical for normalized functioning (,).

Interest expense sensitivity adds complexity since many borrowings carry variable rates pegged above prime rate exposing Vireo to cost escalations within rising interest rate cycles common since late-2022 ([S6],[S9]). Increased debt service obligations compete with investment needs—capital expenditures doubled in FY2025—forcing tough resource allocation decisions amidst uncertain growth returns.

Indebtedness restricts ability to raise additional financing on favorable terms which could hamper agility needed amid evolving state policies or competitive threats ([S8],[S10]). This credit profile alongside accumulated deficit nearing $300 million reduces equity cushion amplifying vulnerability should earnings fail short or unexpected adverse regulatory actions materialize.

Cash Flow Dynamics and Profitability Challenges

While net earnings have trended negative with widening losses culminating near-$68 million for FY2025 ([F1]), operating cash flows demonstrated notable improvement—from approximately negative $10 million in FY2024 into positive territory reaching roughly $3.7 million last fiscal year. Such divergence hints at varying impacts from non-cash expenses balancing cash inflows against accounting recognition rules.

However free cash flow remains firmly negative after factoring heavy capex spending which more than doubled year-over-year reaching over $28 million last fiscal year ([F1]) reflecting ongoing investment into infrastructure expansion—crucial for future sales volume growth yet exacting on liquidity. Persistent negative free cash flow (-$24.6 million approximate) signals structural need for continued external funding alongside disciplined operational improvement if sustainable profitability is sought.

This dynamic confirms an industry-stage balancing act: prioritizing capacity build-out while managing stringent regulatory-induced cost overheads restricts margin recovery despite burgeoning market opportunities at the state level. Longer term success demands converting investment dollars into scalable revenue growth exceeding combined cost escalations ahead of profitability inflection points which remain uncertain.

Investor Returns Expectations: Dividends and ROE Analysis

Consistent with typical profiles among emerging multi-state cannabis operators subject to high reinvestment demands and regulatory complexities, Vireo has never declared dividends nor currently anticipates doing so foreseeable future; thus investor returns hinge exclusively on equity price appreciation linked to successful execution narratives rather than direct income returns ([F1],[S5],[S11]). Accumulated deficits exceeding $299 million erode capital base resulting in approximated return on equity around negative 22%, reflecting operating losses relative to shareholder equity calculated for FY2025 ([F1]). This negative ROE underscores capital consumption as opposed to value generation during recent periods limiting shareholder wealth creation absent multiple expansions or transformative gains via strategic transactions. Buybacks have not been reported indicating preservation of available liquidity toward growth imperatives favored over shareholder returns presently.

Key Milestones and Regulatory Approvals Ahead

Critical upcoming milestones center primarily around completion of definitive transactions linked to Schwazze asset sale scheduled under a credit bid auction structure contingent upon numerous conditions precedent including multiple regulatory consents across jurisdictions where assets operate ([N1],[S2]). Regulatory approval timing remains uncertain with potential delays prolonging transaction closure beyond initially anticipated horizons raising integration timing risk alongside deal execution risk if other bidders prevail. Nonfulfillment triggers for termination rights exist exposing prospective cancellation risk inherent in pending transactions context which may negatively impact market sentiment if unresolved near term. Other approvals relating licenses modifications or changes following transaction completion impacting operational scope will bear on post-close integration gains realization with ramifications extending through execution horizons beyond calendar year quarterly earnings.[N1] Monitoring announcements around state authority responses, and progress applying security protocols aligned with evolving federal guidance will be vital indicators assessing realization likelihood against strategic objectives.[S2] These factors collectively define key watchpoints influencing valuation trajectories independent from ongoing internal operational metrics.

Disclaimer: This analysis is based solely on disclosed filings and publicly available information without speculation beyond stated facts; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments