Purple Biotech’s Strategic Reset: Balancing Clinical Progress with Financial Realignment

Purple Biotech confronts a pivotal juncture as clinical advancements and financial setbacks reshape its oncology R&D trajectory.

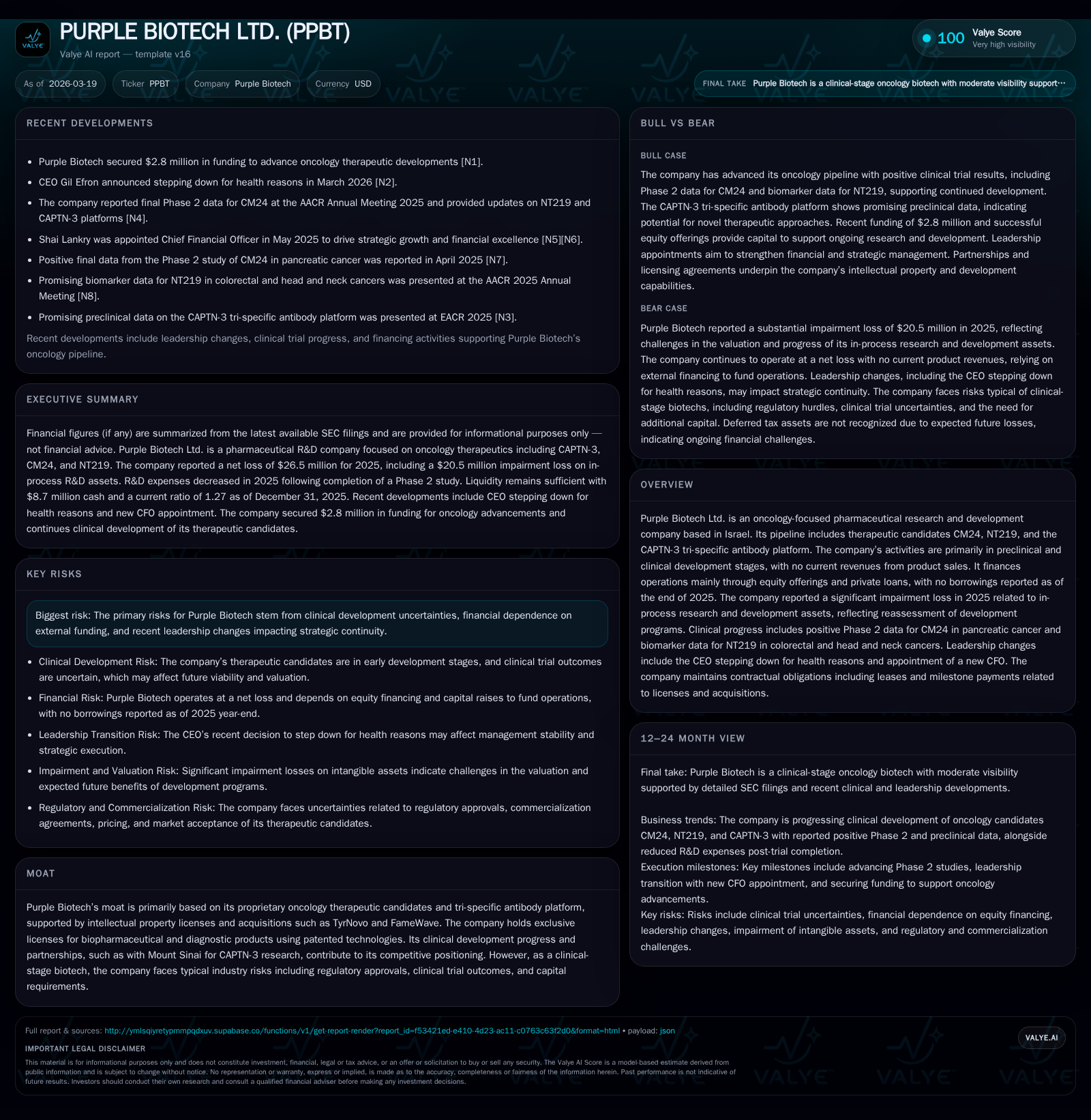

Purple Biotech Ltd., an Israeli oncology-focused biotech, reported significant operational challenges in 2025 marked by a $20.5 million impairment loss relating to its CM24 and NT219 therapeutic programs alongside leadership transitions. Despite this, the company demonstrated promising clinical progress with positive Phase 2 data for CM24 and biomarker validation for NT219. The reduction in R&D expenses following trial completions contrasts sharply with heightened operating losses driven by impairment charges. Financing efforts in late 2024 and 2025 through equity offerings have maintained liquidity, leaving Purple Biotech debt-free but reliant on external capital to sustain pipeline development. Monitoring upcoming clinical milestones and strategic execution under new leadership will be critical for the company’s growth and capital management outlook.

From Clinical Breakthroughs to Financial Setbacks: Purple Biotech’s Recent Performance

Purple Biotech Ltd., an Israeli clinical-stage oncology drug developer, experienced sharp divergence between scientific progress and financial outcomes during fiscal year (FY) 2025. The company’s hallmark achievements include encouraging Phase 2 results for CM24 in pancreatic cancer and ongoing biomarker validations for NT219 in colorectal and head & neck cancers [S1], underpinning potential therapeutic value in high-need oncology segments.

Yet these advances were overshadowed by a significant financial setback — a $20.5 million non-cash impairment charge tied to impairments of in-process research and development assets related to CM24 and NT219 programs [S1]. This write-down drove the operating loss up to $27.4 million, a nearly 150% increase over the prior-year loss of $11.0 million despite a substantial reduction in clinical trial-related R&D spending.

Specifically, R&D expenses declined by over half (53%) from $7.6 million in 2024 to $3.7 million in 2025 as intensive Phase 2 trial activities wrapped up and shifted toward Chemistry, Manufacturing, and Controls (CMC) support tasks [S1]. General & administrative (G&A) costs edged slightly higher by about 4%, driven by increased consulting fees and salary costs that partially offset savings on insurance premiums and share-based payments [S1].

The net loss consequently expanded from $7.3 million to $26.5 million year-over-year principally due to the impairment impact [S1]. However, on a non-IFRS adjusted basis stripping out this charge alongside share-based compensation expenses, the operating loss actually decreased by roughly one-third to $6.6 million versus $10.2 million in 2024 — reflecting underlying cost efficiencies post-trial completion [S1]. This nuanced performance profile highlights the complexity of interpreting biotech financials where episodic write-downs may mask improving operational leverage.

Historical performance (annual)

| FY |

|---|

| 2025 |

| 2024 |

| 2023 |

| 2022 |

Source: SEC companyfacts cache [F1].

Note: Revenue historically stable at nominal levels pre-2019; latest revenue data from [F1]. Operating and net losses reflect IFRS figures including impairments [S1].

The Nexus of Pipeline Science and Impairment Write-Downs

The $20.5 million impairment charge recorded at year-end 2025 pertains mainly to Purple Biotech’s key oncology assets CM24 and NT219 — therapeutic candidates demonstrating favorable clinical signals yet now undergoing strategic reassessment [S1][S2]. Such intangible asset impairments stem from updated valuations accounting for revised expectations regarding development costs, regulatory timelines, market potential, or probability-weighted commercial success rates.

Industry-standard valuation frameworks involve discounting projected future cash flows arising from these assets while integrating uncertainties surrounding transitioning through successive clinical phases toward regulatory approval — commonly described within biotech reporting as evaluation of ‘in-process R&D amortization’ risk [S16][S22]. Despite previously reported positive Phase 2 efficacy data for CM24 in pancreatic cancer, management may have flagged incremental hurdles impacting its projected value capture horizon.

This recalibration process included deeper scrutiny around CMC activities required for manufacturing scale-up and ensuring product quality consistency essential for registration filings — operational facets often driving significant incremental expenditures beyond initial clinical readouts [S16][S22]. Moreover, evolving biomarker validation results for NT219 could have affected development positioning indirectly influencing fair value assessments.

Such impairment recognitions do not indicate immediate stoppage but rather reflect cautious prudence on part of management redefining commercial risk parameters amid early developmental variability common to tri-specific antibody platforms like CAPTN-3 as well [S2]. This latter platform offers differentiated biology through targeting multiple antigens simultaneously but remains at preclinical/early clinical stages requiring sustained investment.

Therefore, while impairments dampen headline profitability metrics temporarily, they embody disciplined pipeline prioritization decisions designed to optimize resource allocation within intensely capital-dependent oncology biotech development cycles.

Leadership Turbulence: Executive Changes and Their Impact on Strategy

Adding complexity to this pivotal phase is Purple Biotech’s recent CEO transition announced March 13, 2026 when Gil Efron stepped down citing health reasons after guiding several years inclusive of critical Phase 2 achievements [N1]. Concurrently, the company appointed a new Chief Financial Officer responding to evolving financing demands amidst tighter capital market conditions.

Leadership shifts at this stage come with pronounced risks due to the need for maintained strategic continuity vital for shepherding pipeline progression through intricate clinical milestones while managing investor relations effectively — especially as execution against timelines is paramount amid retooling rationales implied by the impairment episode.

From an investor confidence standpoint, such departures underscore the importance of transparent communication regarding transitional governance structures alongside reaffirmation of commitment toward advancing validated assets like CM24 while optimizing CAPTN-3 platform opportunities [N1]. This dynamic places heavy emphasis on the newly appointed CFO’s role not only supervising capital raising endeavors but also navigating share-based compensation frameworks that significantly influence expense profiles [S16][S23].

Historically within biotechnology spheres where trial failures or delays instantly translate into valuation swings, executive stability serves as a bellwether facilitating smoother negotiations with potential partners or acquirers urgently needed to share developmental risks.

Financing the Oncology Quest: Equity Raises and Debt Profile

Purple Biotech has predominantly fueled its innovation engine through equity issuances complemented by some private loans now fully repaid — reflecting typical pre-commercial-stage pharma financings absent product revenues [S1][F1]. In September 2025 alone, it raised approximately $6 million via a public offering involving American Depositary Shares (ADSs) coupled with attached short-term warrants exercisable within two years priced at $10 per ADS [S1]. This transaction was preceded by a December 2024 direct registered offering garnering an additional $2.8 million at elevated share prices around $60 per ADS reflecting episodic improved market sentiment based on clinical announcements [S1][N2].

Moreover, warrant inducement transactions during mid-2024 contributed inflows totaling roughly $2 million reflecting shareholder willingness to support financing reloads albeit at dilutive terms given reduced exercise prices compared with initial grant levels [S1]. As such capital deployments remain quintessential due to zero product sales revenue streams.

Liquidity indicators concretize these dynamics: cash plus equivalents reached approximately $8.7 million as of December 31, 2025 yielding a current ratio near 1.27 which signals adequate near-term coverage against outstanding liabilities amounting near $7.75 million but warrants caution considering neither cash flow breakeven nor tangible revenues currently exist [F1][S4][S5]. Notably Purple Biotech reports no borrowings presently which underscores equity reliance though also limits financial leverage flexibility should rapid capital requirements arise unexpectedly.

Intraday usage of At-The-Market (ATM) programs remains minimal relative to total issuances indicating measured deployment consistent with prudent dilution controls customary in oncology biotech sectors seeking sustainability without excessive shareholder pressure [S1][N2].

Capital Allocation Under Strain: Evaluating Cash Burn and Capital Structure

Given the absence of revenue-generating products coupled with high upfront outlays characteristic of biopharmaceutical pipeline advancement, Purple Biotech’s operating cash flows have remained negative albeit improving during FY25 compared with FY24 due largely to scaled down Phase II clinical activity expenses after CM24 trials concluded [S16]. Net cash used in operating activities diminished significantly from about $14.4 million spent in FY24 down to approximately $5.7 million spent in FY25 demonstrating effective cost containment after peak trial spending periods subsided.

However, this improvement belies the substantial non-cash impairment that inflated reported losses without corresponding cash impact — illustrating typical biotech volatility where accounting charges distort periodic profitability measures while core burn rates reflect ongoing research investments including CMC pilot manufacturing steps critical for pivotal trial readiness or regulatory submissions [S8][S16].

Equity remains constrained down from about $33 million at end-2024 plummeting close to roughly $9.66 million at end-2025 highlighting severe erosion attributable predominantly to accumulated losses plus impairment write-offs diminishing net asset bases despite balance sheet strengthening efforts via recent offerings [F1][S1]. Return on equity calculations based on last profitable periods are no longer materially informative given rapid losses overwriting prior gains thus signaling reset conditions common among early-stage innovators where shareholder returns hinge mostly on binary trial outcomes or licensing deals rather than steady earnings streams.

Furthermore, share-based payment expenses remain notable cost contributors affecting overall operating expense profiles partly offsetting gains realized through reduced external trial spend underscoring tradeoffs faced between talent retention incentives versus leaner operational mandates during financial realignment phases [S16][S23].

What Investors Should Monitor Next: Upcoming Clinical Milestones and Funding Needs

Looking ahead beyond the immediate turbulence lies an array of critical markers shaping Purple Biotech’s trajectory including:

- Ongoing biomarker qualification studies related to NT219 which may enhance patient stratification strategies thereby potentially elevating therapeutic differentiation within colorectal and head & neck cancer indications ([N2], [S2]).

- Further development progress on CAPTN-3 tri-specific antibody platform with mounting preclinical/early clinical evidence generated through partnerships such as Mount Sinai – pivotal for determining platform viability beyond isolated candidates ([N2], corporate presentations).

- The capacity of new executive leadership team particularly CFO caliber financial stewardship coupled with CEO succession plans impacting milestone delivery cadence amidst need for fresh capital injections.

- Fundraising timing notably ATM program activation or alternate instruments deployment necessary given finite liquidity runway demonstrated by current cash position relative to burn projections ([S1], analysis).

- Regulatory submission progress or early-phase clinical data readouts providing inflection points influencing pipeline valuation recalibrations either positively offsetting prior impairments or triggering further reviews.

In summary Purple Biotech finds itself balancing a strategic reset necessitated by rigorous financial discipline amidst encouraging albeit challenging developmental strides typical for specialized oncology biotechs dependent almost exclusively on shareholder capital until licensing or commercial launch occurs fully embedding uncertainty risks fundamental to this space.

Disclaimer: This analysis is based solely on publicly available information provided up through March 19, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments